Crowding Out

Holy momentum. (@FoFtyTrader)

This is funny to think about. Lots of misinformation surrounds the conflict, which raises a critical question: should we accept a closed Strait as the new normal?

Alphabet has announced a $80 billion equity capital raise to expand AI infrastructure and compute, with participation from Berkshire. This marks the first time Google has raised equity in two decades, proving the AI arms race is real. Gavin Baker made a good point that the hyperscalers, particularly Google, have a 6 to 12 month view into what the leading edge looks like. The outlook must still look promising. (Sergey Alexashenko)

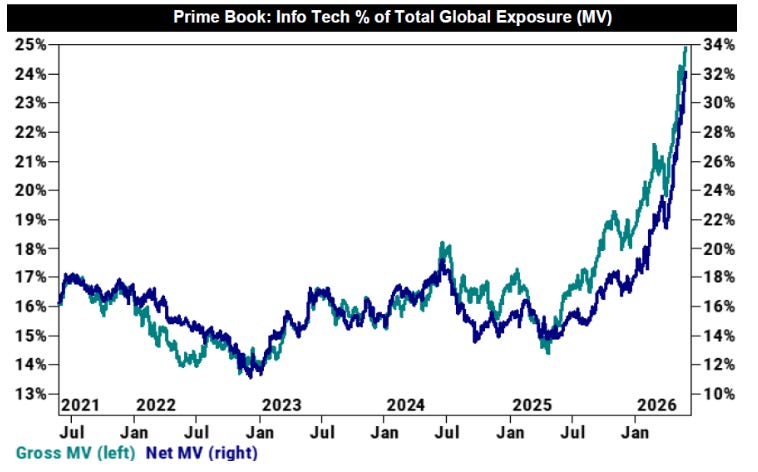

As big tech taps capital markets, we could see other sectors get crowded out. Hedge fund exposures perfectly illustrate this dynamic. Gross and net allocations to Info Tech, as a percentage of the global Prime Book, are both still hovering near five-year highs. (Goldman)

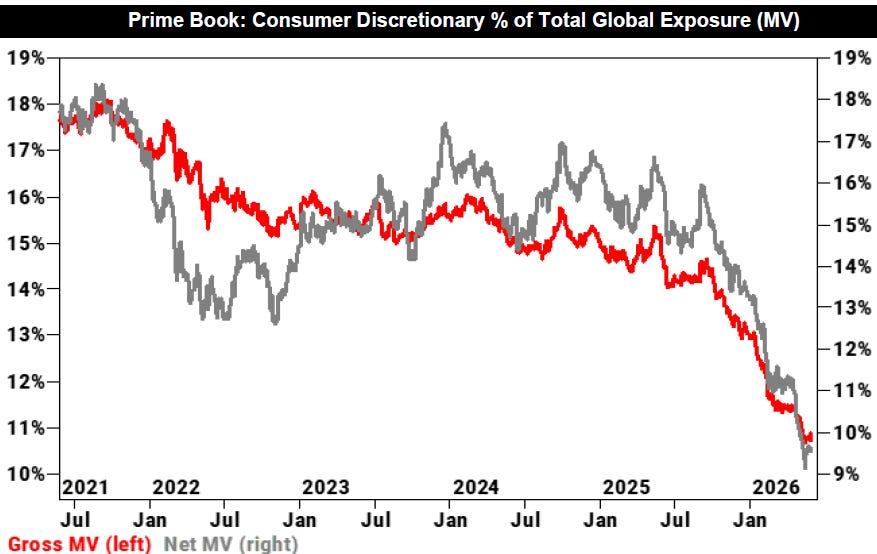

Meanwhile, gross and net allocations to Consumer Discretionary are hovering near five-year lows. This shift could either be a direct consequence of tech crowding out or a reflection of a weakening consumer. (Goldman)

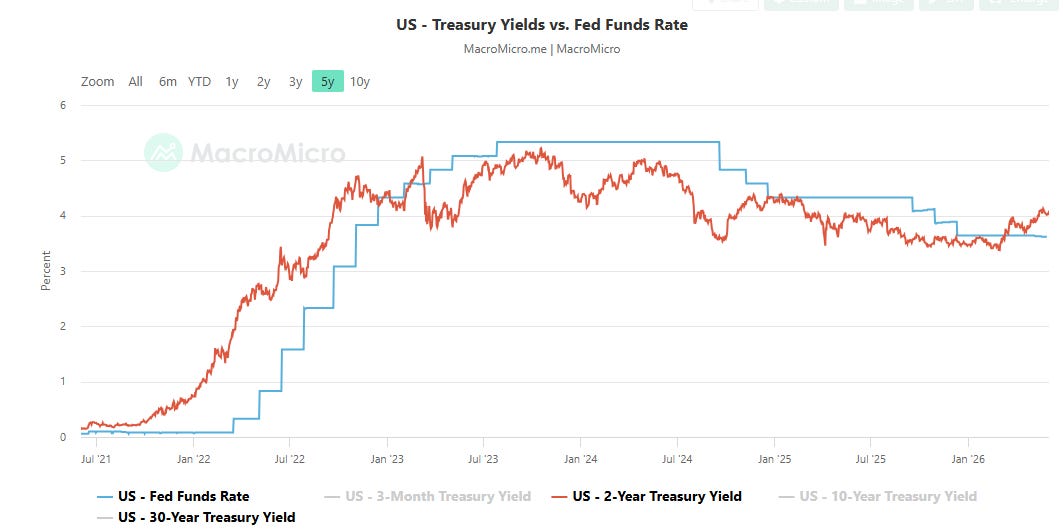

Apollo also believes hyperscaler debt issuance could push Treasury yields up. The yield curve is under attack from all angles.

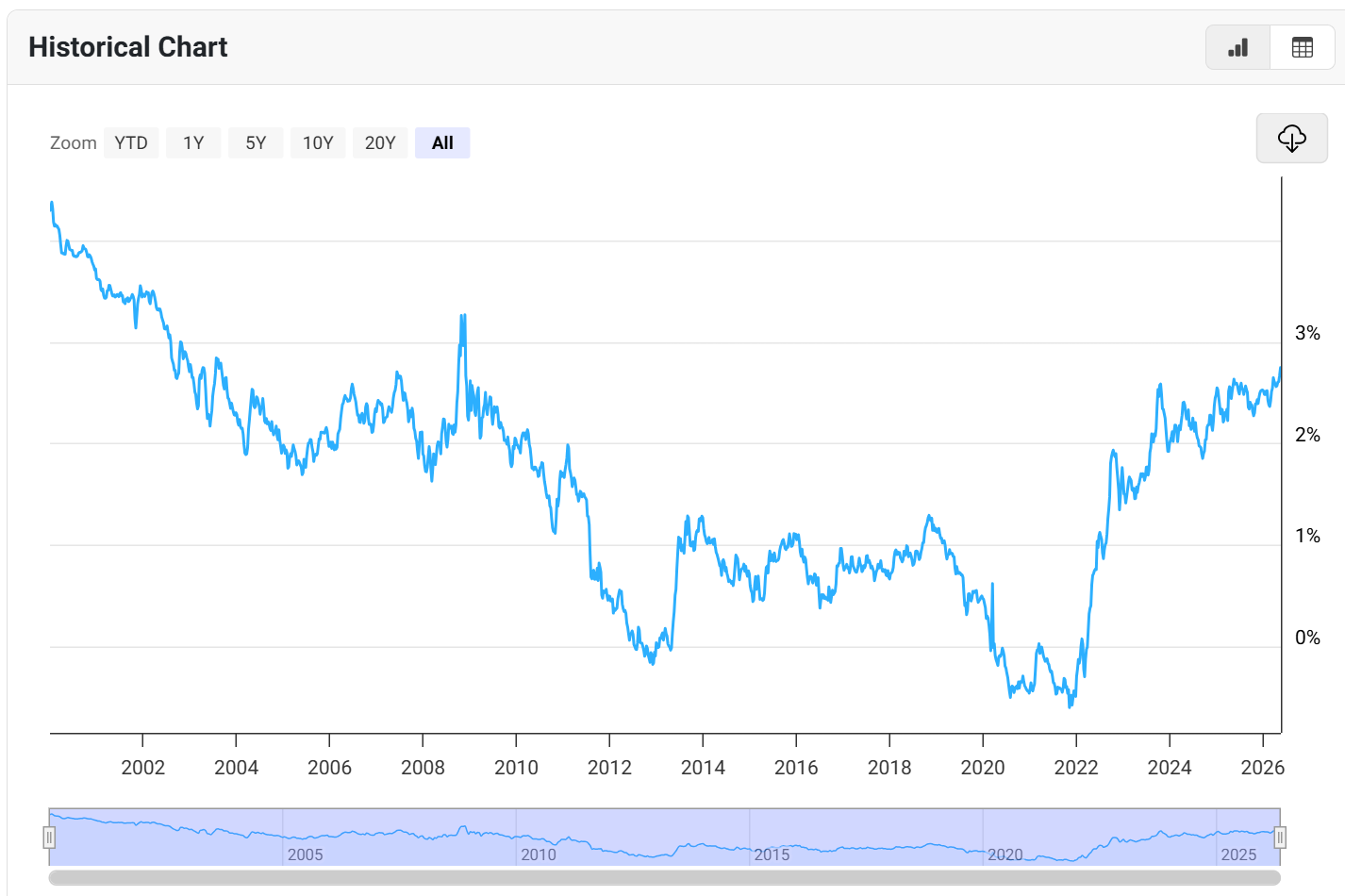

For the first time in three years, the 2-year yield has risen above the Fed funds rate, highlighting persistent inflation problems.

With rich equity markets and real fixed income returns pressured by inflation, locking in a 10-Year TIPS Yield of 2.74% seems compelling for a risk-averse investor, as it guarantees an almost 3% real return for the next decade. You can certainly argue that CPI does not reflect real cost of living increases and can be gamed, which is true, but this remains a compelling option.

Full pitch below.

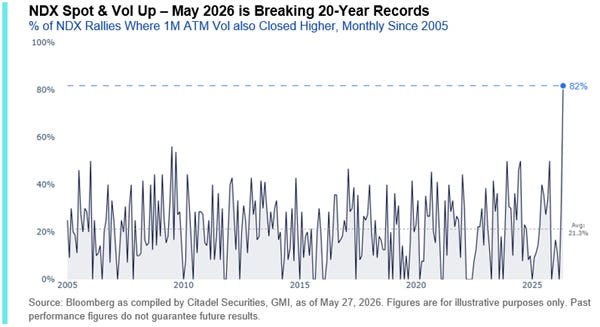

What has made this rally particularly unusual is a persistent "spot up, vol up" dynamic across Nasdaq and Semiconductor leadership. Aggressive call option buying has pushed volatility higher even as equities rise, driving NDX volatility to its richest levels versus SPX in over a year. Through May 2026, the NDX saw 9 sessions where both spot and 1-month implied volatility rose simultaneously, accounting for roughly 82% of the month's rallies. This is the highest frequency since 2005, far exceeding the 21% historical monthly average. (Citadel)

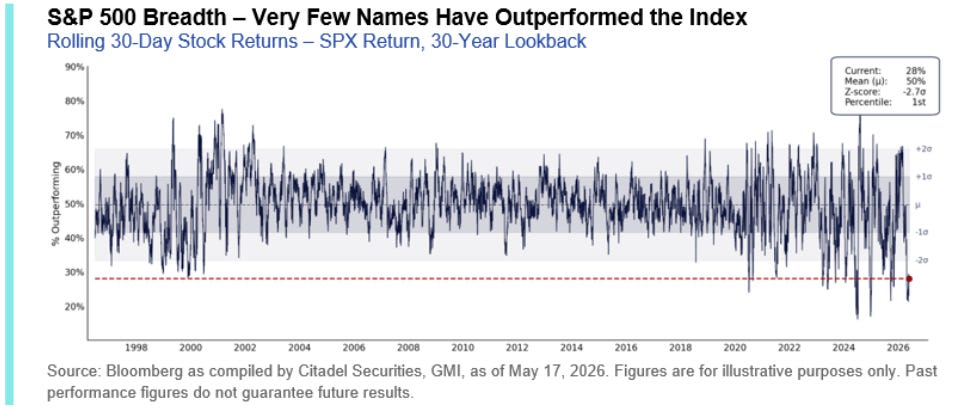

Underneath the surface, market breadth is historically narrow. Only 28% of S&P 500 constituents have outperformed the index over the past 30 trading days, a 1st percentile observation relative to the last 30 years. Put simply, just 10 companies have driven 67% of the S&P 500’s rally since the end of March. (Citadel)

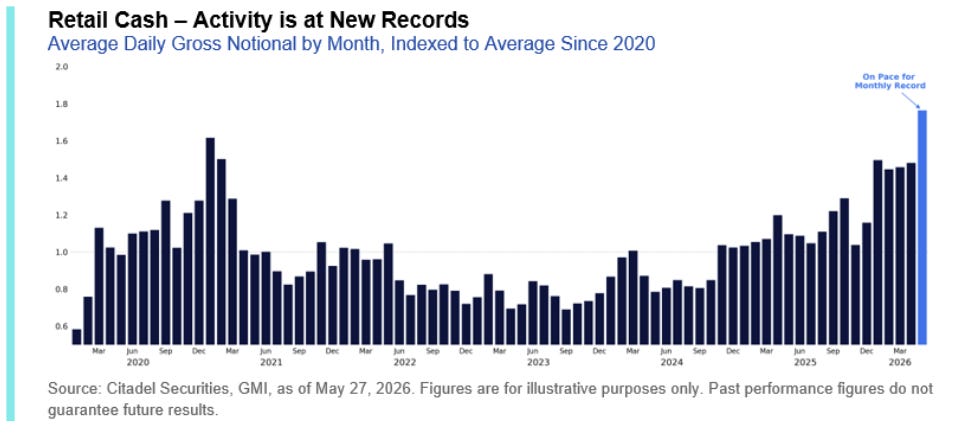

Retail traders have become the new price setters, with May retail cash and options volumes tracking at record levels. Daily cash volumes are on pace to finish nearly 10% above the previous January 2021 meme-stock record. However, unlike 2021, retail participation is now concentrated in the same institutional leadership names, specifically mega-cap tech, AI infrastructure, and semiconductors. (Citadel)