The Time has Come ✂️

Interesting thought from our macro hedge fund manager.

AI and generative AI represent the commoditization of knowledge and intelligence. This means the added value of knowledge and earning power of intelligence will drastically decline. Why are doctors paid more than cleaners? Because of their expertise, years of study, and their ability to apply knowledge to make conclusions and help their patients. AI will eliminate or at least narrow this gap. So, readers beware that soon all our jobs will face competition from AI including doctors, coders, lawyers and traders – not just drivers being replaced by robot taxis. One of the few areas I believe will not be challenged by AI is sports, as nobody will be interested in watching humans compete against robots. Just as no one today is interested in chess players competing with machines, the appeal lies in human vs. human.

The dispersion of the impact of covid across developed world economies is surprisingly wide. The US had the best growth. Japan the lowest levels of inflation. Japan, UK and Germany all had worse growth than Canada, Italy and France but unemployment levels are higher in these countries.

Market is pricing 50 bps of cuts tomorrow, economists are calling for 25 bps. I’ll call 50 since Powell has surprised to the dovish side over the past year. I don’t think it really matters, I don’t think either are enough to immediately stimulate the economy. The Fed should err on the side of caution and should prefer to overtighten rather than see inflation reemerge. Another round of inflation is the distratrous scenario for the economy and markets. At the end of the day, the economy is extremely complex and no one knows the right answer to the decision being made later today.

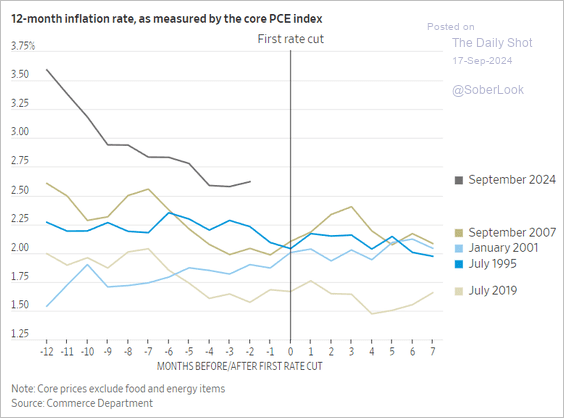

Inflation is low enough, giving enough cloud cover for the cuts.

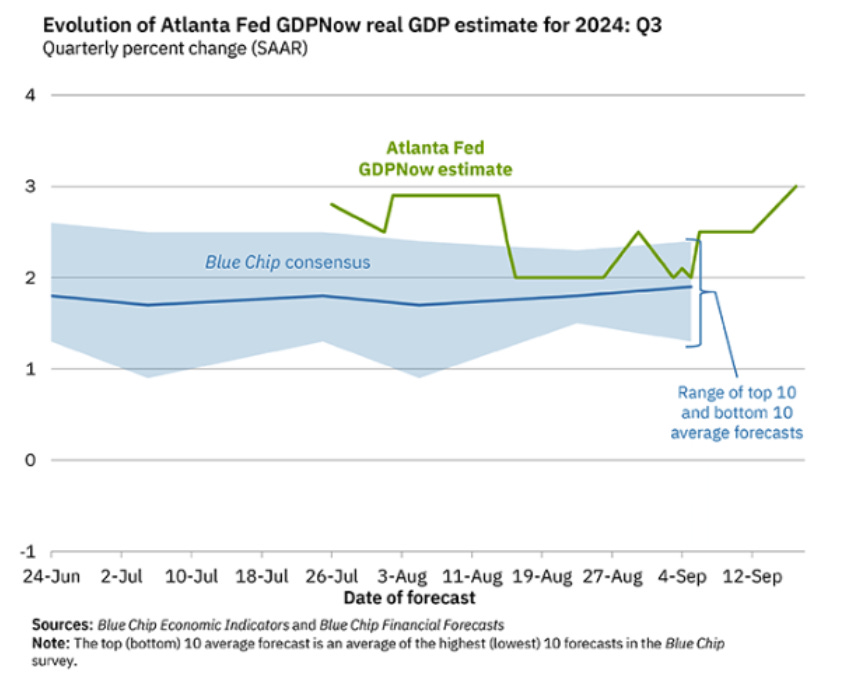

Atlanta FED GPDNow forecast projecting 3% real growth in Q3, up from 2.5% last week. This doesn’t seem like an economy that desperately needs cuts.

GDP estimates are primarily being driven by healthy consumption.

But you don’t have to look far for signs of weakness. Room rates in Las Vegas are declining in another sign of softness.

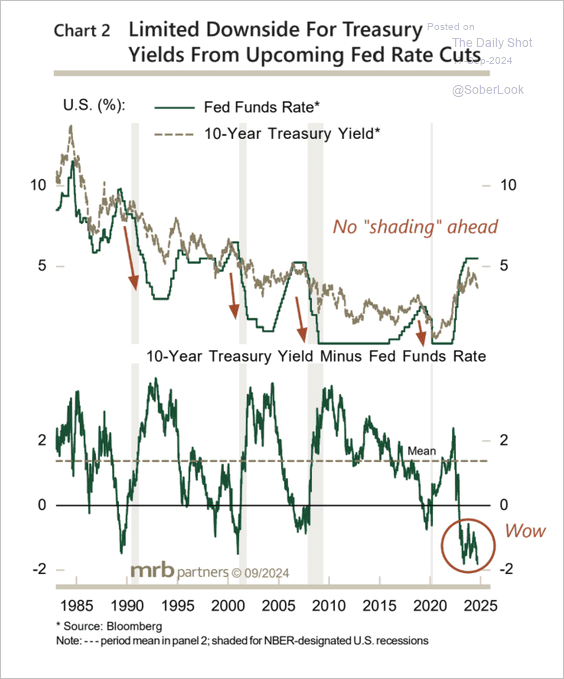

Despite the strong GDP and other indicators holding up. The bond market is definitively calling for economic weakness, as measured by the spread between the Fed Funds Rate and 10Y yield being at its lowest point in over 40 years. The spread between the Fed Funds Rate and 2Y is indicating something similar.

The cuts the bond market are pricing in, look more like a recession is on the horizon rather than a soft landing.

The consensus view across fund managers is that monetary policy is the most restrictive since 2008. The only other times policy was viewed to be this tight was around previous crises.

But the majority of fund managers do not expect a recession.

The direction of the equity market isn’t clear after the start of the cutting cycle. It is dependant on whether a recession is near and that isn’t clear.

Another way to look at it.

We are in the seasonally weakest period of the year for the S&P 500.

Canada's August inflation rate falls to 2%, the lowest since March 2021, and equal to the BoC's target. The war seems over but prices are up 18.3% since Jan 2020.

Fund managers still hate commodities.

Great reminder about where we are in the inflation cycle since 2020. 2% sounds great until you compare it to 2020.