Multi-Managers & Manufacturing

The Atlanta Fed's sticky-price CPI rose 3.5% MoM on an annualized basis in August, following a 3.2% increase in July. On a YoY basis, the series is up 4.1%. Why are we rushing to cut rates? This probably takes 50 bps off the table next week.

There are limited recession fears globally, again why rush to cut.

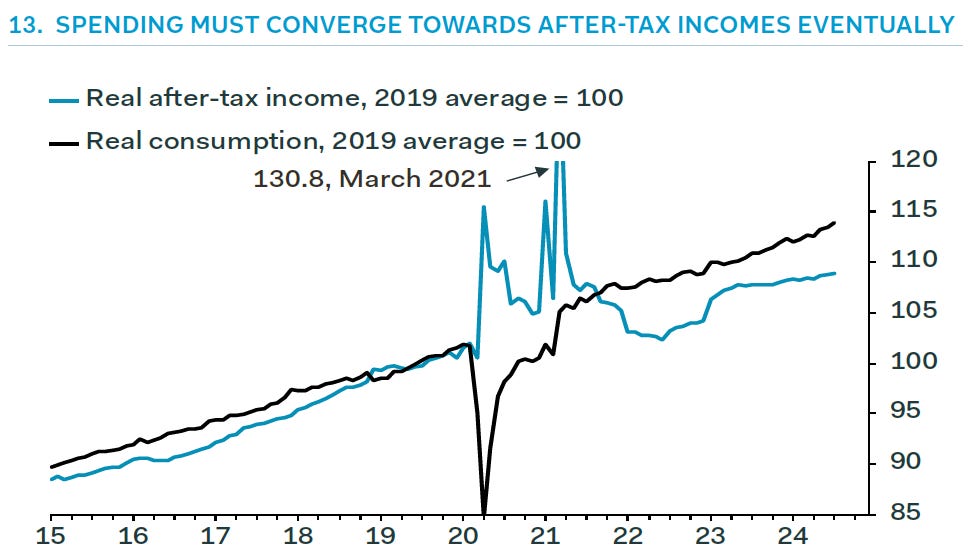

Eventually, consumption needs to converge with after-tax income, until then, people will continue spending above their means.

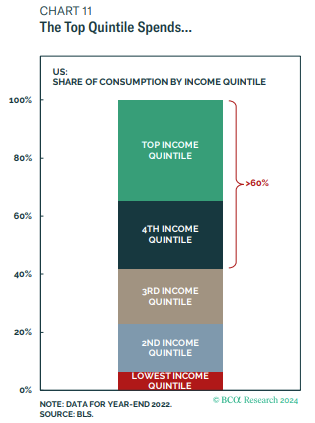

Wealthy households are responsible for the majority of consumption in the US. The economy can continue humming along, even as bottom quintile income earners struggle to get by.

Another way to look at it, the bottom quintile of income earners is only responsible for 10% of consumption and earns 7% of total income.

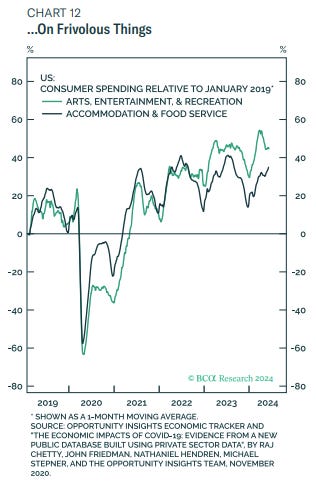

People are still spending money on discretionary activities.

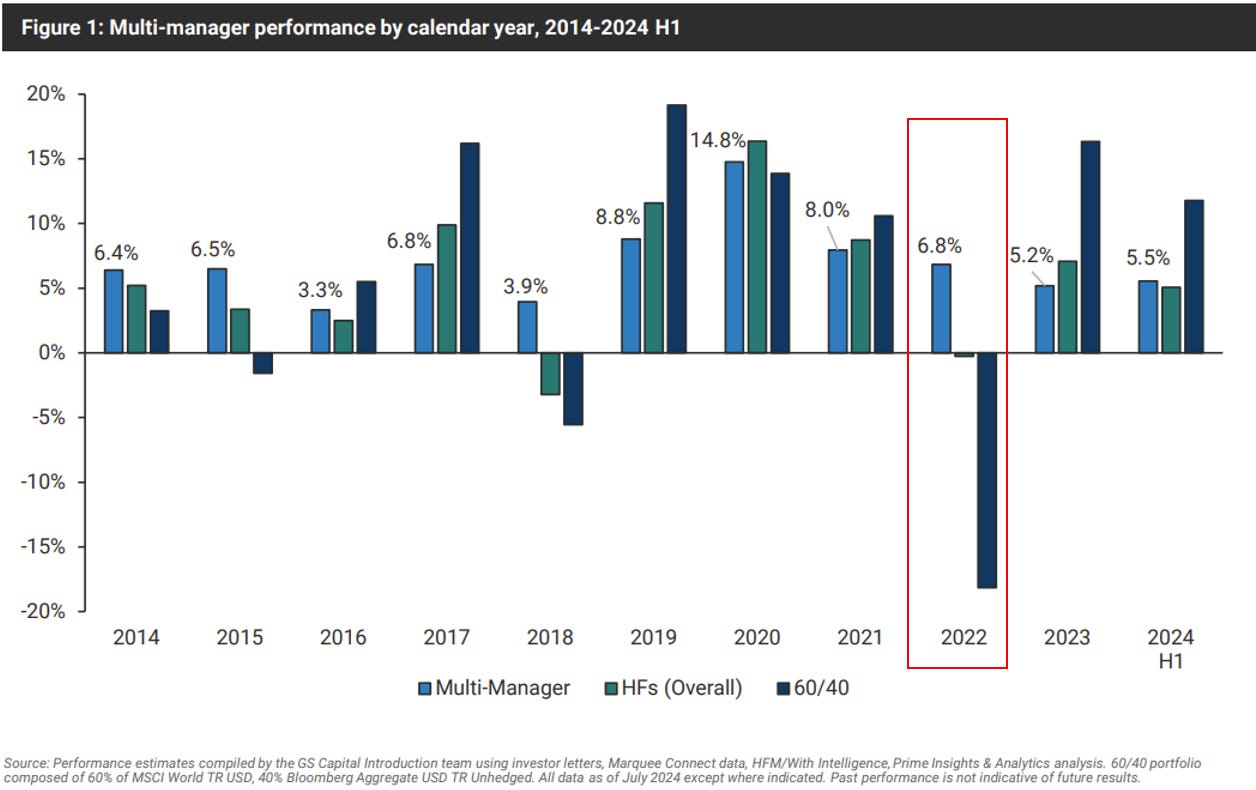

Multi-Manager hedge funds (Citadel, Millenium, etc.) became all the rage in 2022 when equities, bonds and the majority of other asset classes sold off with rising rates but Multi-Managers continued to deliver stable, consistent returns. Multi-Managers were one of the only asset classes where institutions could put hundreds of millions to work and should continue to work in rising rate environment.

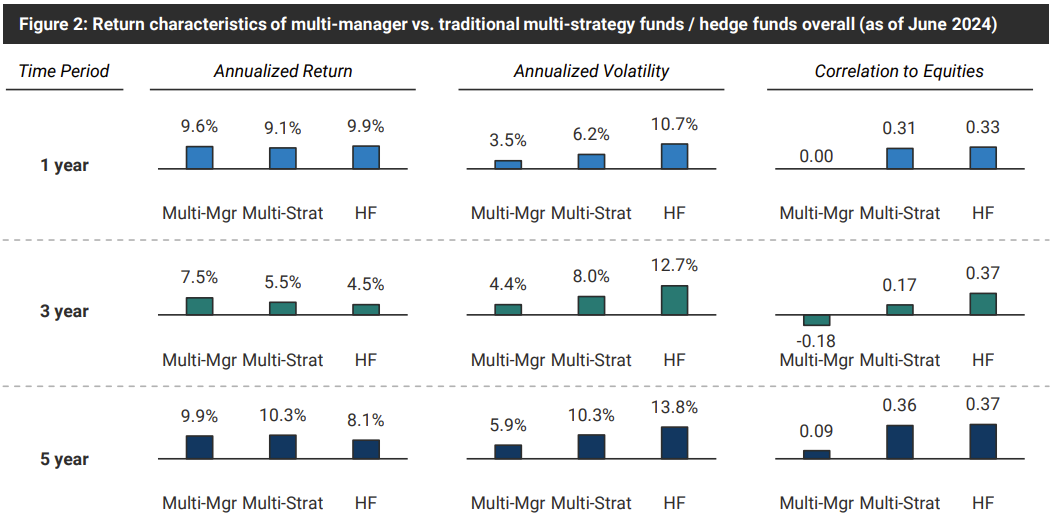

Multi-Managers have consistently delivered attractive, low vol returns of 1, 3 and 5 year time horizons. What makes these hedge funds unique is that they are market neutral, meaning they have correlations with other asset classes of close to 0; the ultimate diversifier. However, after all expenses you could be paying upwards of 4% and 40% of performance to these funds.

Many hedge funds are correlated to markets and end up being expensive beta and levered beta, leading to underperformance.

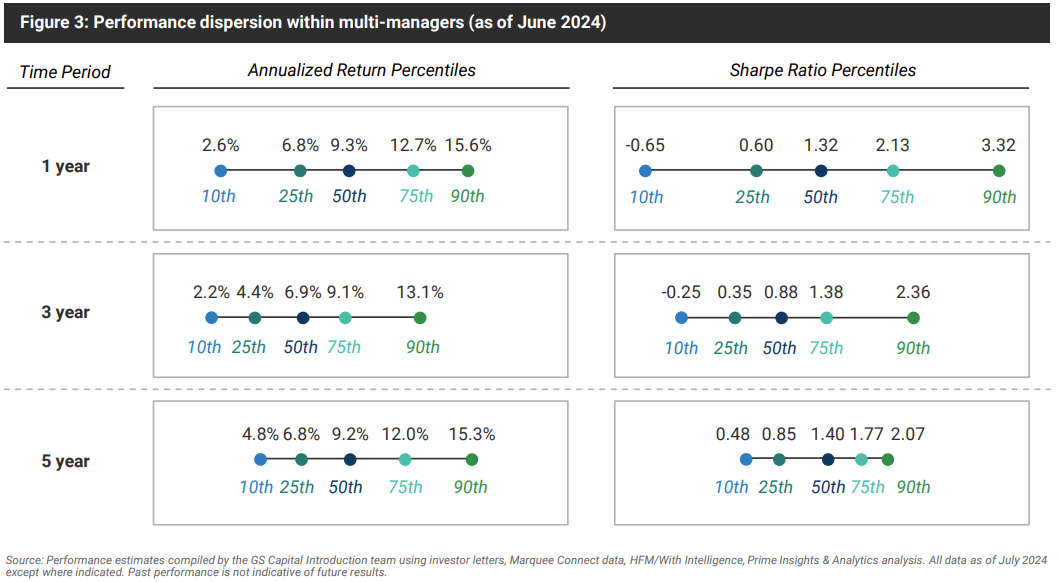

In the top quartile, double digit returns with an almost 2 sharpe, dominated most asset classes on a risk adjusted basis.

I read a paper, backward looking over the past 30 years, the optimal portfolio was private equity (highest returning) and hedge funds (highest sharpe).

2024 is the first year to see outflows across Multi-Managers. This is because as they raised billions, they were able to push terms on to allocators such as longer lock-up and the bill for more expenses.

Have we hit peak Multi-Manager?

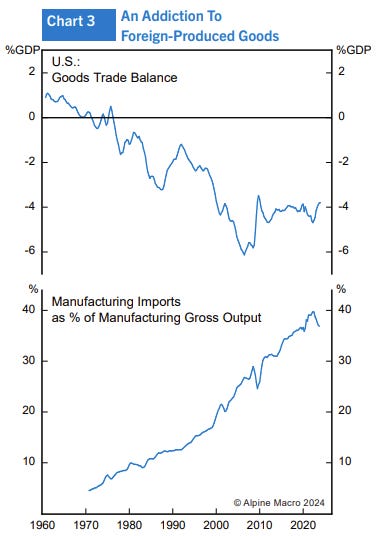

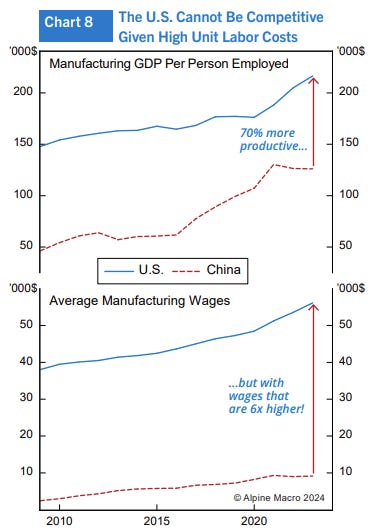

The US is highly dependant on foreign goods and as tensions rise, you’re better off being self sufficient.

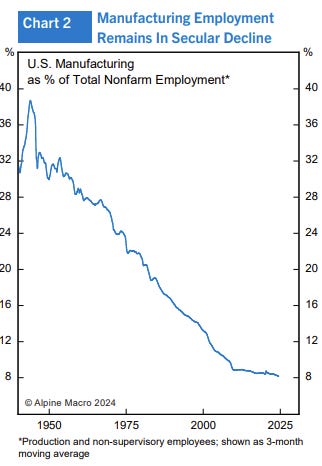

Manufacturing employment in the US went from almost 40% of all employment at the end of WWII to 8% today. This has been part of the hollowing out of the middle class.

The issue with the reshoring narrative is that while US manufacturing workers are 70% more productive than Chinese workers, wages are 6x higher. Reshoring likely involves significant automation. It would still be in North America’s interest to rebuild the manufacturing base.

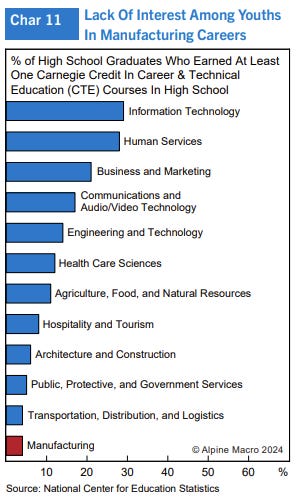

Working at a factory isn’t viewed as a prestigious career and therefore there is limited interest from young people.