Adverse Selection

Great post on adverse selection and the dangers of crowdfunded private investing.

One of the biggest risks lurking in the shadows of private markets? Adverse selection.

Preeminent firms with a reputable brand and, presumably, dry powder to deploy, attract the best deals. Their brand is a proxy that creates ‘signal’ and accretes value.

As such, investors should be consistently asking themselves (i) why am I seeing this deal? and (ii) is this deal objectively (not subjectively) attractive irrespective of the brand effects?

The logical deduction is then, why raise via crowdfunding? Unfortunately, the answer may well be, ‘everyone else said no.’

But allocating to brand name funds might not be the answer, they’ve underperformed as they’ve become household names (full post).

In private equity, 6 firms control ~25% of industry assets under management, “the Big 6,” all of which are publicly traded, with multi-decade track records, and have institutional brands. And with PE’s market consolidation trend not seeming to show any signs of deceleration, I was curious to understand the effect on LP returns.

From ’98 to ’09, 64% of Big 6 firms outperformed the industry benchmark (i.e., the Big 6, for the most part, outperformed).

However, from ’10 to ’21, only 38% of Big 6 firms outperformed the industry benchmark (i.e., they largely underperformed relative to the broader asset class).

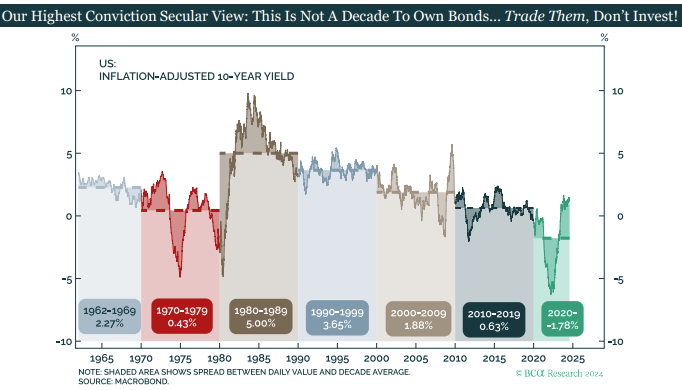

Unrealized losses on bond portfolios and issues with real estate exposures will only cause banks to pull back further from lending markets. Rate cuts will provide some relief.

I struggle to see bond investments preserving purchasing power over the next decade. Especially, after tax.

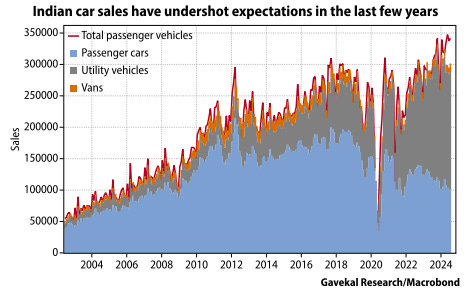

Indian car sales have not taken off exponentially.

Interesting discussion about how oil has shaped our past and present.

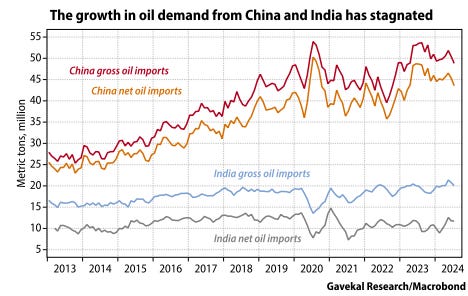

Oil demand in India has not grown at the same pace as China’s.

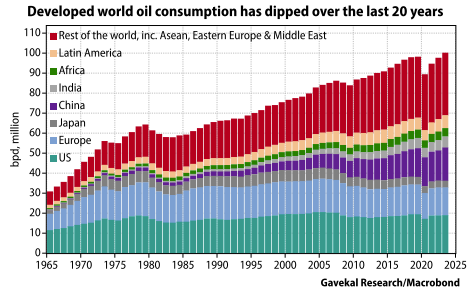

Oil demand is going to be driven by the emerging world. Oil demand has plateaued in US, Europe and Japan over the past 20 years.

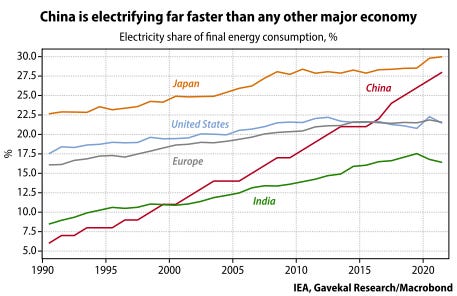

China is electrifying faster than any other major country. Energy independence.

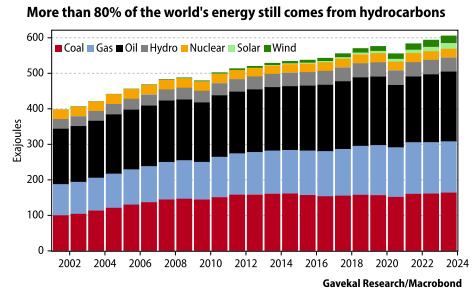

Despite efforts to transition to renewables, 80% of the world’s energy comes from fossil fuels.

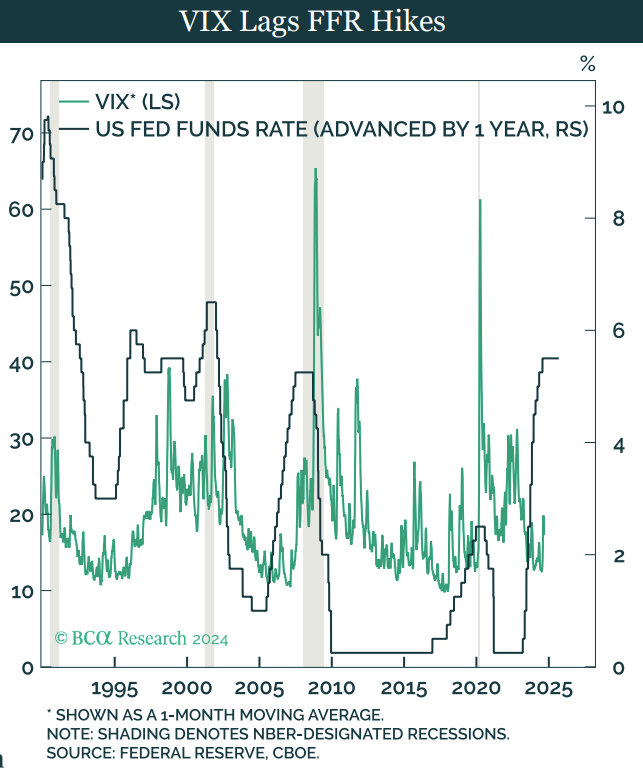

Proactive cuts could prevent the spike in the volatility, typically associated with hiking cycles.

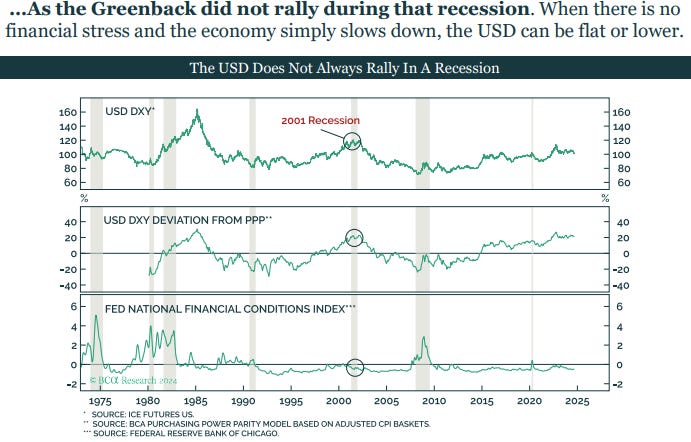

The USD tends to rally in recessions except when there isn’t a “crisis” moment.

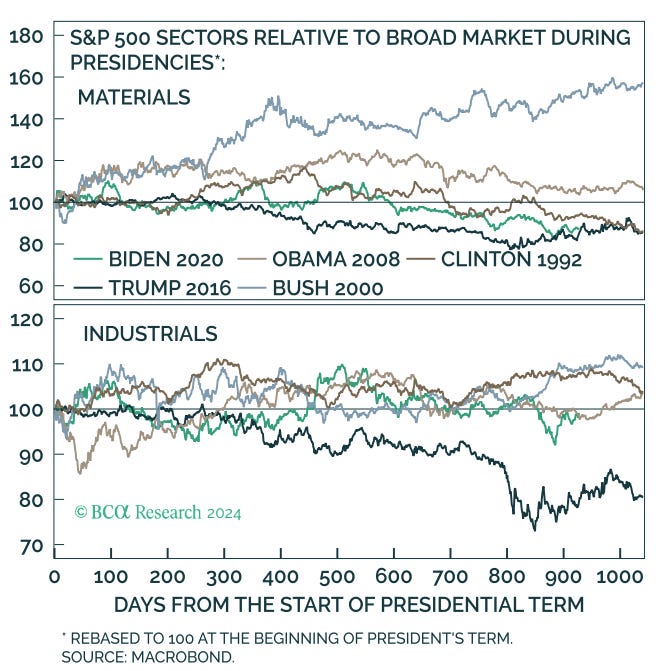

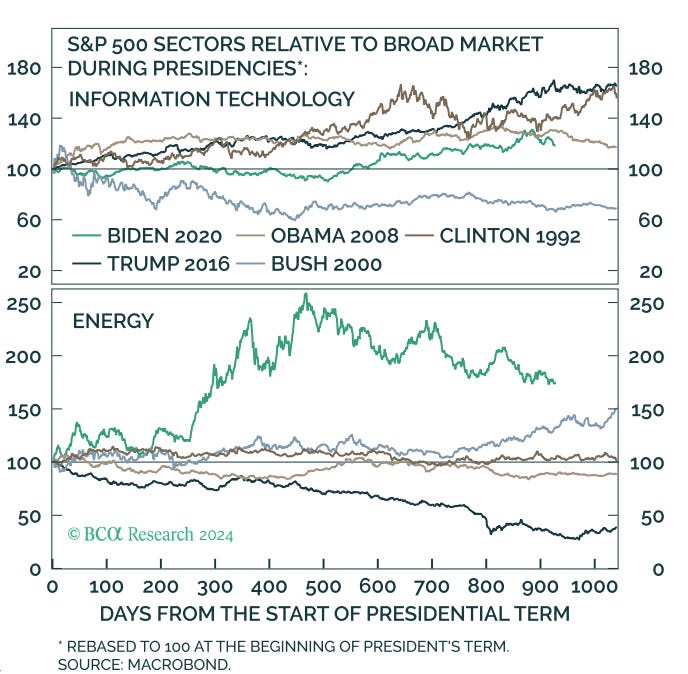

Trump was good for Tech and Biden was good for the energy sector.

Neither were good for blue collar sectors like materials and industrials.