Multiples Matter?

Apple event yesterday, the iPhone 16 looks like the iPhone 15. These events have become less relevant over time. Upgrade rates over 15 years, below. Apple bulls hope that the incorporation of AI in new models will drive more upgrades. Based on my usage of Siri, maybe a stretch.

September is the seasonally weakest month for the S&P 500.

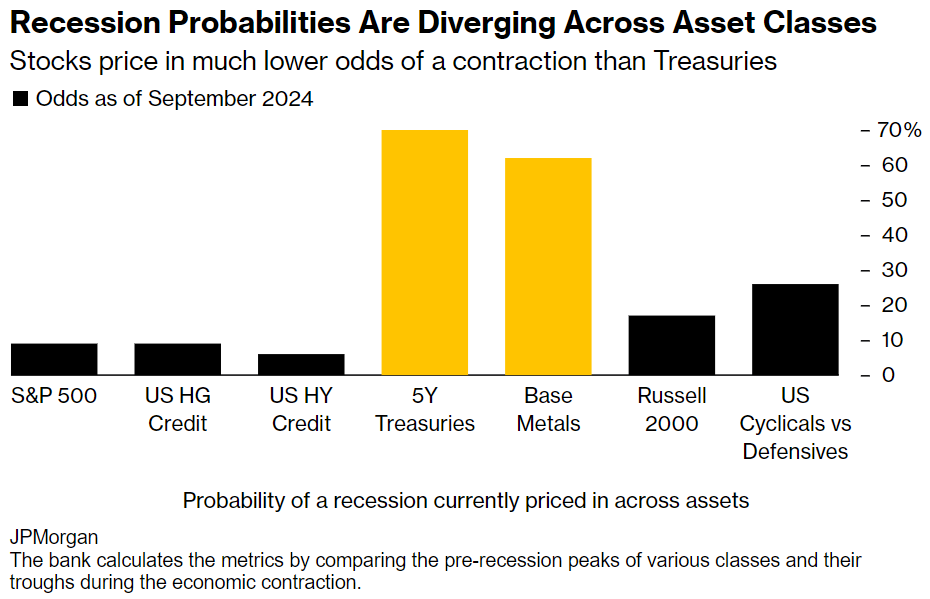

We remain in a regime where different markets are pricing in very different outcomes. S&P 500 at all time highs, credit spreads are tight but yield curve pricing cuts and commodities are depressed.

Credit spreads not flashing any signs of concern. Ahead of a recession, you’d expect spreads to begin widening.

The labour market does not give warning and is rather confirmation of a recession. The labour market historically, sheds jobs as the recession starts.

Over the past year, US markets have been driven by multiple expansion and earnings growth. Asia has seen contracting multiples.

Verdad had a good piece on multiples. This has been a pain trade for subscribers of the philosophy that multiples matter. Valuation sensitive investors were underweight US markets because they’ve been viewed as expensive for the better part of 2.5 decades. One of the reasons they’ve continued to outperform is earnings growth.

As American earnings growth has outpaced international peers over the past 15 years, US stocks have returned 13.4% annualized, more than doubling the 5.9% annualized return of developed international stocks.

But with more than a quarter of total US market capitalization being attributable to just six technology stocks today, it’s worth questioning whether hyper-concentration in yesterday’s winners will be a winning strategy in the years ahead.

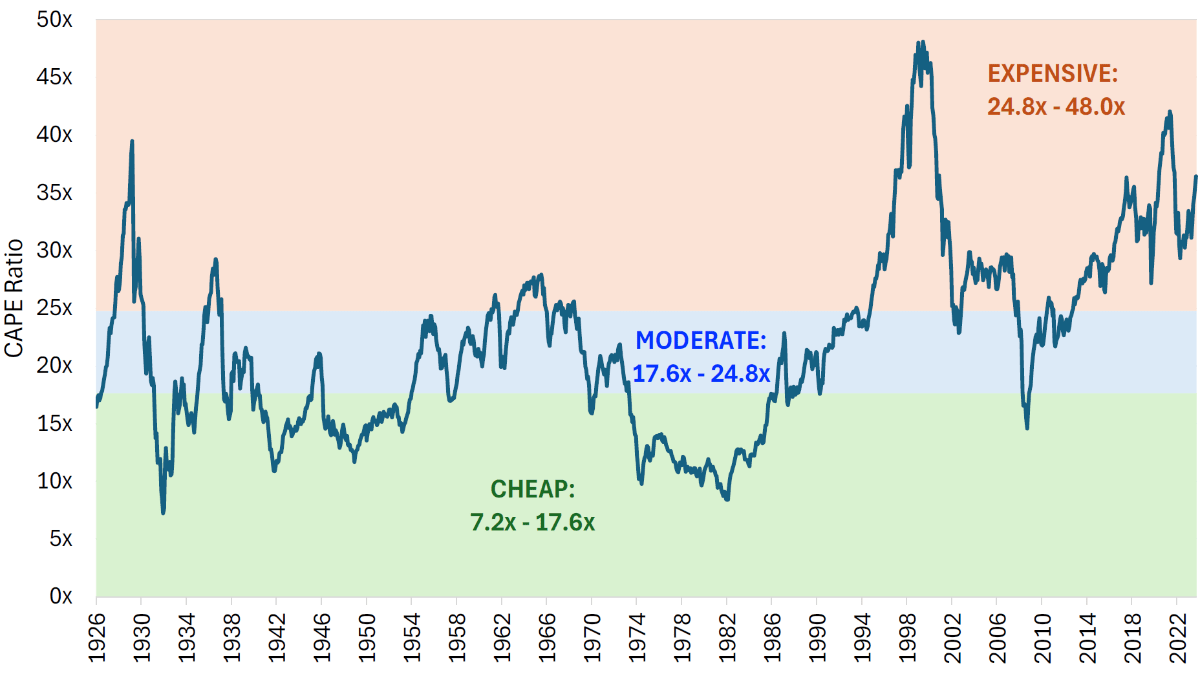

To start, it’s worth noting that the US stock market’s magnificent run over the past 15 years has resulted in a cyclically adjusted PE ratio (CAPE) of 36x today, a valuation level that is firmly within expensive territory by historical standards. In the figure below, we grouped historical values of the United States’ CAPE ratio into three categories with an equal number of monthly observations.

Figure 1: United States CAPE Ratio (1926–2024)

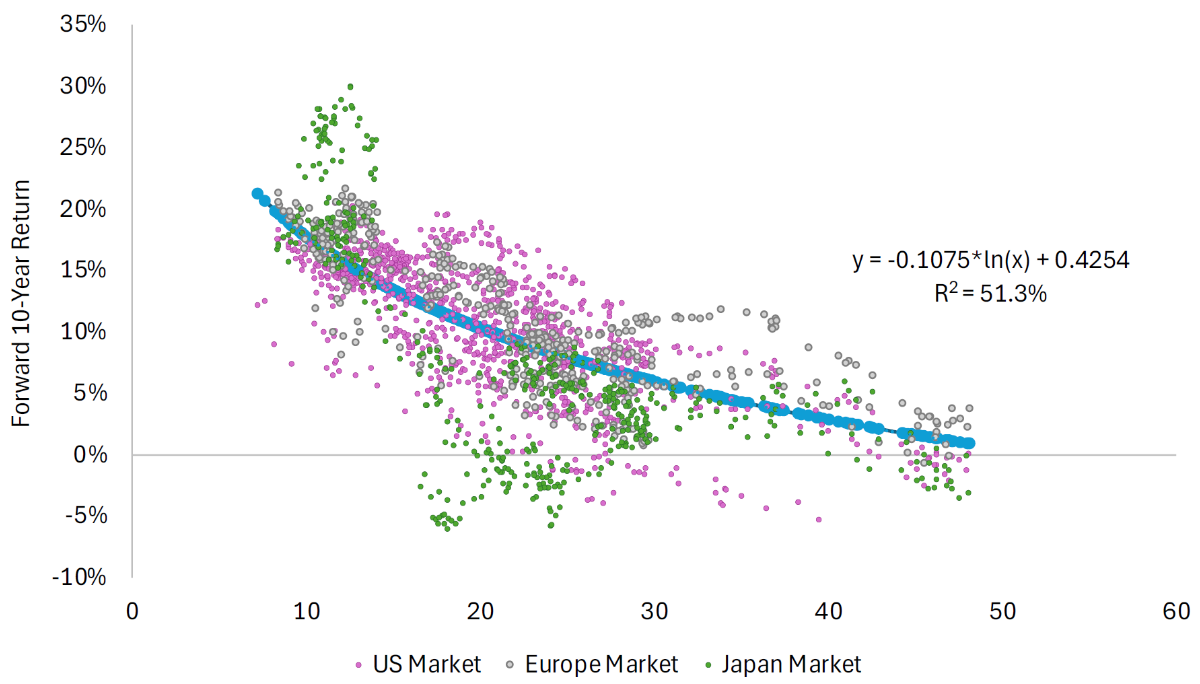

Below you see the relationship that gave investors pause. Higher multiples tend to lead to lower forward 10Y returns. Intuitively, this relationship makes sense but has left investors underweight the best performing market.

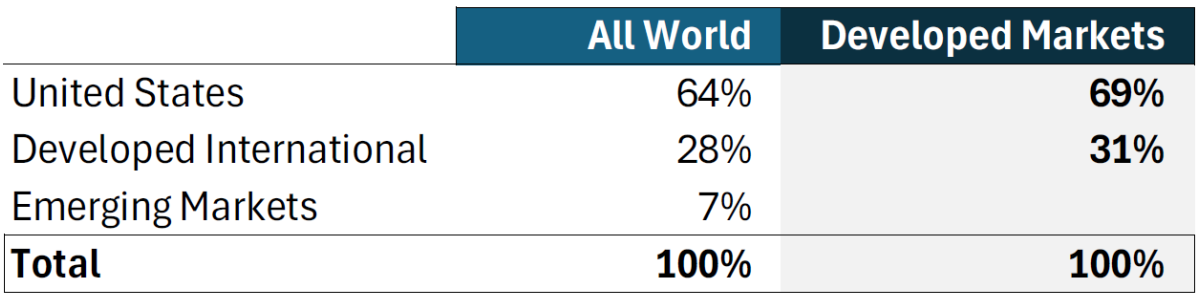

In addition to lowering expected returns, the expensive valuations in the US may also increase idiosyncratic risk in a portfolio through hyper-concentration in the biggest winners of the past decade. Consider a seemingly diversified index like the ACWI benchmark, which contains more than 2,750 large- and mid-cap stocks from around the world. This global index mechanically allocates two-thirds of capital to the United States, and within its developed market allocation, the United States has a weighting of almost 70%.

Figure 3: MSCI ACWI Allocations (June 30, 2024)

Valuation sensitive investors are forced to look at other geographies and overlook concerns that Europe might be turning into an open air museum.

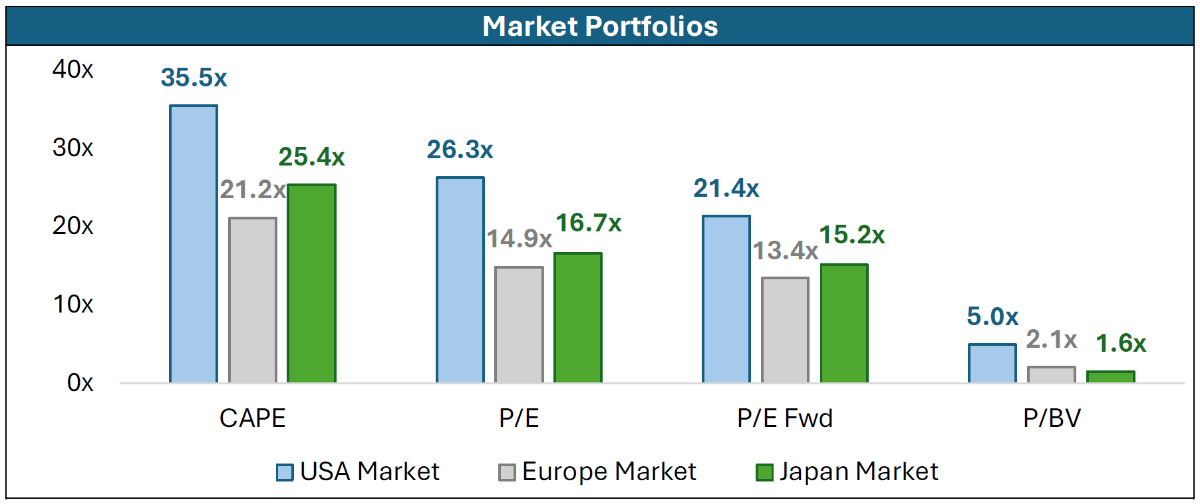

While the US market trades at an expensive valuation of 36x CAPE today, international markets are more moderately priced, with the European market trading at 21x CAPE and the Japanese market valued at 25x CAPE as of June 30, 2024. As a forward-looking measure, the CAPE ratio has a negative relationship with expected returns, as shown in the figure below, with higher CAPE valuations being associated with lower returns over the next decade.

Figure 5: Global Valuations (July 2024)

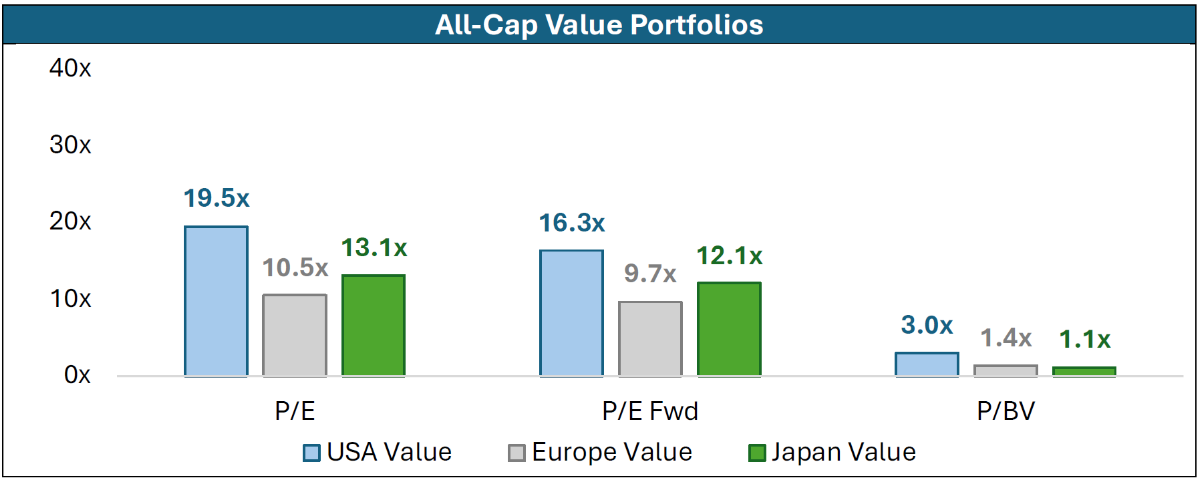

Expanding to include the entire universe of listed securities in various regions, the US remains the most expensive.

The theory goes, over the long run the narratives depressing multiples in various geographies will subside and new narratives will emerge. Over the long run, this should lead multiples to mean revert and investors can capture the returns from multiple normalization.

China is the poster child for this. A Taiwan invasion, peaking demographics and a recession have caused the MSCI China to trade at 40% of the S&P 500 multiple. Can US relations normalize and China’s growth return or is it a Russia 2.0/a falling knife?

That was a fun read. Thanks Andrew!

Also, Price/Book is lame... ha