AI vs Oil

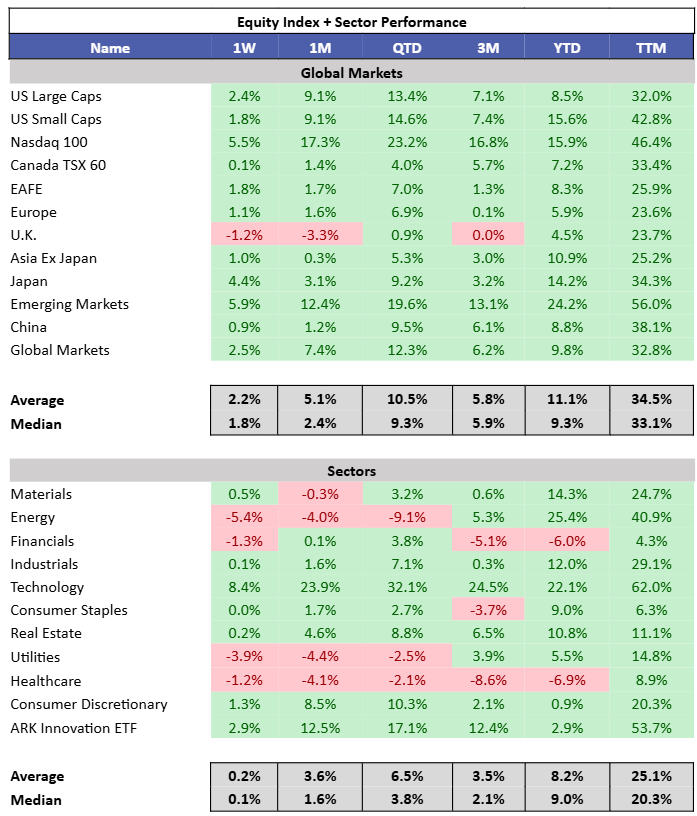

Equities moved higher with the Nasdaq posting its second-best week of the year, while the S&P 500 pushed toward fresh highs as strong earnings and a better-than-expected payrolls print helped sentiment. April U.S. nonfarm payrolls rose 115k versus expectations closer to 65k. Canada was much weaker, with the economy shedding 17.7k jobs and the unemployment rate rising to a six-month high of 6.9% versus expectations of 6.7% and compared to 4.3% in the U.S. Earnings remain strong. Roughly 85% of the S&P 500 has beaten EPS expectations, with Q1 EPS growth now tracking nearly +28% YoY versus expectations closer to +13% entering earnings season. Emerging markets and Japan also posted strong weeks. Tech was the top-performing sector while Energy lagged.

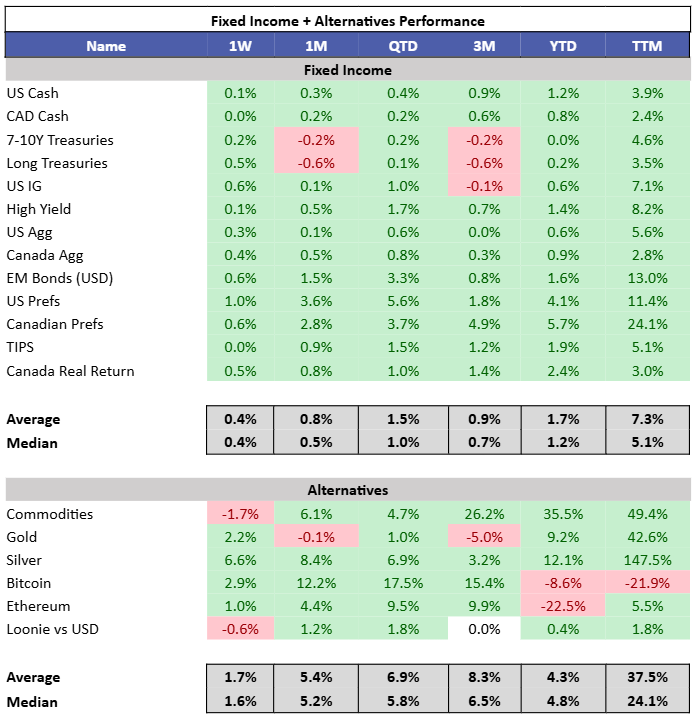

10Y yields fell 2 bps in the U.S. and 5 bps in Canada, making for a decent week for fixed income. Commodities struggled overall, although precious metals had a strong week.

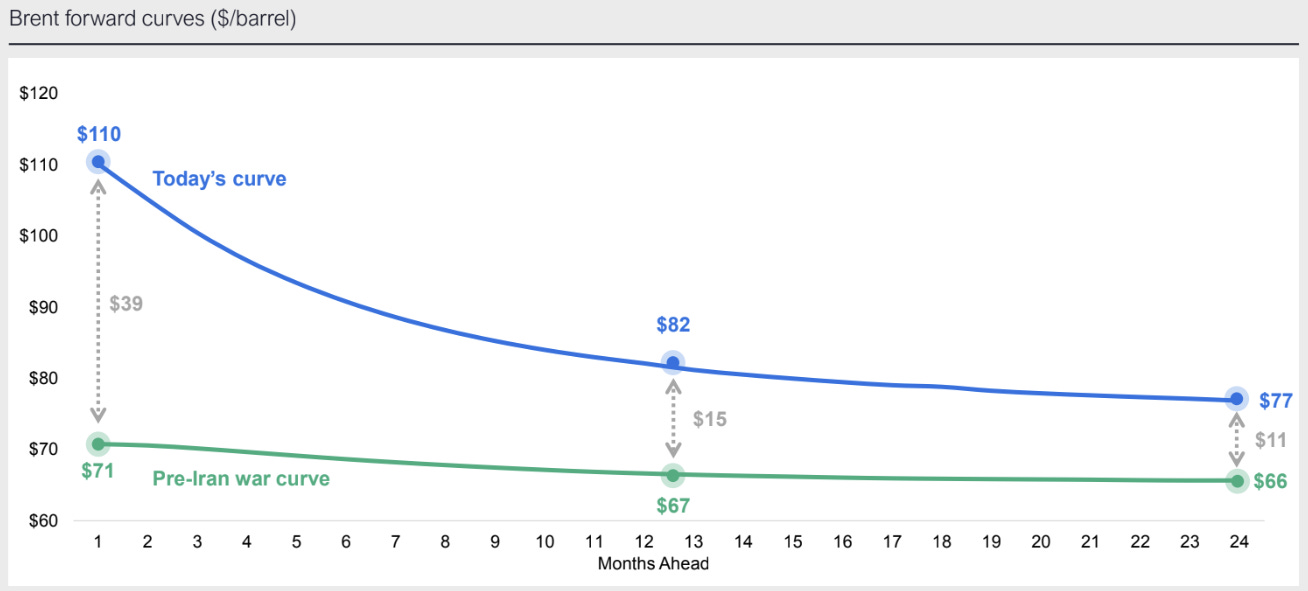

The AI infrastructure trade has dominated fears over Hormuz-driven oil shortages YTD. (Blackrock)

This podcast does a good job dissecting the crossroads markets are at. There is growing tension between AI capex driving earnings sharply higher and the overhang of what potential oil shortages could mean for the global economy.

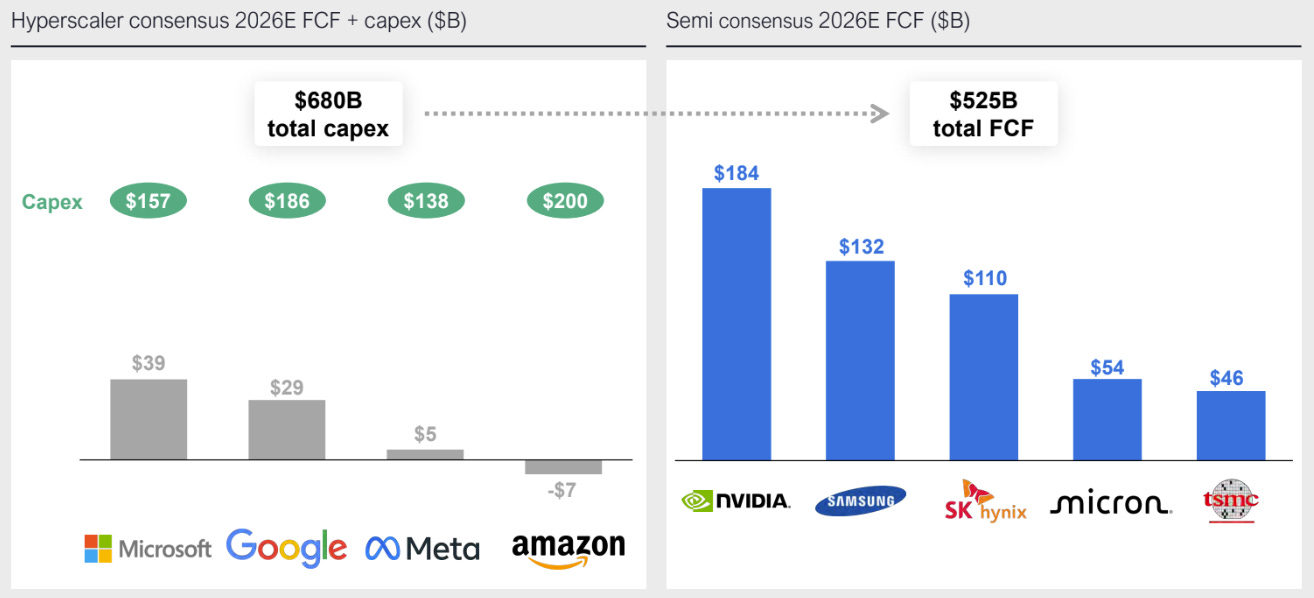

In hindsight, it probably should have been clearer that hyperscalers pointing a bazooka of cash at the AI infrastructure industry would cause cash flows across that supply chain to surge. (Coatue)

What we underestimated was the impact of cash flow that would have otherwise gone toward buybacks being redirected into the real economy, and the knock-on effect that would have on earnings growth. (GS)

Oil markets continue to price in a normalization of the conflict with Iran. (Coatue)

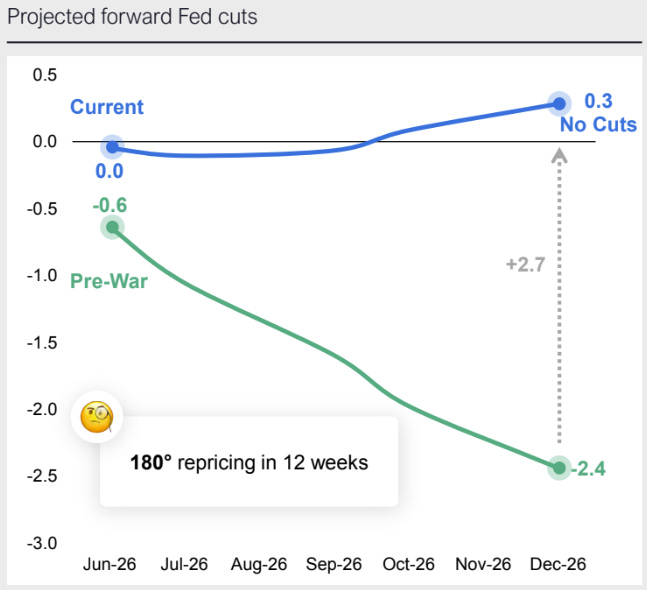

However, the Fed cuts that had been priced into markets have largely been erased. (Coatue)

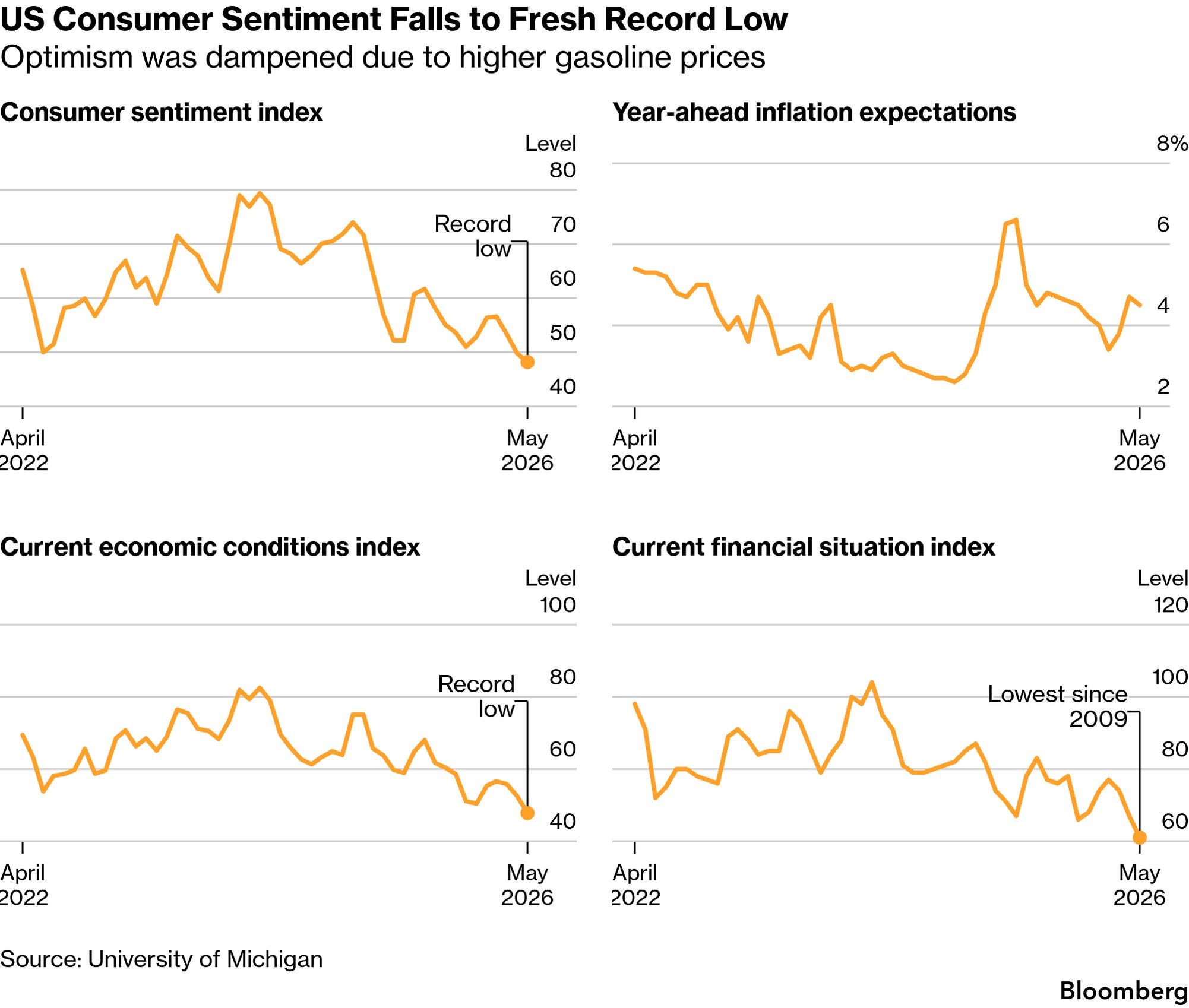

Consumer confidence remains near record lows. During Q1 earnings season, several companies cited weakness among lower-end consumers. (Bloomberg)

Companies also began discussing the impact of higher gas prices on earnings calls. (Bloomberg)

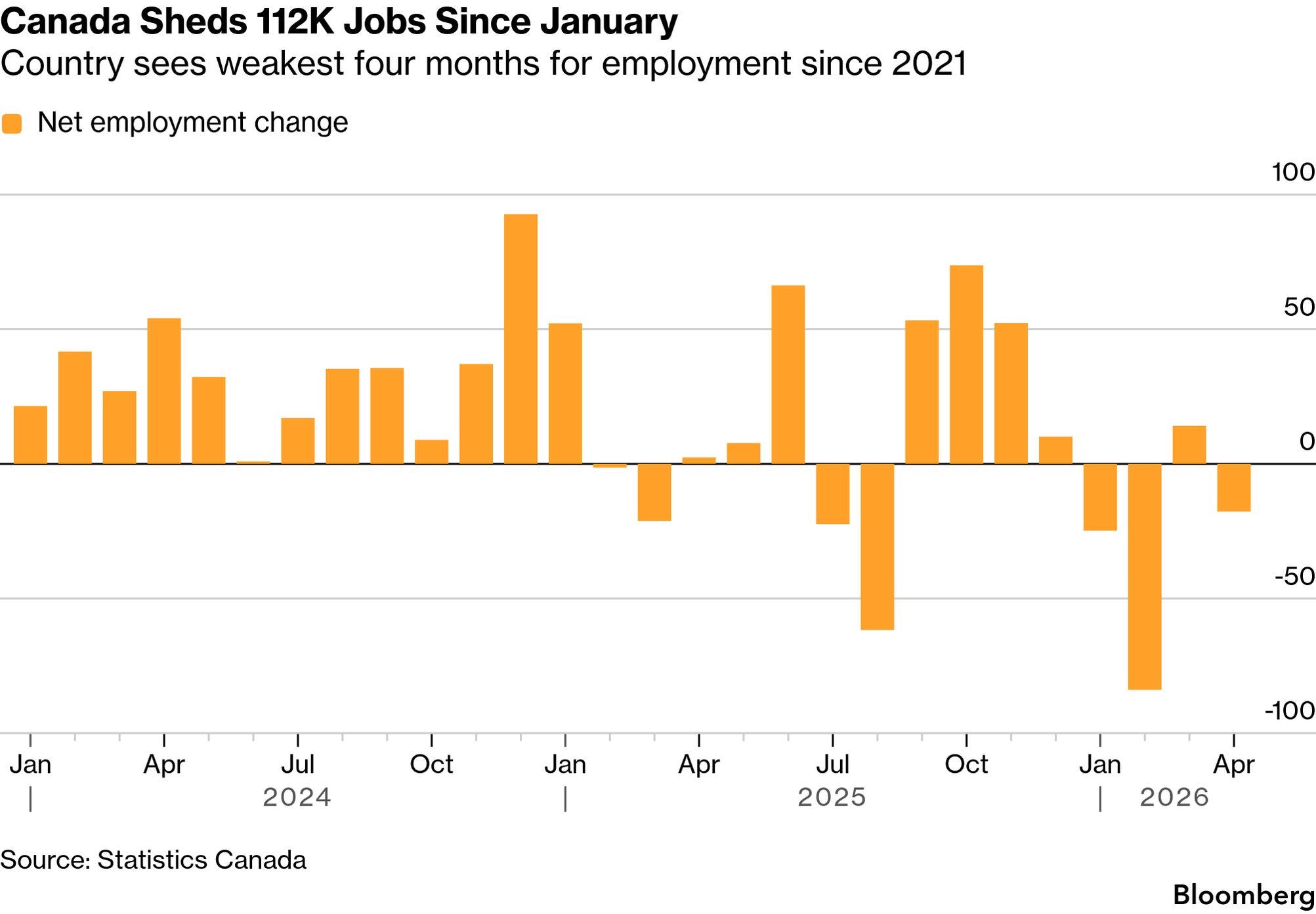

The Canadian economy has now shed 112k jobs so far this year, marking the weakest four-month stretch since the Covid-19 pandemic in 2021. Employment fell by 17.7k in April while more people entered the labour force, pushing the unemployment rate to 6.9%. Expectations were for job growth of 10k and for the unemployment rate to remain steady at 6.7%. The weaker print caused CAD to sell off. (Bloomberg)

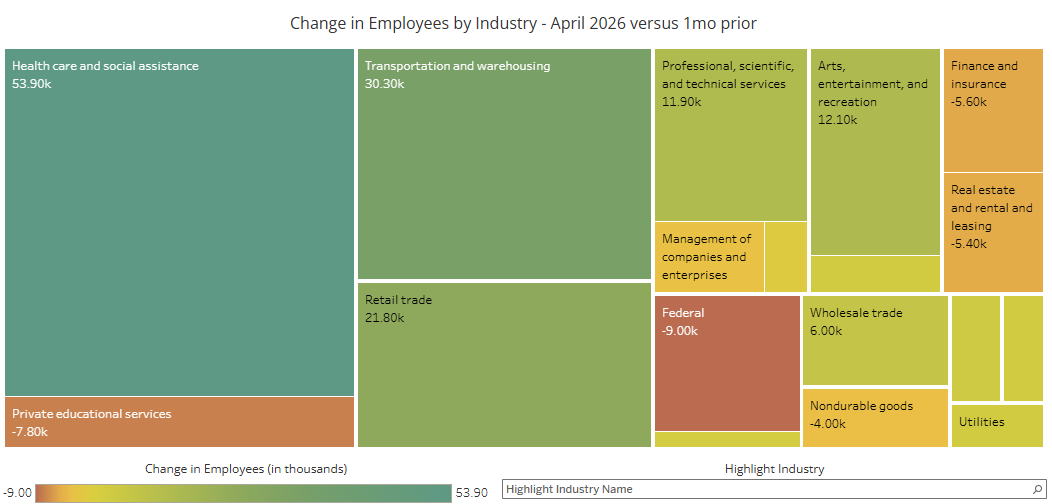

Healthcare, transportation, and retail trade drove U.S. job gains in April, making the report broader-based than previous months. (Bancreek)

That said, the labour market still does not look overly strong beneath the surface. Since early 2023, most job gains have continued to come from government-adjacent sectors. (Blackrock)

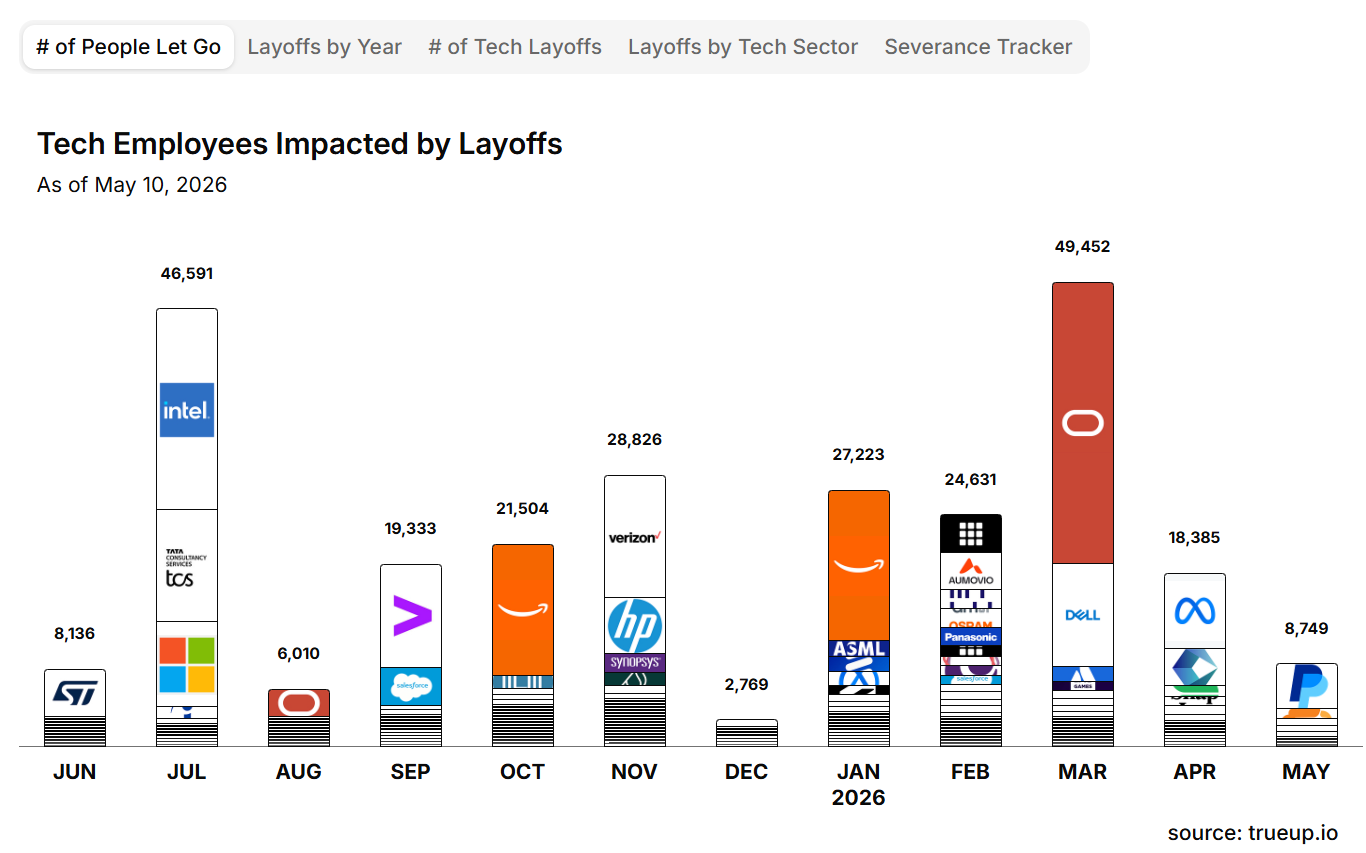

There were also several notable tech layoff announcements last week, with PayPal, Cloudflare, and Coinbase all reducing their workforces by double digits. We may need to start thinking about labour markets differently. Historically, a strong economy meant more jobs, but productivity gains from AI could begin to change that relationship. If layoffs accelerate meaningfully, that could eventually point to economic weakness, but for now unemployment remains relatively low.