You Get a Tariff!

Investors who bought last weeks dip were rewarded with the best week of the year for US stocks. US inflation came in line with expectations, traders continue to flip flop about the magnitude of Fed cuts this week. Tech had a monster week.

First Presidential debate, Harris was viewed to have won but, the race is still too close to call. Another, attempt to shoot Trump over the weekend and we are still 2 months out.

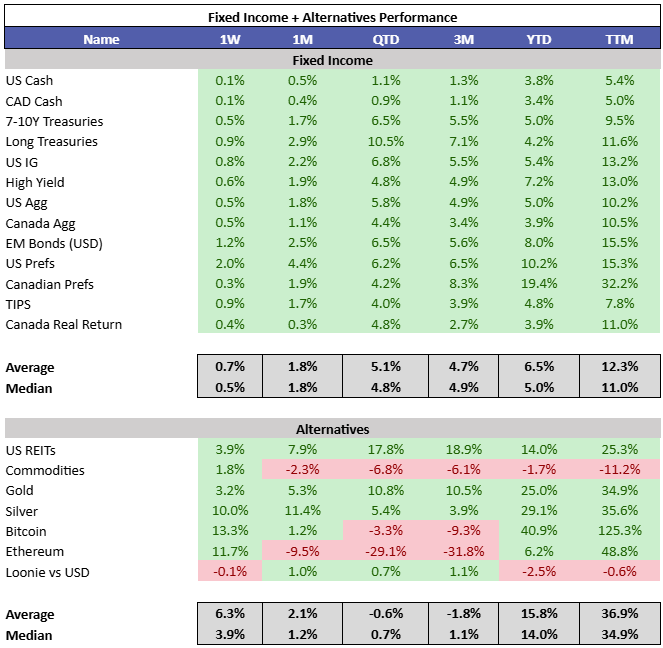

Yields were down 6 bps in the US and Canada, solid week across fixed income. Commodities, precious metals and crypto all performed well.

Last week was the best week of the year for the S&P 500. Weekly moves have gotten larger into September.

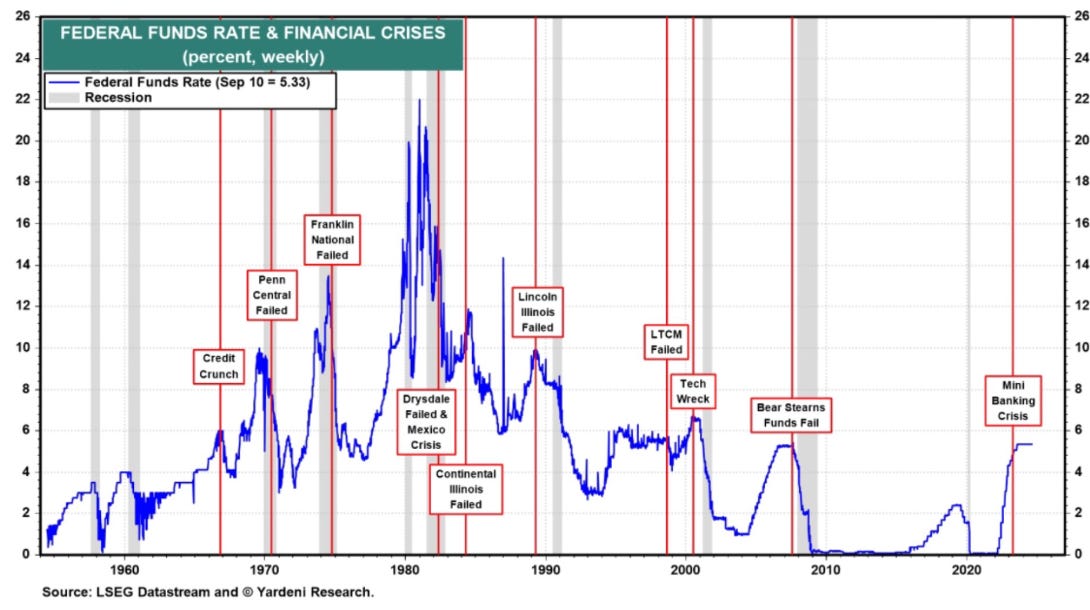

25 or 50 bps from the Fed this week? I don’t think it matters, long and variable lags mean the next 12-24 months are baked. Additionally, 25 or 50 bps isn’t going to move the needle.

A Fed easing cycle usually always starts when the Fed expects a soft-landing, only for them to eventually realise the economy is diving into recession and the wheels fall off the financial sector.

Still lots of signs that the economy is holding up.

I bet, if you polled equity investors there would be many who couldn’t fathom a lost decade. Long drawdowns are more common than you think.

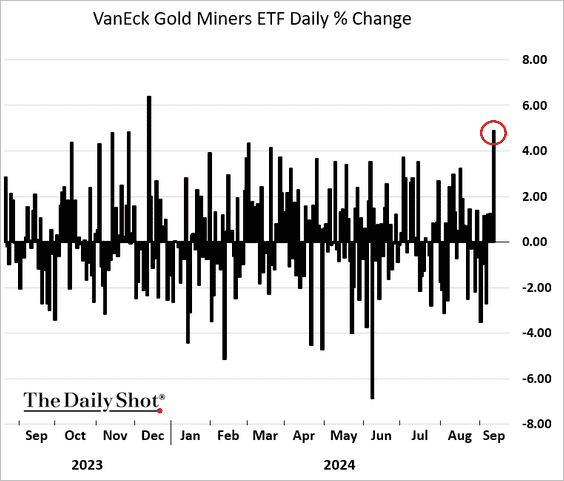

Last week, the gold miner ETF posted its best day of the year.

Recent Venture Capital vintages are experiencing a longer J-curve, starting out negative. If you are invested in a fund that has found a generational company, you will be fine.

I wonder if early underperformance is predictive of the funds ultimate performance.

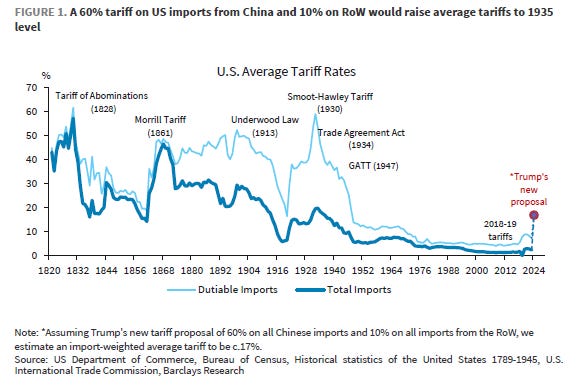

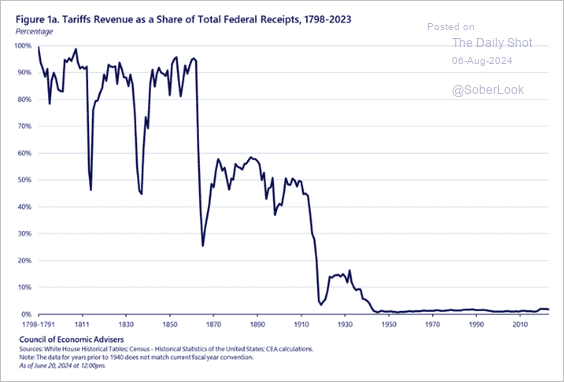

One of Trump’s flagship policy proposals is more tariffs in an attempt to reindustrialize parts of America. Tariffs were fairly normal prior to WWII.

In the early 1900s, half of the Government was funded by tariffs.

Palmer Luckey recently discussed the US rembracing tariffs (link). Yes, he is talking his book but he makes some valid points. You don’t want to be reliant on adversaries for critical manufacturing. This discussion is relevant to the car companies today, as China is leading EV manufacturing and design. North America has taken the stance of slapping high tariffs on Chinese EVs. You need to still figure out how to limit complacency if you are going to protect domestic industry.

It’s clear the West regrets letting China hollow out their manufacturing capabilities.

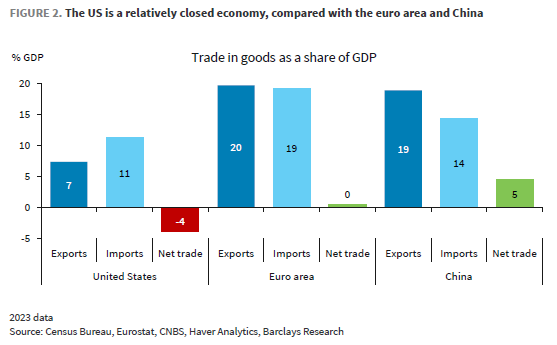

Surprisingly, the US is a relatively closed economy compared to Europe and China.

It’s not a free lunch. Tariffs are expected to be inflationary and detract from GDP. This is the cost of moving away from the lowest cost producer.

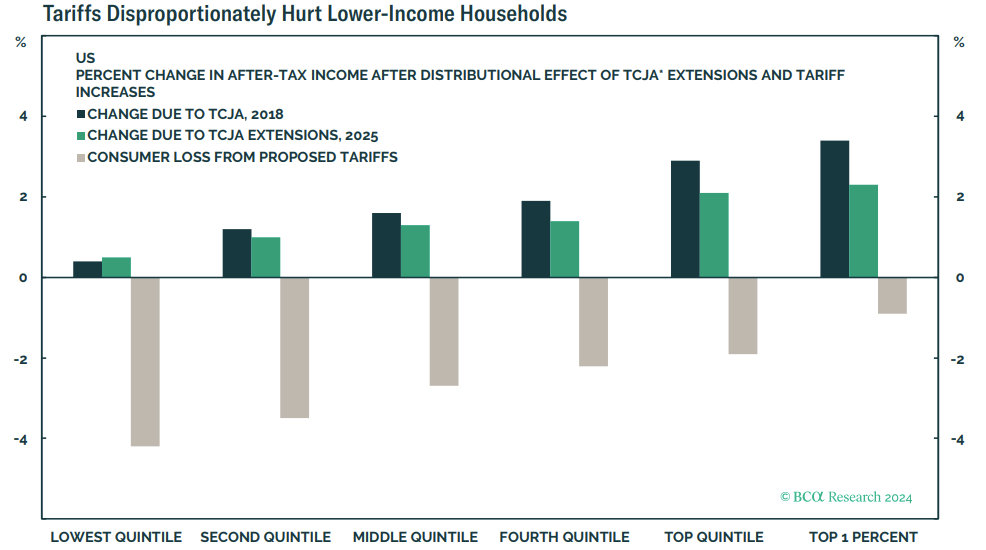

Tariffs are also regressive, they will impact the poorest consumers the most. The hope is longer term, they repatriate manufacturing jobs that help rebuild the middle class.