Is it Inflationary? & Chinese Stimulus 🐼

Is it Inflationary? & Chinese Stimulus 🐼

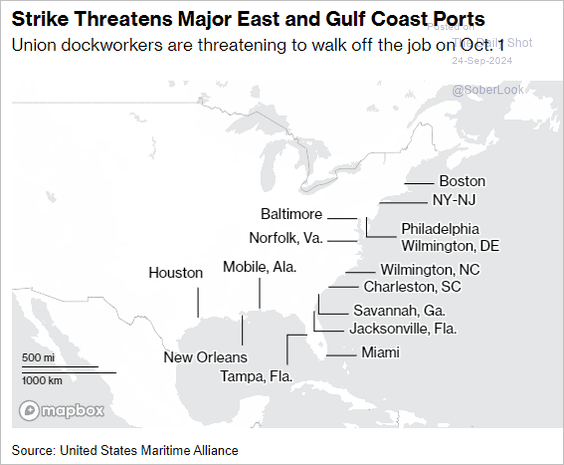

Around 45,000 dockworkers at major ports along the East and Gulf coasts are threatening to strike in October. A strike would shut down 36 ports that handle roughly half the nations’ cargo from ships. West Coast port workers got 32% over 6 years, setting the precedent.

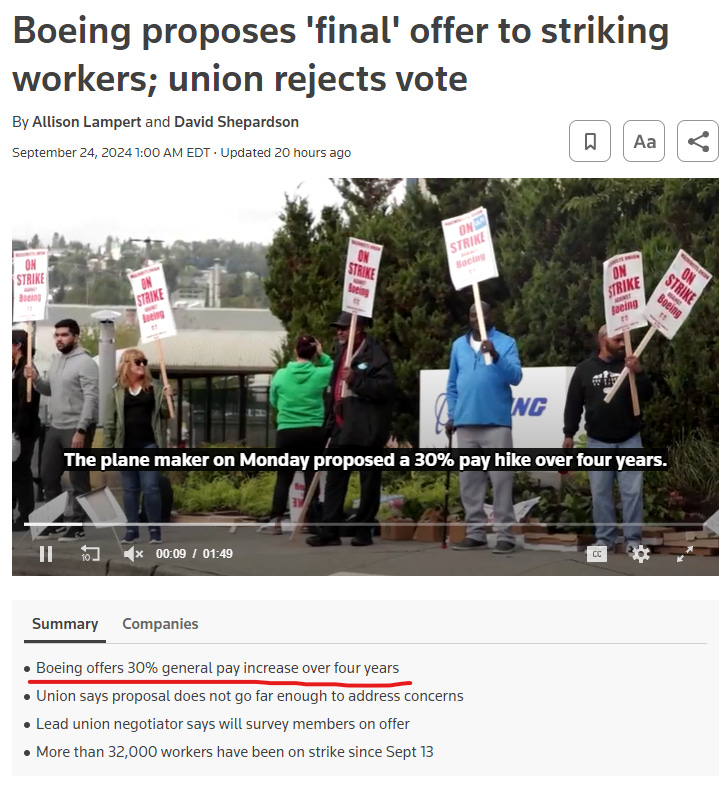

Yesterday, Boeing workers rejected a 30% pay hike over 4 years.

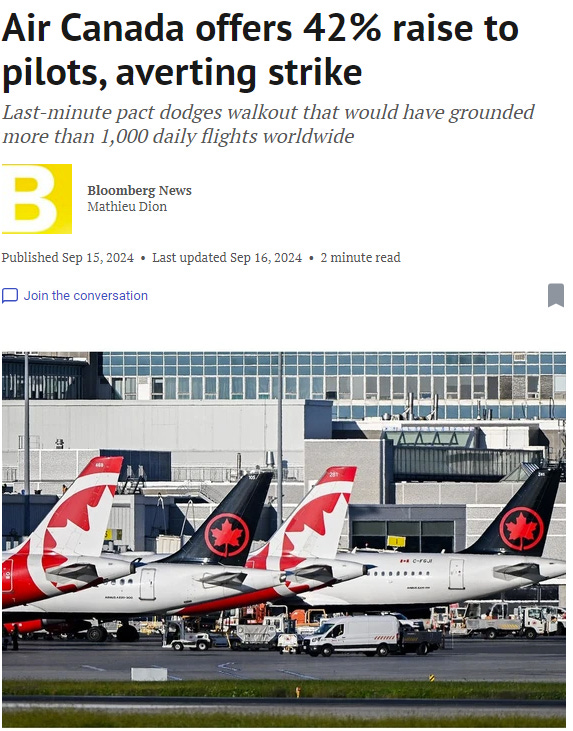

Last week, Air Canada pilots received a 42% pay hike over 4 years.

Good time to be in a union. Immigration in both Canada and the US should limit wage inflation on unskilled work and slack in the economy should limit white collar wage inflation. Nonetheless, these eye-watering wage increases will eventually flow into end user prices.

People’s Bank of China cut a key short-term interest rate, announced plans to reduce the amount of money banks must hold in reserve to the lowest level since at least 2018 and other measure, in an attempt to buoy the stock market, property sector and broader economy. This caused Chinese stocks to have their best day since 2020.

Aside from Chinese equities, commodities caught a bid on hopes of a recovering China and liquidity sensitive assets did well, such as Bitcoin and Gold hit another all time high. Central Banks around the world are definitively easing, a prime set-up for Gold and Bitcoin.

The stimulus is an effort to boost Chinese domestic consumption that has been steadily slowing.

The major problem weighing on the broader economy and consumers is the property sector. There is now more housing inventory unsold than the global financial crisis.

Chinese growth never recovered to its pre covid trend.

Investors have left China for dead and have rotated into other emerging market economies.

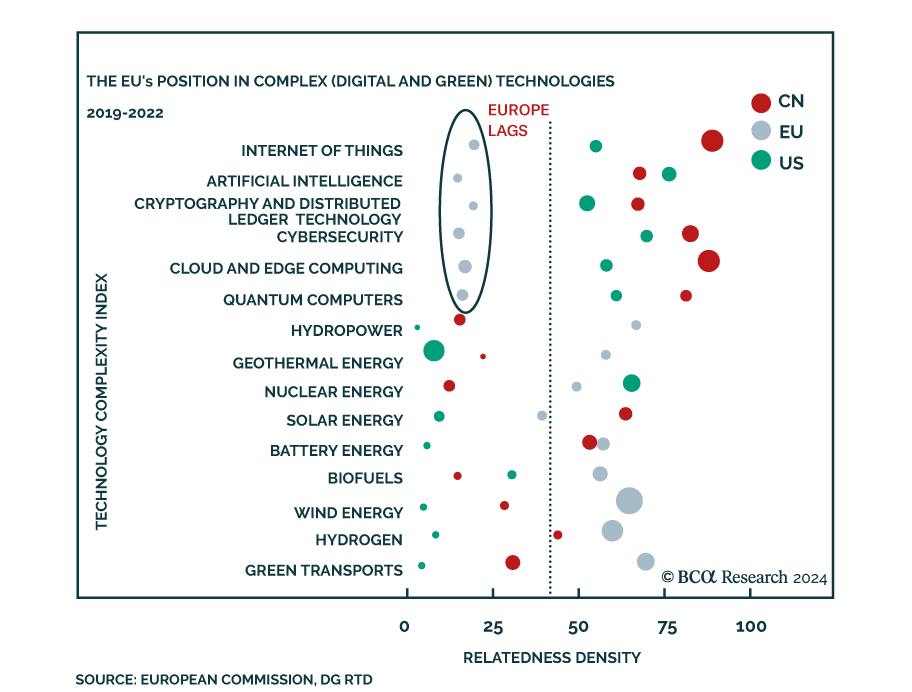

Europe is lagging both China and the US in important technologies. The regulatory first approach is slowing innovation and leaving the continent behind. Europe is more focused on green energy.

Private equity’s annualised IRR fell below 10 per cent in the year to March 2024, says PitchBook. Additionally, DPIs, look terrible. Funds in the 2019-2022 vintage have disbursed about 15 cents on the dollar so far, according to a Goldman Sachs analysis on Preqin numbers. At the same juncture, previous vintages had returned well over half the money invested. It will be interesting to monitor how these vintages finish. With no Private Equity outperformance, it is difficult to justify the lock-up.

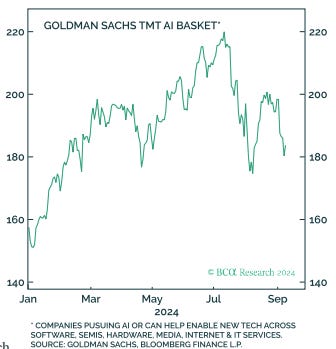

AI stocks seem to be losing their luster.

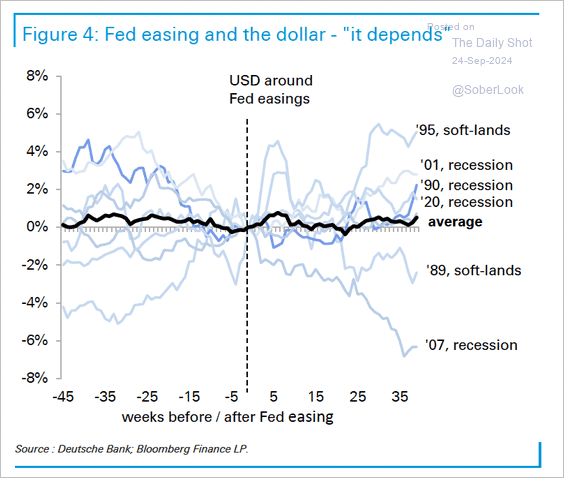

My first reaction to the Fed easing was that it would hurt the dollar but with other Central Banks easing and other economies struggling more than the US’, it isn’t clear.

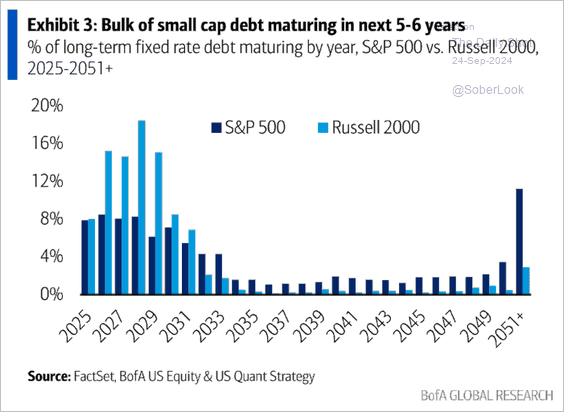

Small caps will benefit more from an easing cycle, as it relieves some of the pressure from the upcoming maturity wall.