Heading South

One of the world’s largest companies was down almost 10% yesterday after they were hit with a subpoena from the DoJ.

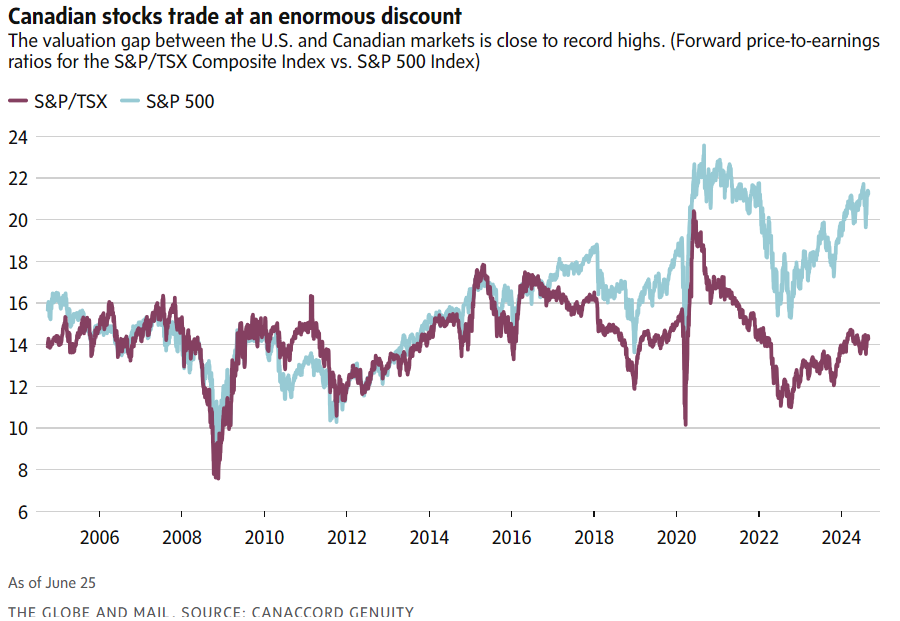

Thought provoking article in the Globe yesterday, discussing how Canada’s capital markets are not providing the capital Canada’s businesses need.

Part of this is evidenced by the discount that the Canadian index trades at vs the US.

Some of this can be chalked up to sector mix but my research indicates, its impact is overestimated.

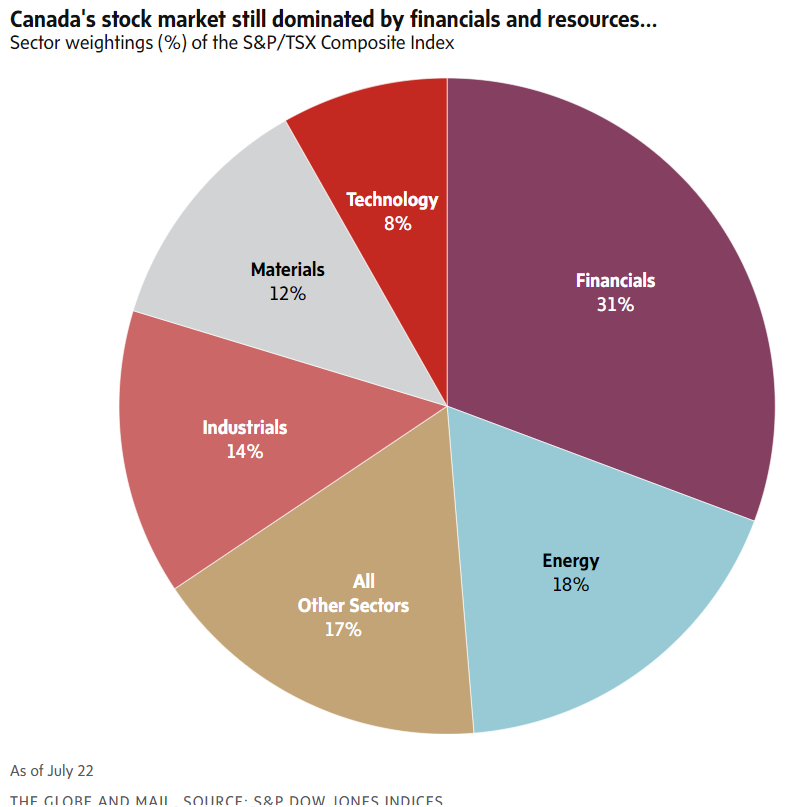

Shocking that, the TSX is 50% energy and financials.

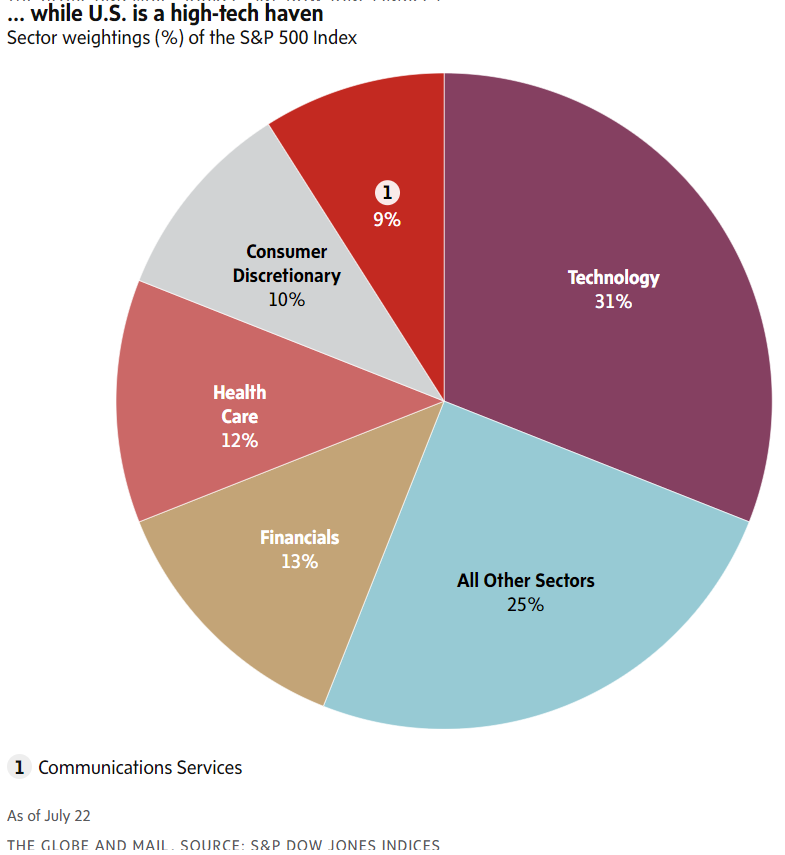

The US is better diversified and led by tech. These tech companies are global champions and deserve a premium wherever they are listed. Canada lacks the global champs.

Canada isn’t the only region with companies leaving to list for higher multiples in the US, Europe is experiencing the same thing.

It raises some interesting questions:

In an interconnected online world, will we observe more dynamics like those in the technology industry, where the market leader captures the majority of the spoils? Will more global companies list in the United States?

Are global investing frameworks less relevant when today’s champion companies are by default global?

Inflation in the 70s vs today. Market doesn’t think this is a possibility.

Market is pricing a 39% chance of a 50 bps cut two weeks from now. Could this be enough to cause the economy to reaccelerate? You can cherry pick data to reinforce a too hot or too cold economy. This post from Michael Kao lays out the argument on why a pivot is premature.

The Bank of Canada is expected to cut today. Thus far, cuts have down little to stimulate the economy but the Canadian economy was weaker relative to the US by the time they started cutting.

The goods-producing side of the economy is slowing. Excluding the pandemic, the ISM production index (44.8) hit its lowest level since April 2009. New orders declined for the fourth time in the last five months.

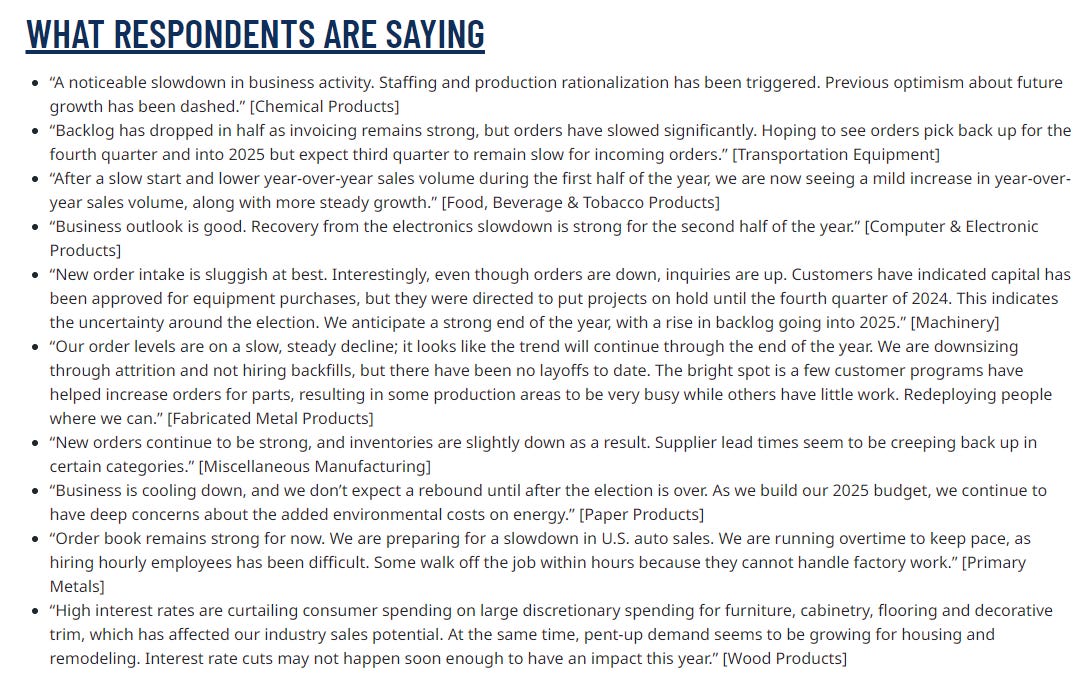

Respondents from ISM, echo similar themes as last weeks survey from Dallas Fed but it’s not everyone.

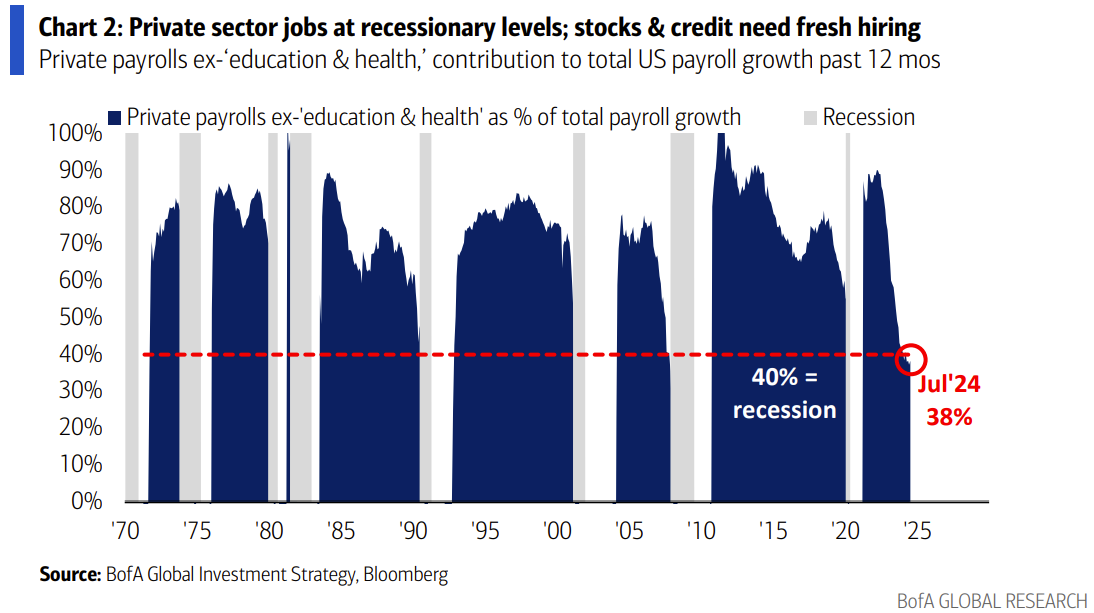

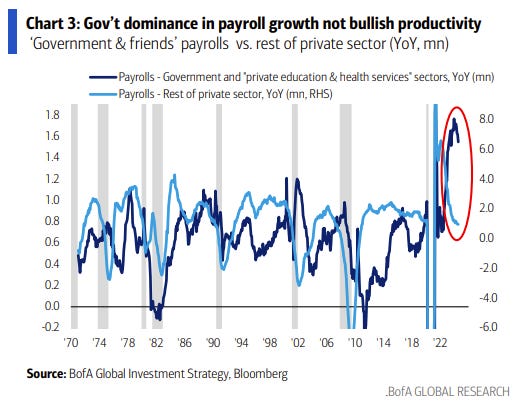

Public sector payrolls are dominating payroll growth, at levels normally associated with recessions.

As government payrolls grow, private sector lags.

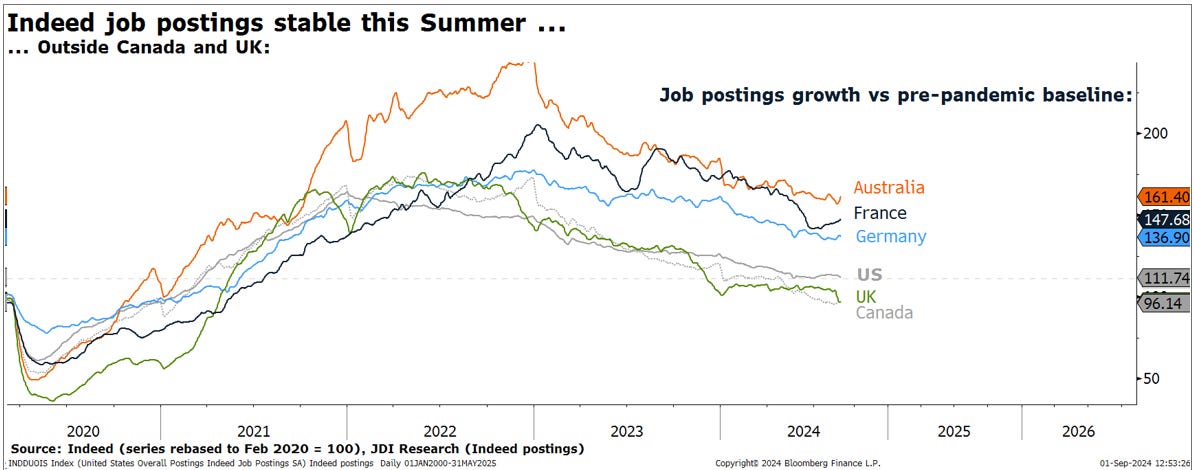

Canada and the UK now have less job postings on Indeed compared to pre-pandemic.

For now, large deficits keep the US labour market tight.