A Fiscal Disaster

Apollo did a piece on the budget, Treasury demand and the yield curve (Full Presentation). I hardly got past the first section because it gives some context to this unbelievable move in gold over the past 6 months. Nonetheless, below are Apollo’s takeaways:

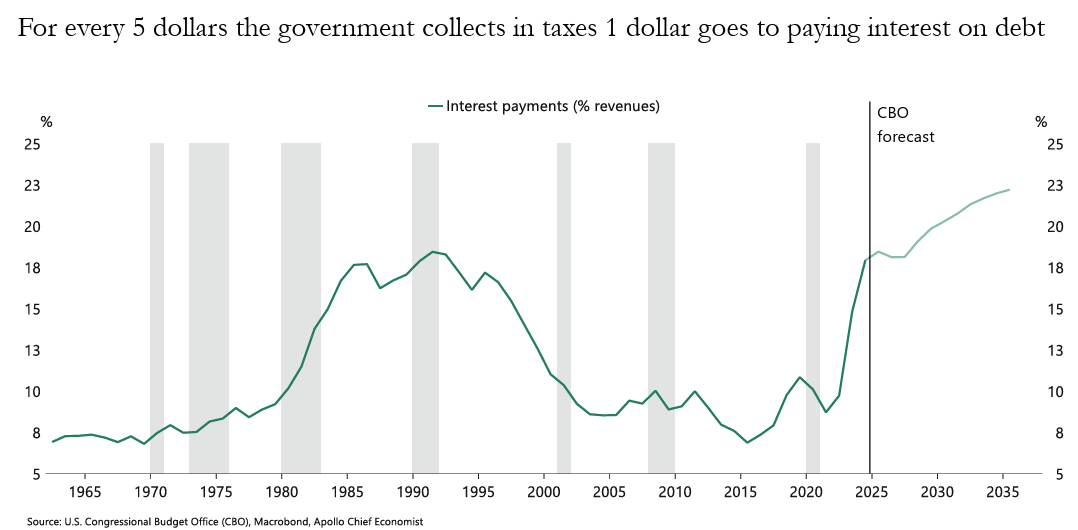

1. For every $5 the government collects in taxes, a dollar goes to paying interest on debt.

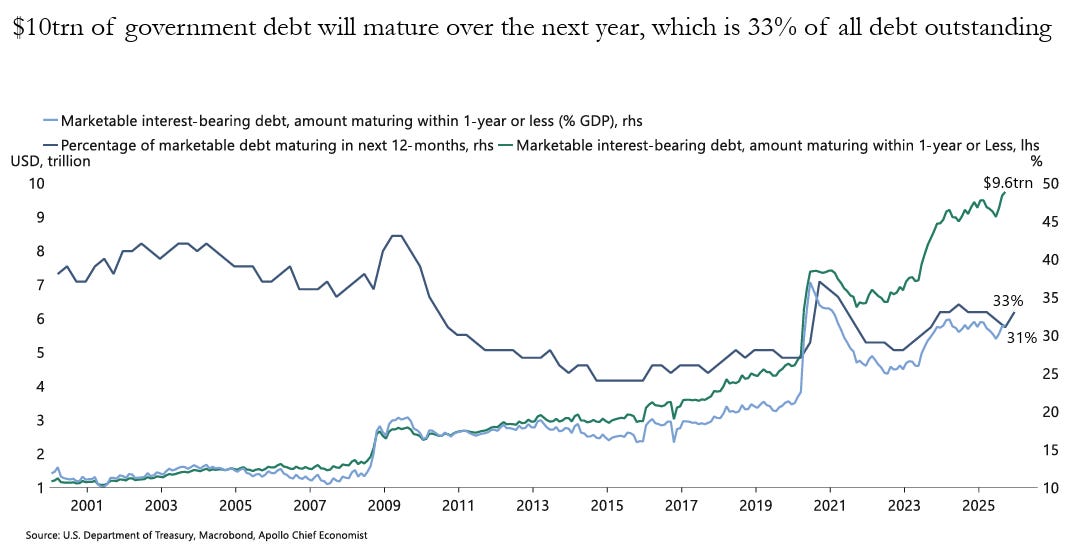

2. $10 trillion of government debt will mature over the next year, which is 33% of all debt outstanding.

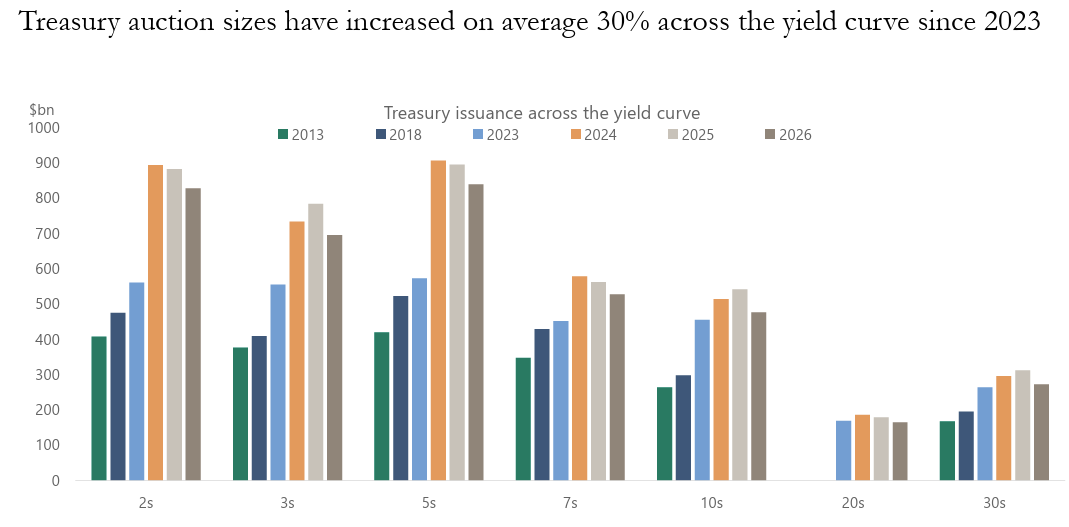

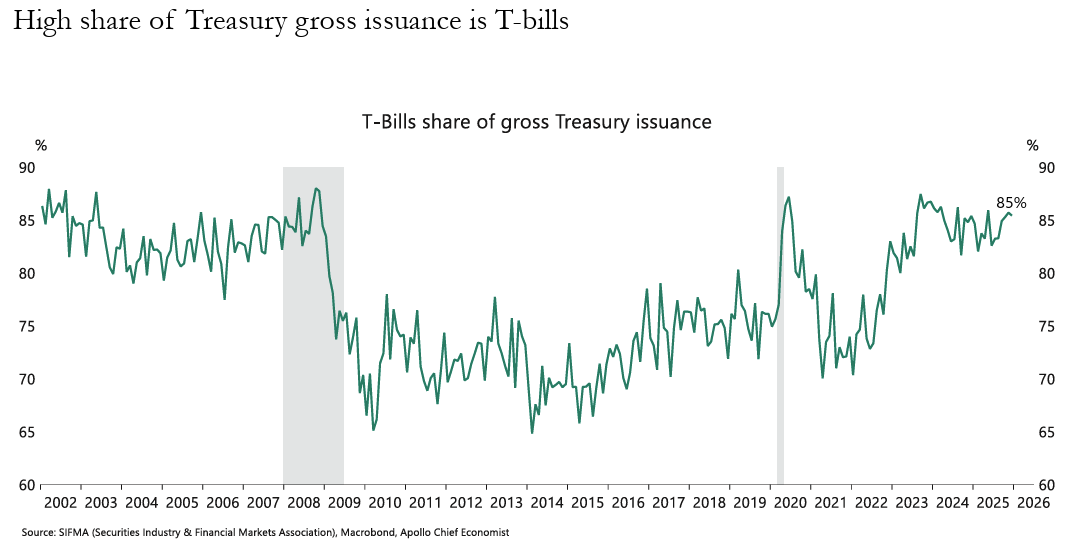

3. The share of T-bills outstanding has increased to 22%, and 85% of Treasury gross issuance is T-bills.

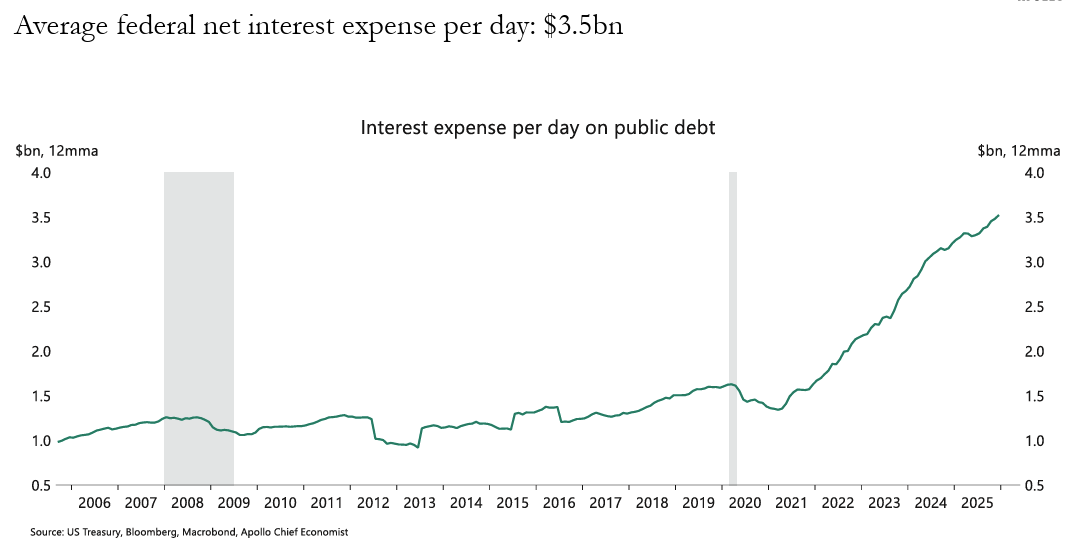

4. The average federal net interest expense per day, including weekends, is now $3.5 billion.

5. Foreign ownership of Treasuries has declined to 25% of the total outstanding, down from 33% a decade ago.

6. Japan has been increasing its holdings of Treasuries while China has been lowering its holdings.

7. In Treasury auctions, tails and stop-through have been small and relatively balanced, implying that there is still solid demand across the curve.

8. Treasury auction metrics show that indirect bidding, often a proxy for foreign central bank demand, has been declining over the past year, particularly for notes.

9. The Fed cutting interest rates has not lowered inflows into money market funds, implying that “money on the sidelines” is not as interest rate sensitive as many people think.

10. 89% of US government debt is fixed rate, and 22% of debt outstanding is in bills.

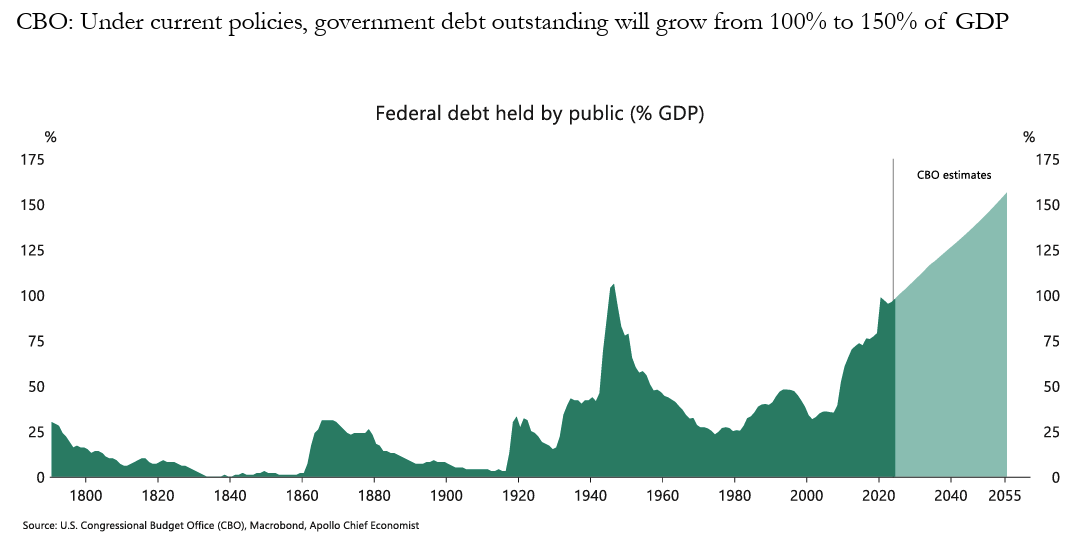

Investors are increasingly concluding that Western nations will likely inflate away their debt burdens rather than repaying them in real terms. Although AI-driven productivity gains offer a glimmer of hope, they may not arrive fast enough to prevent a currency devaluation. As this realization takes hold, the demand for sovereign bonds will evaporate, triggering a rotation into hard assets and traditional stores of value like gold. I think that is what we are seeing in gold markets. Below you can see that the CBO projects the deficit to only grow.

While the US situation could be worse, like Japan's, Japan may offer insights into potential future trends for the rest of the developed world. Japan is currently inflating away debt.

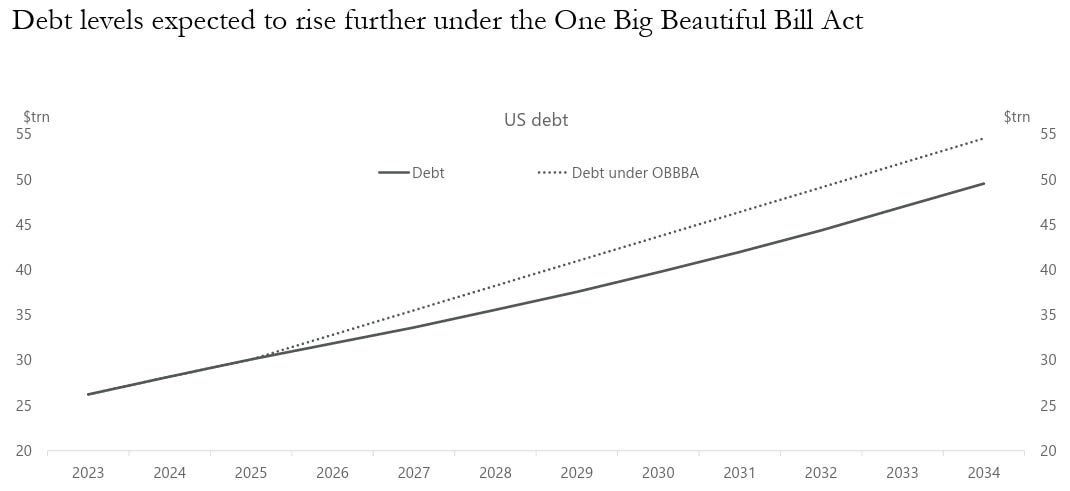

Remember the promises of DOGE to slash the deficit? Feels like a long time ago. With the addition of the One Big Beautiful Bill, the deficit only increased from the baseline forecast.

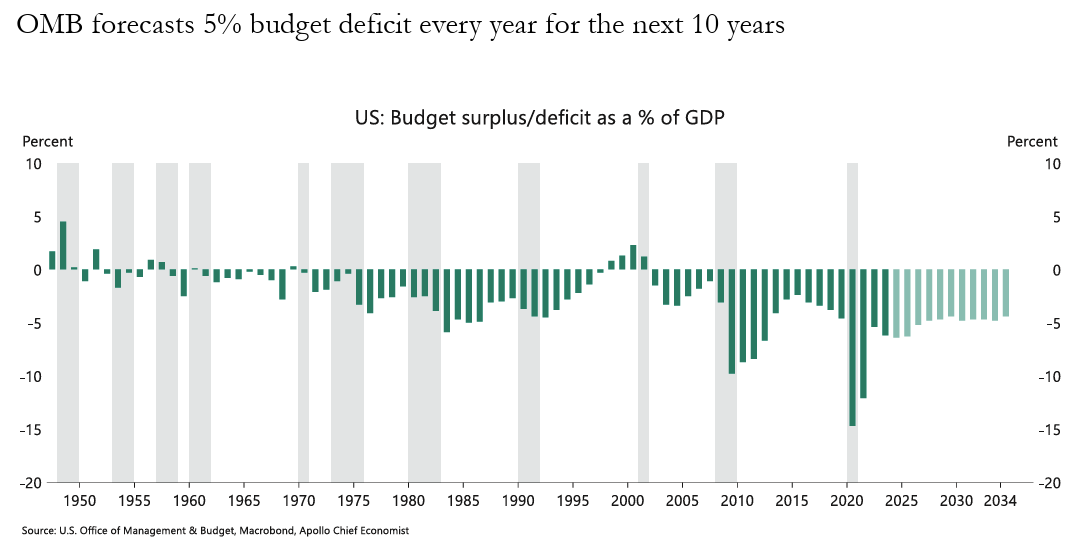

There are no plans to shrink the deficit below 4% of GDP, never mind balance the budget.

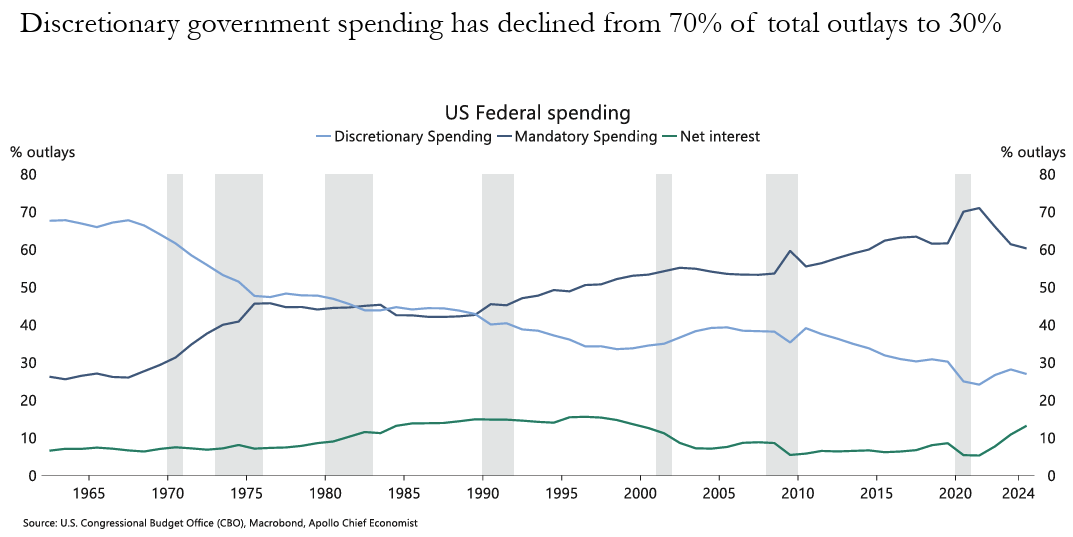

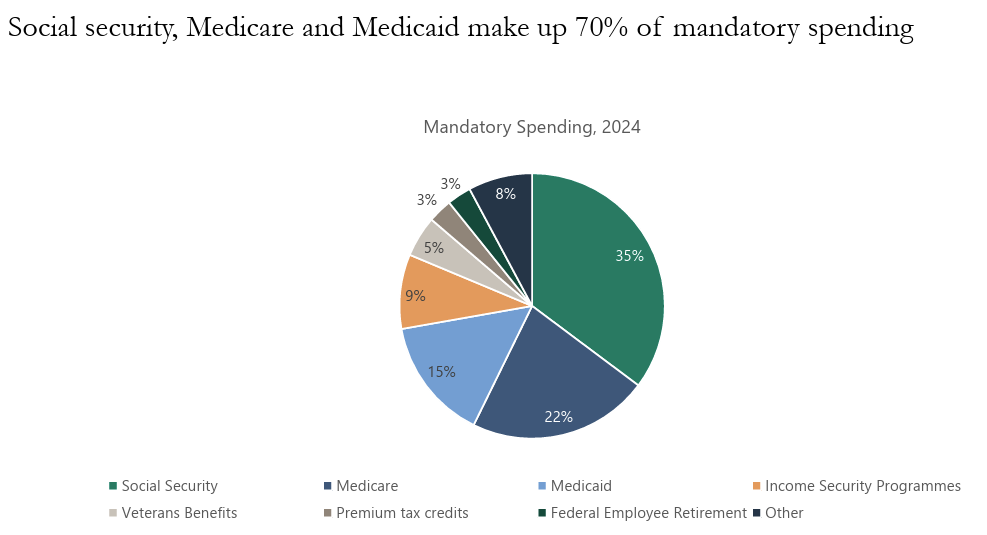

The fiscal reality is stark: 60% of outlays are now locked into mandatory spending. Simultaneously, rising interest expenses are devouring the budget, a form of non-productive spending that represents the cost of demand previously pulled forward. We are effectively paying for yesterday’s consumption with today’s potential growth.

Why can’t they cut mandatory spending? 70% of it is Medicare and Medicaid, as the population ages, only more burden will be put on these programs.

14% of the federal budget is allocated to interest expense, more than defense… And that is the biggest army in the world. The US is spending $3.5B a day on interest expense.

That is $1 of every $5 of tax collected to pay interest.

33% of all debt outstanding will be rolled in the next year. That’s why the administration wants rate cuts, as it can lower interest rates at the short end of the yield curve. This is not a sustainable solution, it only kicks the can down the road.

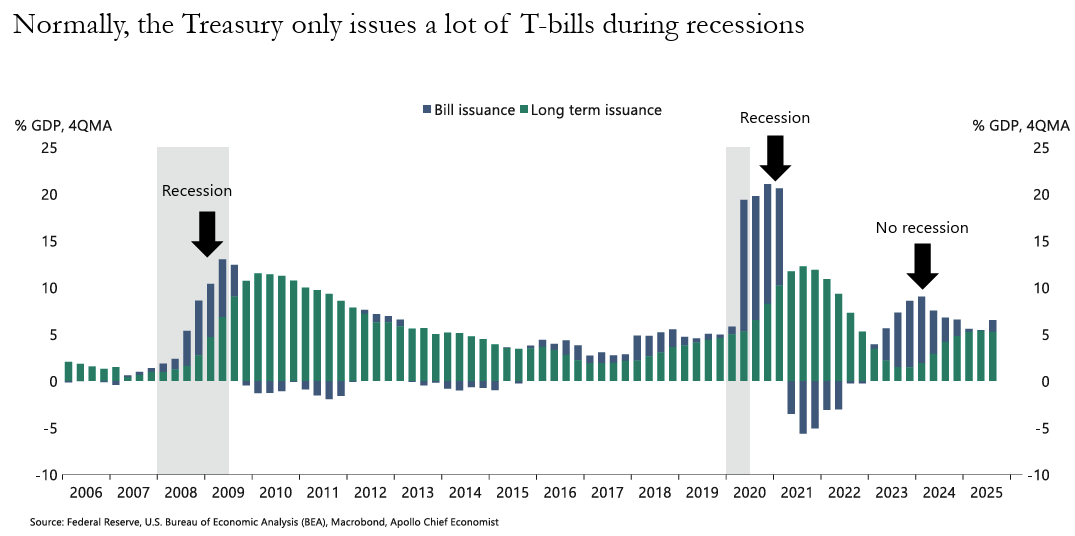

The Fed has less control over the long end of the yield curve, and the long end of the yield curve has been sniffing out the global fiscal irresponsibilities. Therefore, in recent years the Treasury has resorted to issuing at the short end of the curve. This is a classic Emerging Market country move prior to a debt crisis.

85% of issuance is now T-bills.

Historically, excess bill issuance was reserved for recessions, recently it became an everyday occurrence.

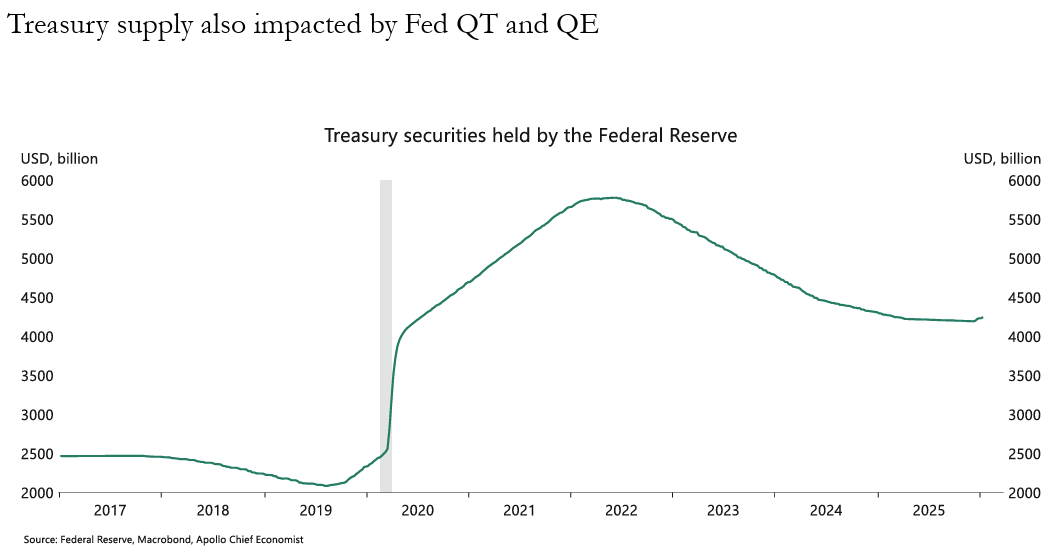

The Fed still owns trillions of dollars of US debt and QT has ended, they’ve reached the limit of balance sheet shrinking at the Fed.

All to say, if gold is an indicator, it appears the chickens are coming home to roost.