Secondaries & Chips

Some interesting research on the secondary market from PEFOX.

The Chart above shows the discount to NAV of a group of over 15 listed private equity funds. This can be used as a proxy to get an understanding of real time valuations. For listed PE funds, they persistently tarde at a discount in the range of 75-80% of NAV. A discount is required to exchange long-term assets for short-term liquidity. These marks have stabilized in the past few years.

Pricing for private equity secondaries was largely flat over the last quarter, rising only fractionally higher to reach an average level of 89.8% on Q1 2024 NAV. Market conditions are healthy, with liquidity being provided by a wide swathe of well-capitalised buyers. The strength of the equity markets this year (e.g. S&P 500 up over 19% year to date) has had a pervasive influence, spreading confidence amongst buyers.

We also note the increased activity of Evergreen funds, which has acted to shake up the market. Hardly a day goes by without news of another Evergreen fund being launched. The retail nature of their investor base means they are typically well-positioned to be the best buyer in auction processes for brand name assets. The choice for traditional buyers is either to beat them on pricing or lose out.

Of funds that have already reported Q2 2024 NAVs, including those managed by leading firms such as Apollo, Ares, Blackstone, Carlyle, EQT, and KKR, indicates NAVs will be written up around 2.4% compared to Q1 2024 on average. Such is the level of demand we see right now, we have little doubt pricing on Q2 2024 NAV will at least match Q1, meaning that buyers will bear the brunt of pricing on this more expensive NAV.

Discounts on secondaries can differ widely across asset classes.

How have these secondaries funds performed as investments?

This is a 2015 vintage secondaries fund with aggregate commitments of $10.1bn. The current remaining NAV is over $5.5bn and this is broadly diversified across hundreds of underlying LP stakes acquired through secondary transactions.

The additional wait will, of course, act as a major drag on returns. Just looking at the two year period Q1 2022 to Q1 2024, the drag effect is significant: LCP VIII has gone from a 1.74x net multiple and 19.5% net IRR to a 1.67x net and a 15.2% net IRR. Over the same period, Strategic Partners VI’s cash multiple has fallen from 1.56x to 1.51x and it’s IRR from 15.4% to 13.7%. If this continues in the same fashion for a few more years, what was once a good investment will start to look decidedly mediocre or even poor.

The Lexington fund is not the only fund in this vintage to plateau. Since 2015, secondaries have only gotten more competitive and performance could disappoint after high IRRs early in these fund lives due to purchasing at a discount.

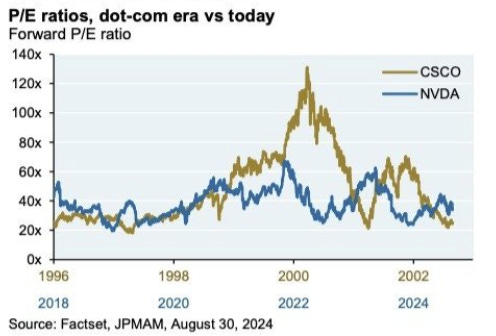

Nvidia has been the Taylor Swift of the investment world this year. Relative to the size of US GDP, Nvidia looks like a bigger bubble than Cisco in 2000.

But Nvidia’s valuation is far less extended than Cisco at the peak. Have to hope you aren’t buying at peak earnings

The US is trying to reverse the offshoring of the semiconductor industry. The US regrets giving up this industry.

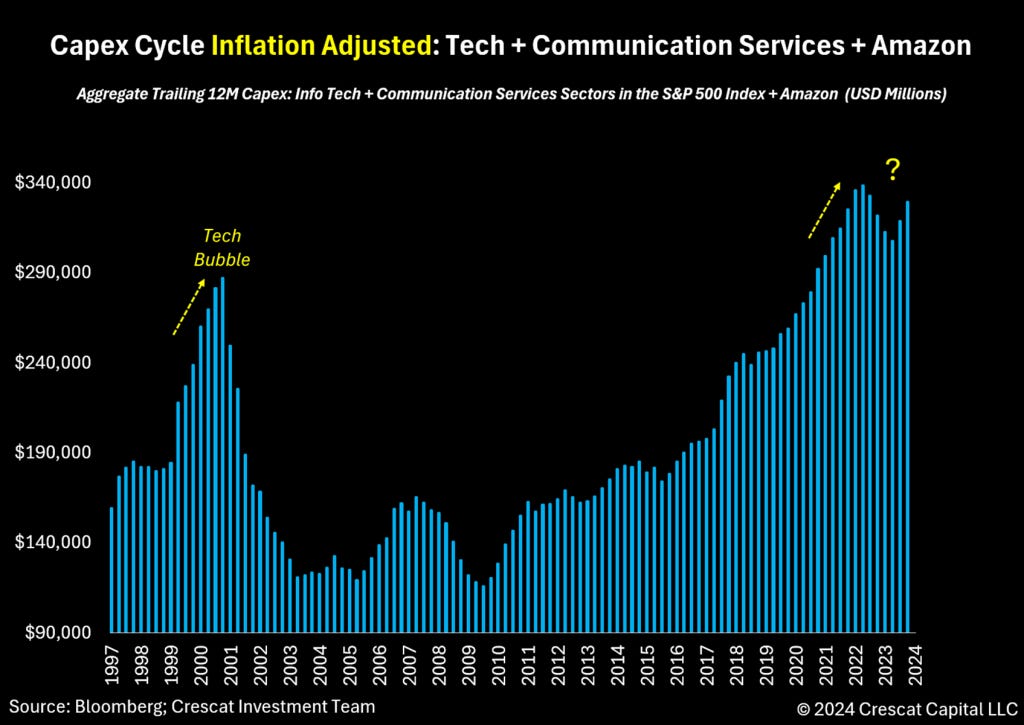

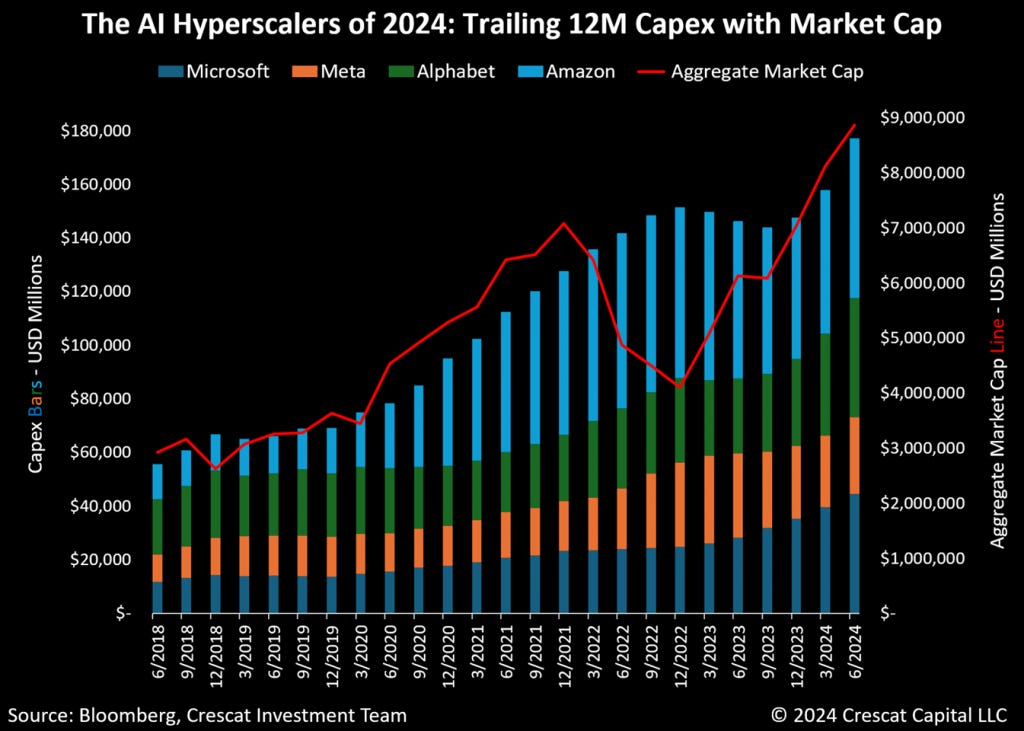

It would be natural to expect the capex investments from the US giants to be cyclical and begin to roll over but maybe AI is bigger than we think.

The hyperscalers continue to bet their futures on God like AI. Can’t get left behind.

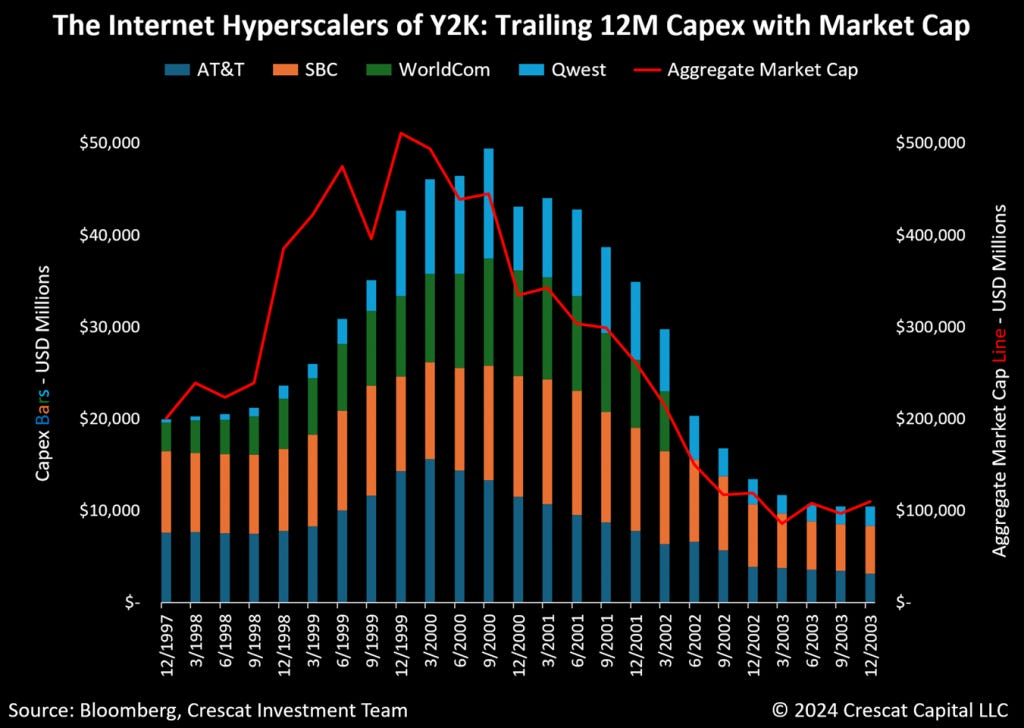

A similar thing happened in the dotcom bubble, eventually internet profits couldn’t justify continued capex spend.

It’s not uncommon for technologies to take decades to reach the mainstream. Experts predict this time will be different with AI.

Software, as developers are replaced by co-pilots is expected to receive the biggest boost from AI adoption.