Daily Charts - Blackstone Quarterly Outlook

Daily Charts - Blackstone Quarterly Outlook

TL;DR

Near term momentum offsets recession risk, longer to occur

inflation will be more persistent

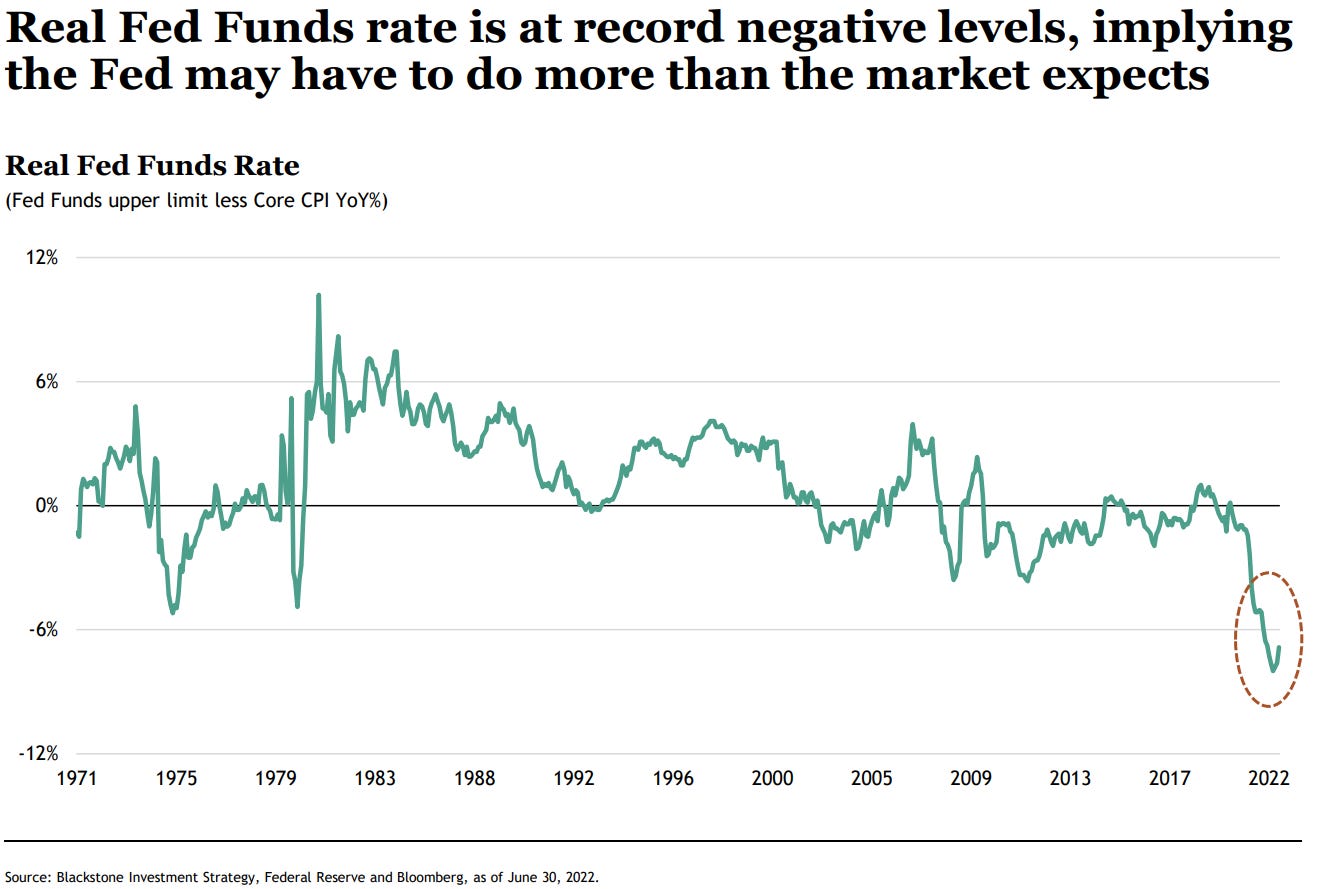

Interest rates will be higher for longer

Based on their view, most portfolios are underweight inflation hedges; inflation linked bonds, hard assets, commodities and maybe gold. Some of these have scenarios where they suffer but they should perform better than stocks and nominal bonds in an inflationary environment.

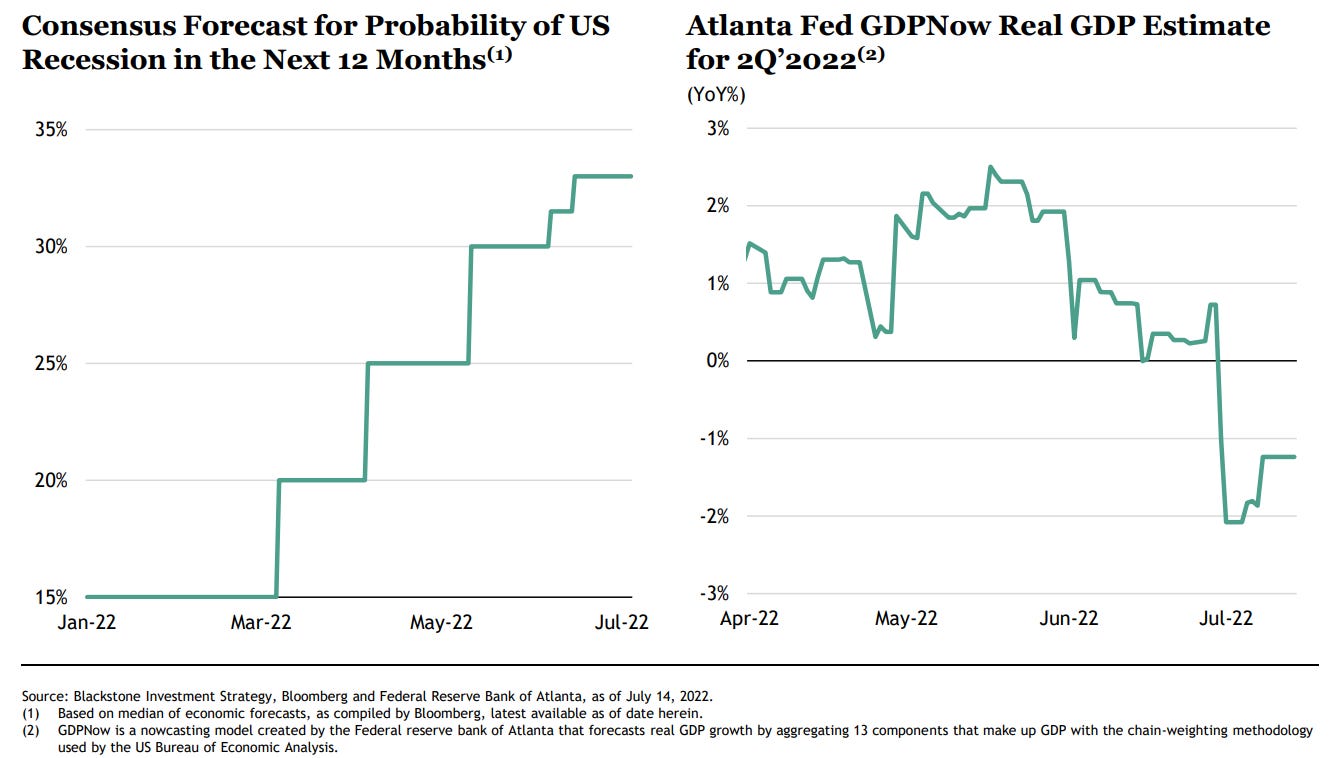

Consumer is in the dumps, economists believe there is a 33% chance of a recession in the next 12 months… Blackstone believes it could be higher.

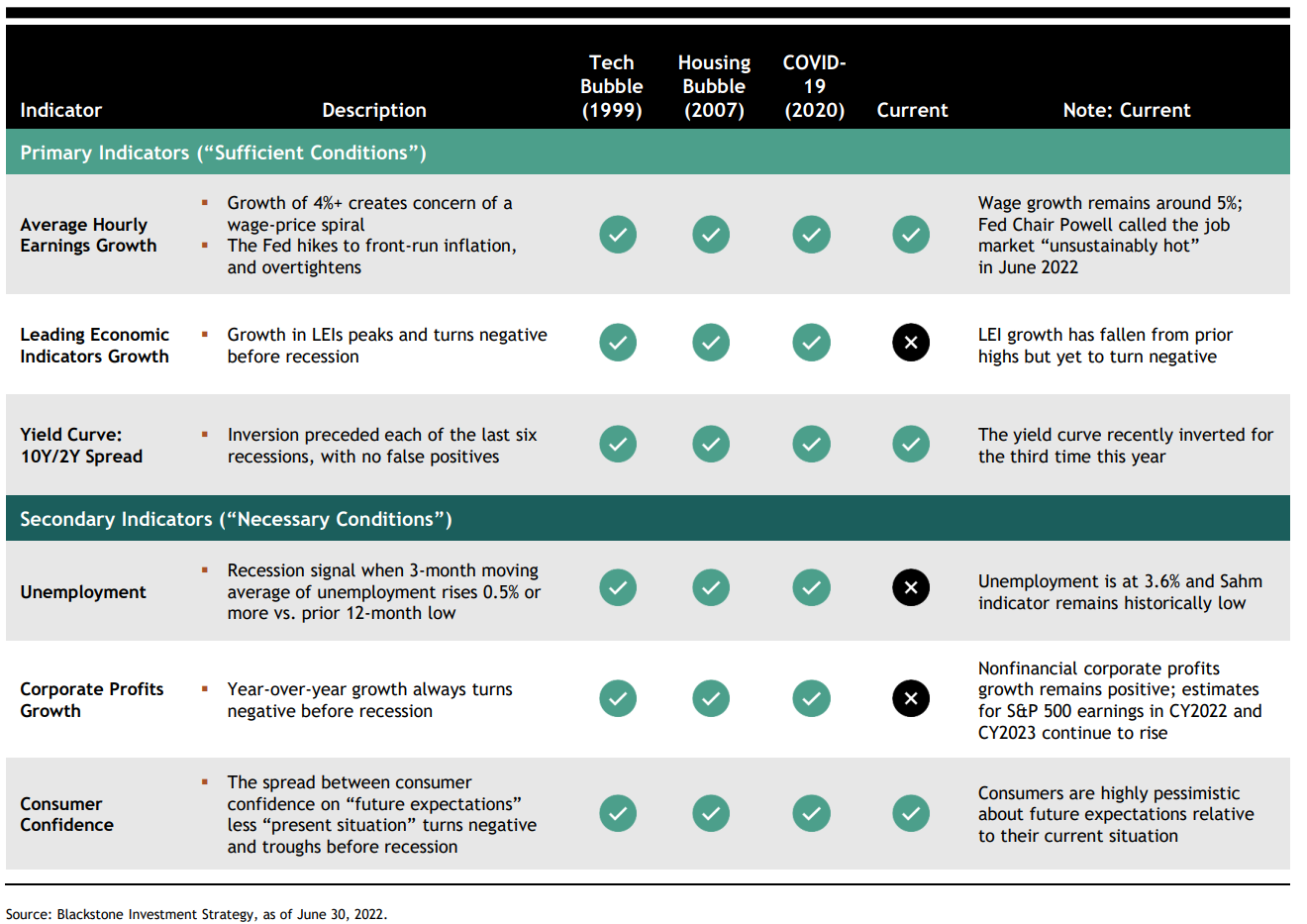

Recession checklist. Again, weird situation where we have a very tight labour market, consumer is in good shape, corporate profits are fine and the economic indicators are not at recessionary levels but other indicators like the yield curve and consumer sentiment point to trouble ahead. These distortions are lively due to the massive fiscal impulses pumped into the economy.

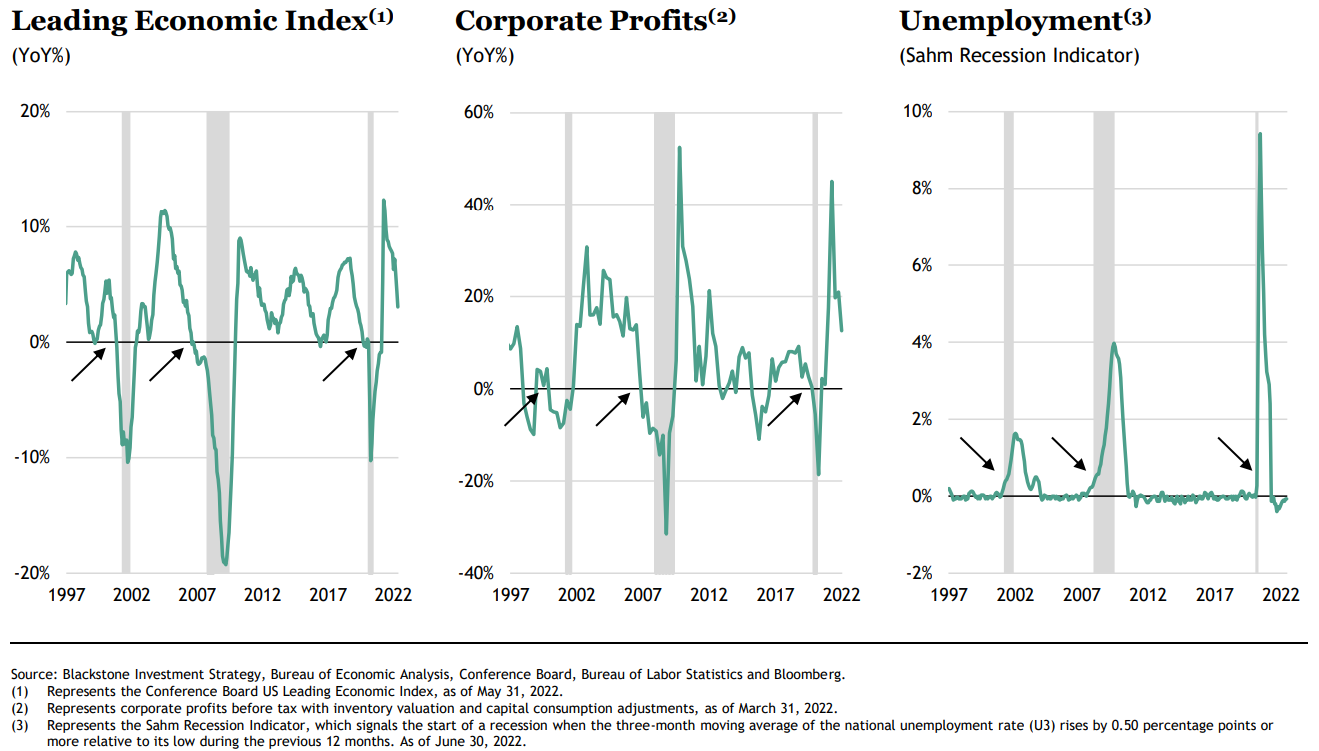

These are the 3 economic indicators that are hanging in there, delaying an official recession. They are headed in the wrong direction but nowhere near recessionary levels.

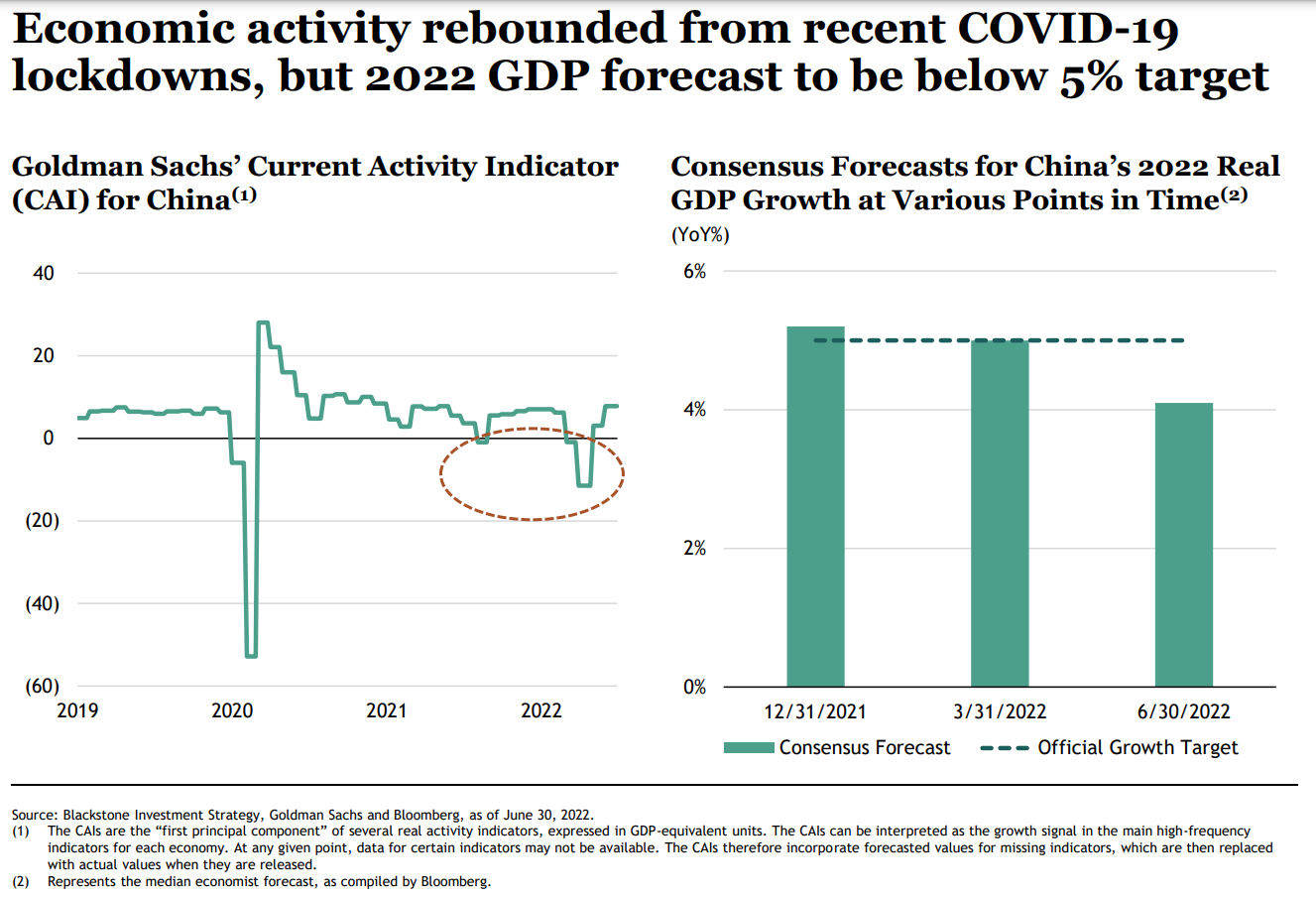

China is slowing down, the worlds second largest economy.

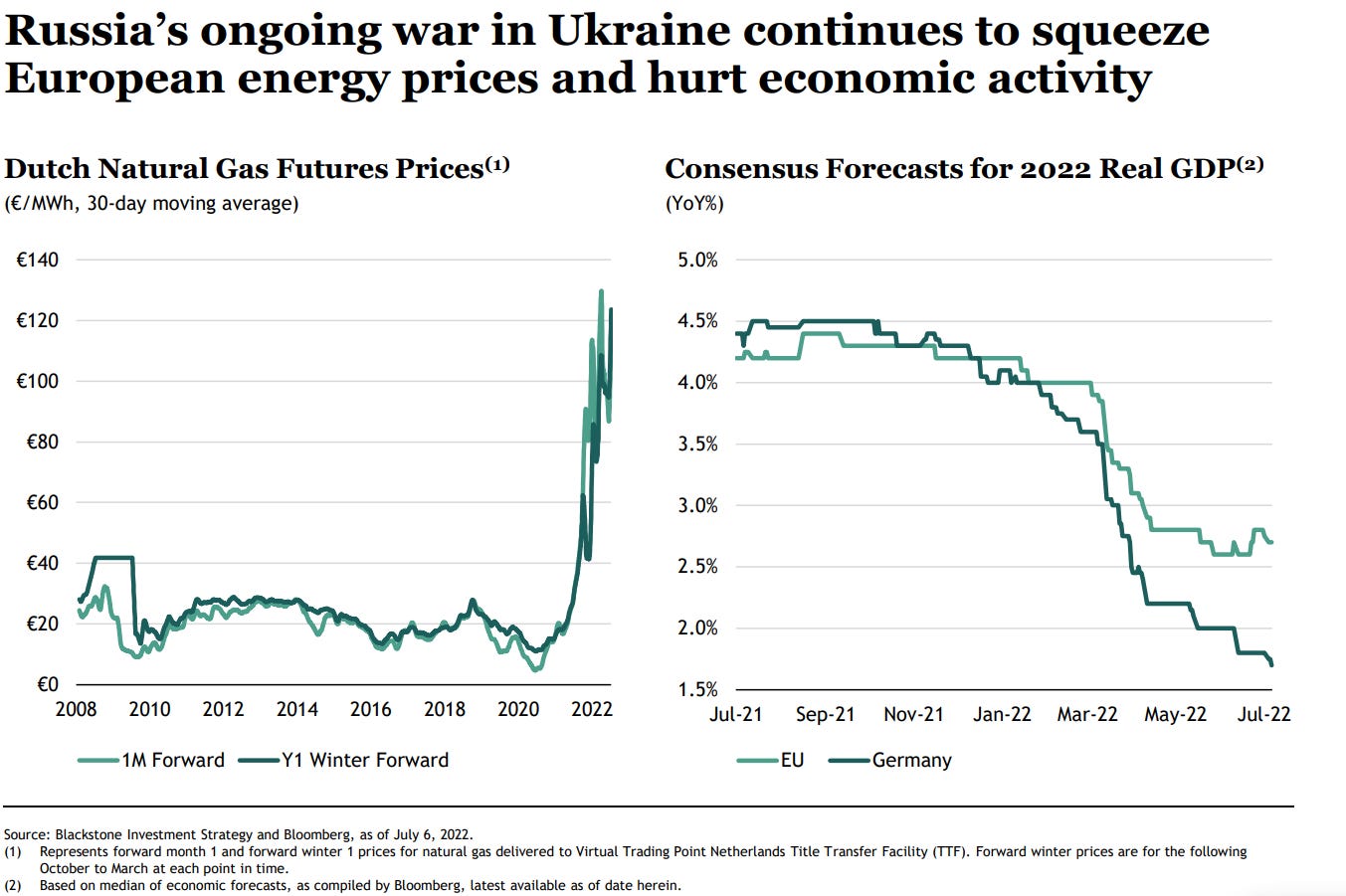

Europe is in the worst situation of the developed world. They have an energy crisis which is morphing into a debt crisis. Italy is the weakest link.

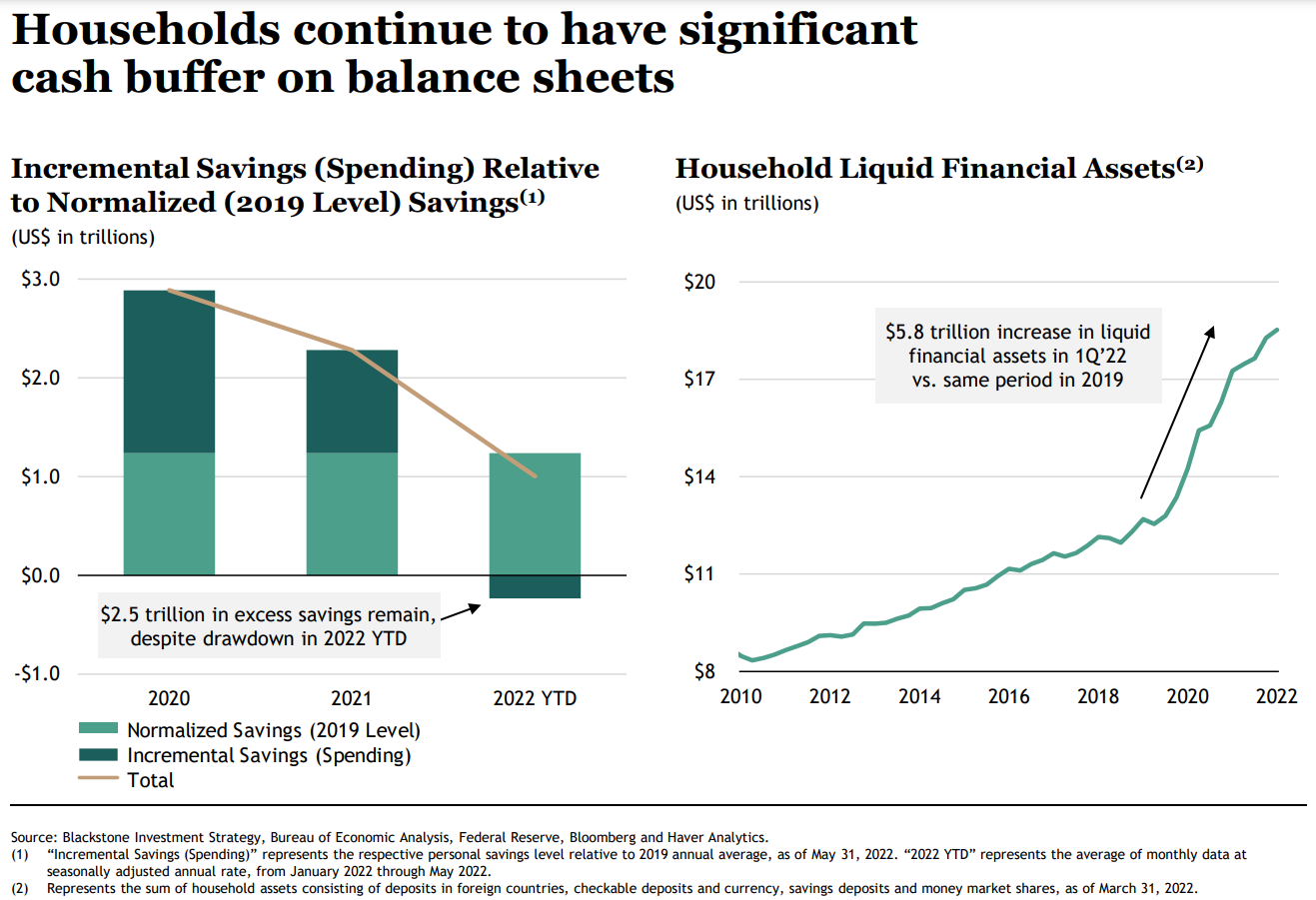

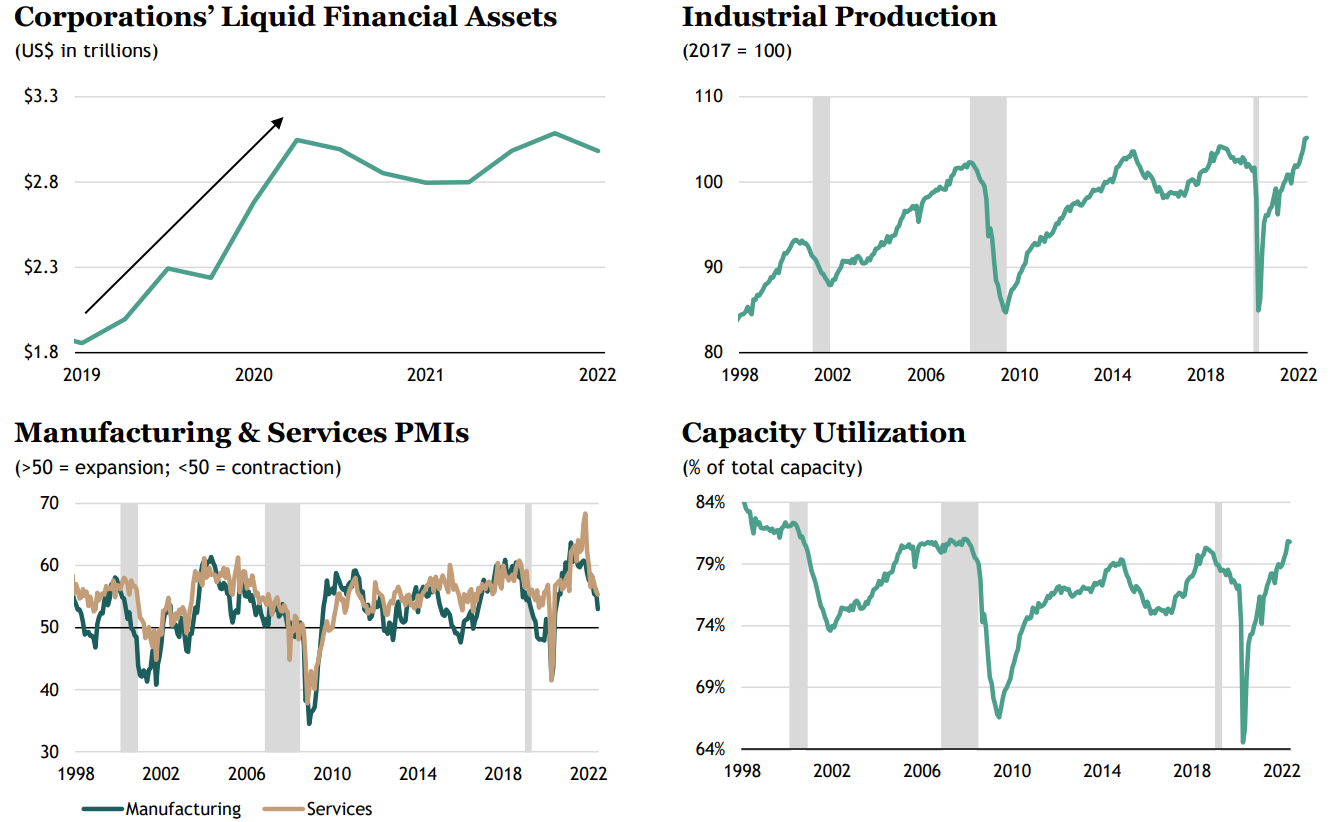

But… households are flush with cash.

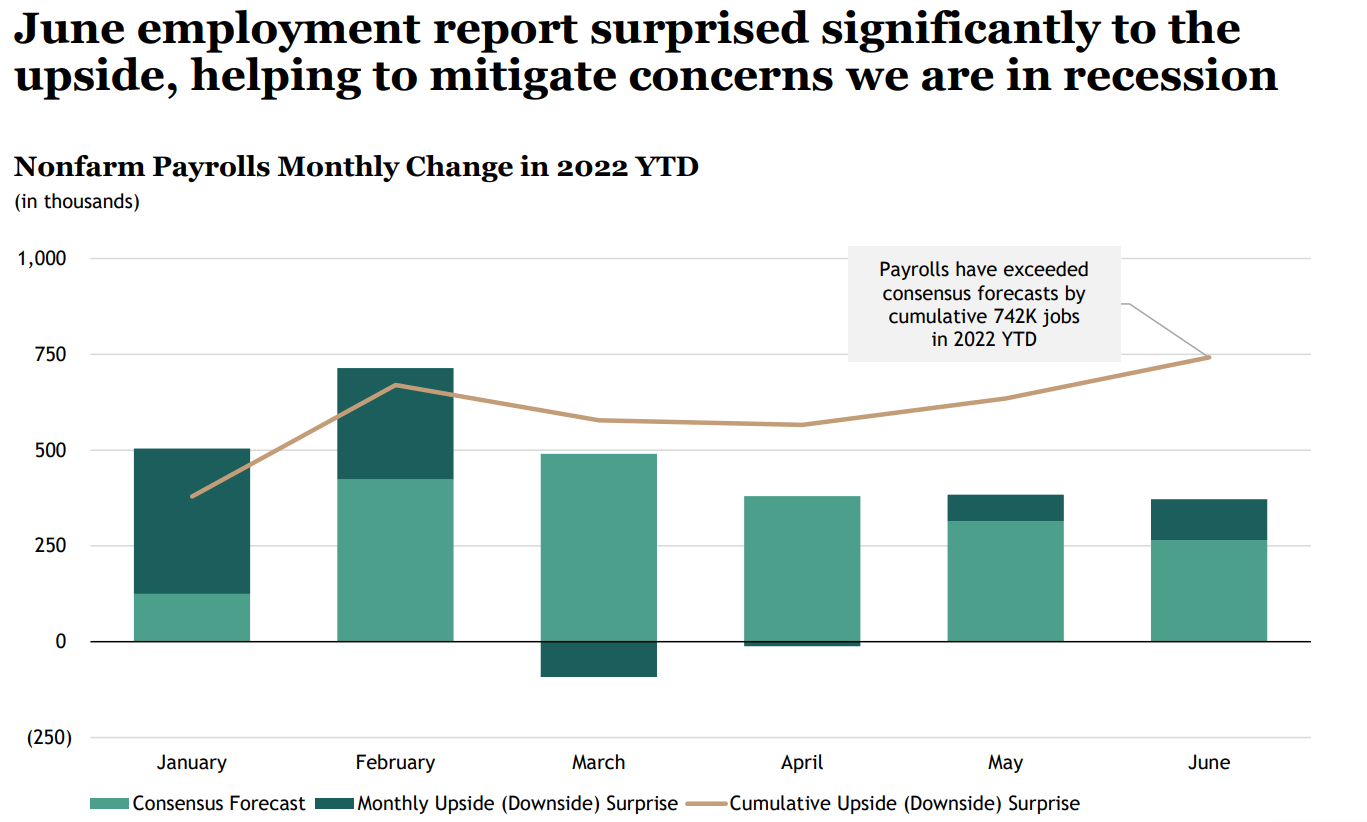

Labour markets continue to surprise to the upside, pressuring inflation.

Corporates are liquid and continue to produce goods.

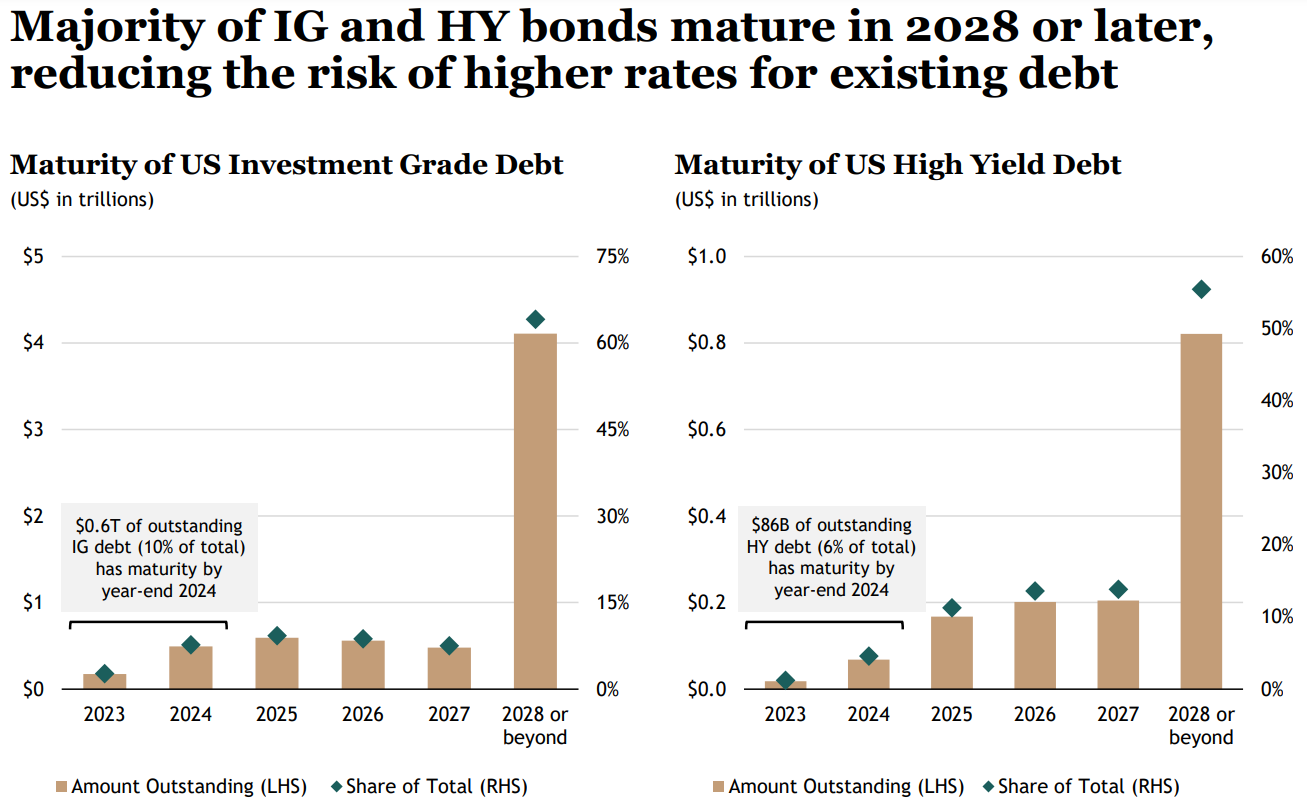

There won’t be near term financing pressure until beyond 2028.

Shelter will continue to push inflation higher, it takes a while to flow through due to calculation methodologies. Volatility in the financing market have caused projects to be pulled, which won’t help the housing shortages. They think we require positive real rates across the curve to cool inflation.

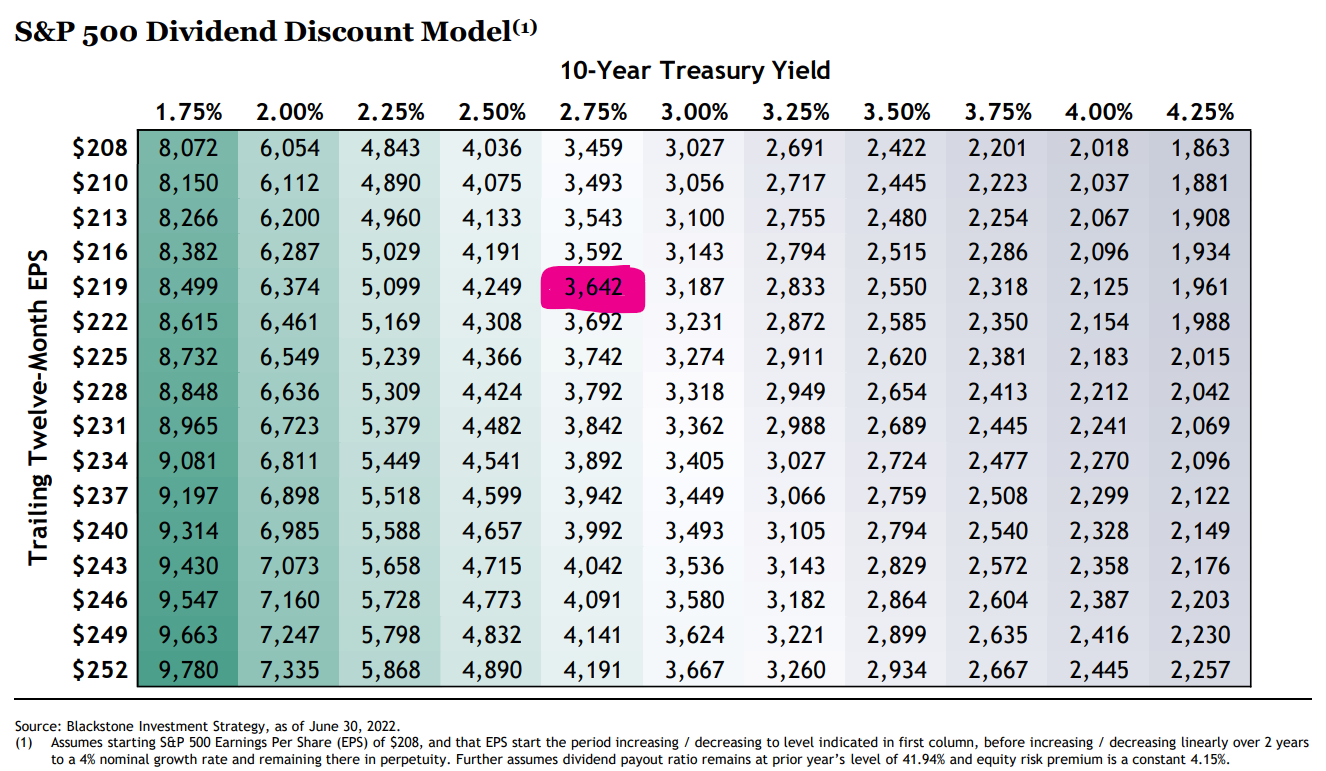

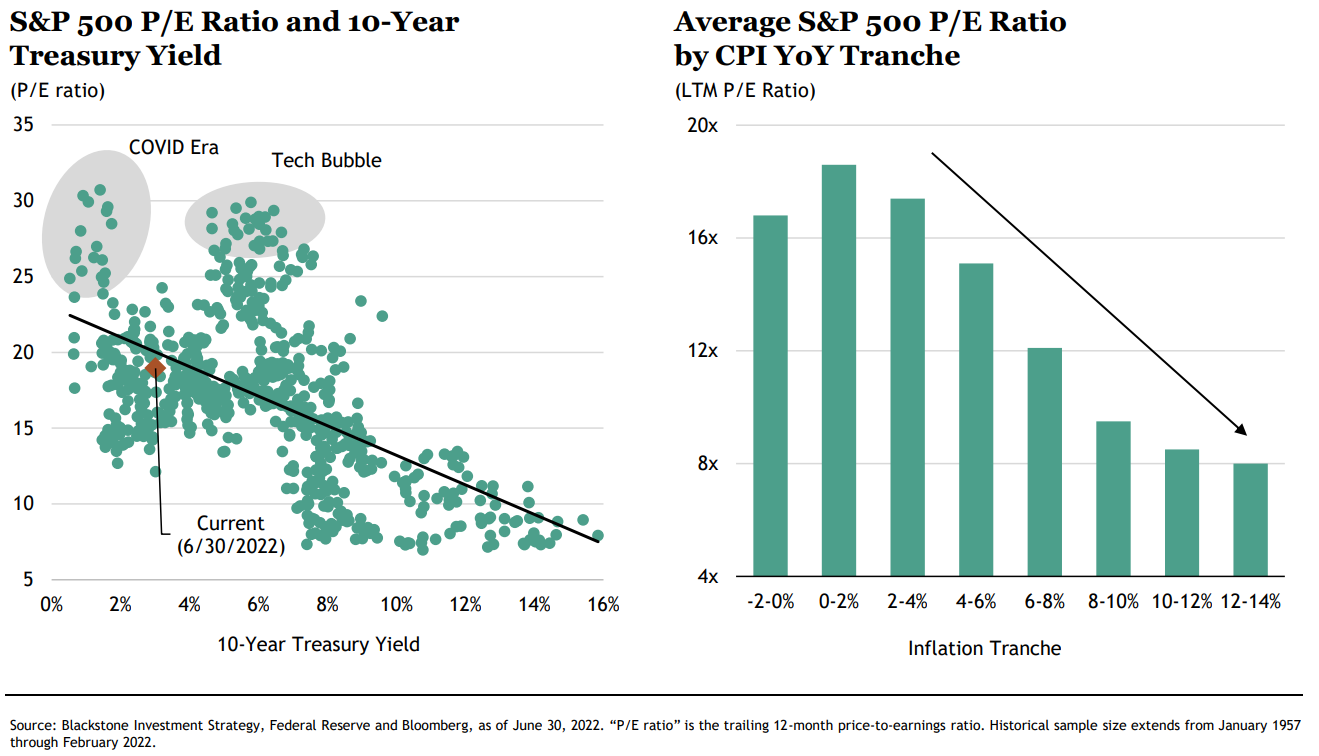

SPX is currently at 3966, 10Y treasury is 2.80%, trailing 12M earnings are around $220. I’ve highlighted where that gets us, down another 8%. Most interesting to note, valuation levels are far more sensitive to interest rates than earnings.

Another way to look at valuations. Blackstone thinks inflation will be stickier than expected and they will have to hike higher than the market expects to control that inflation. Therefor there is implied downside risk.

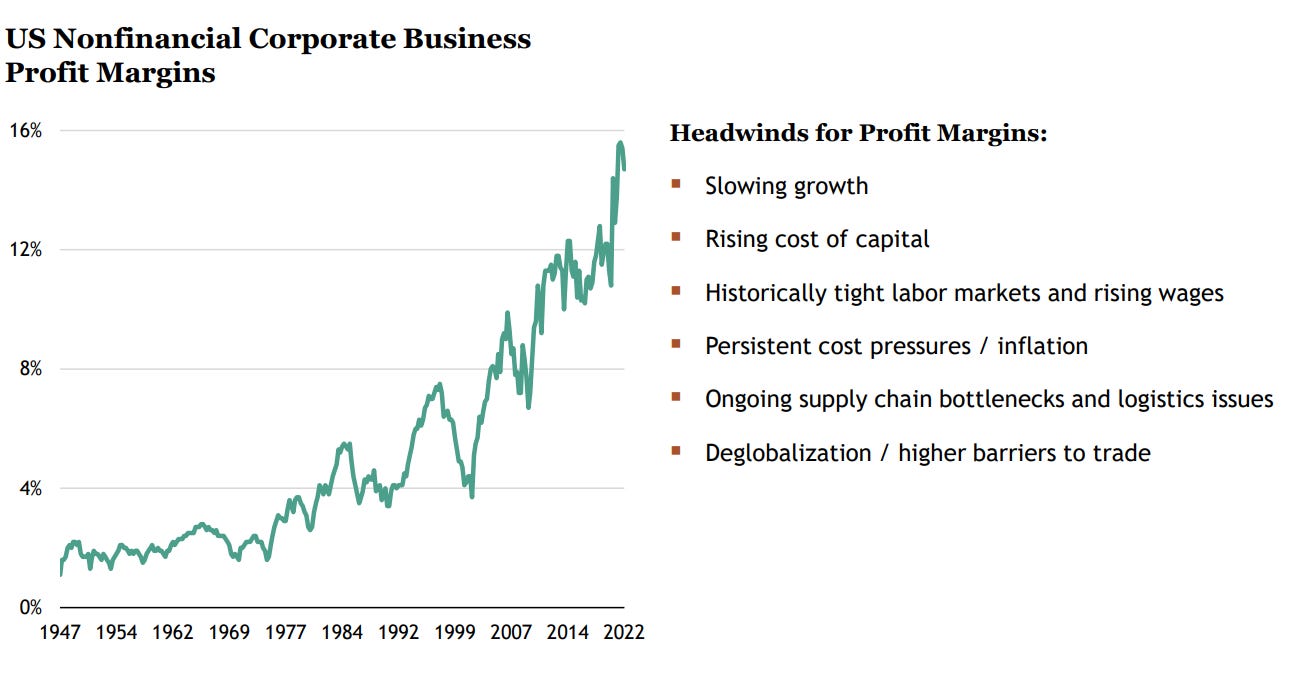

They also see some headwinds to warnings as the year progresses.

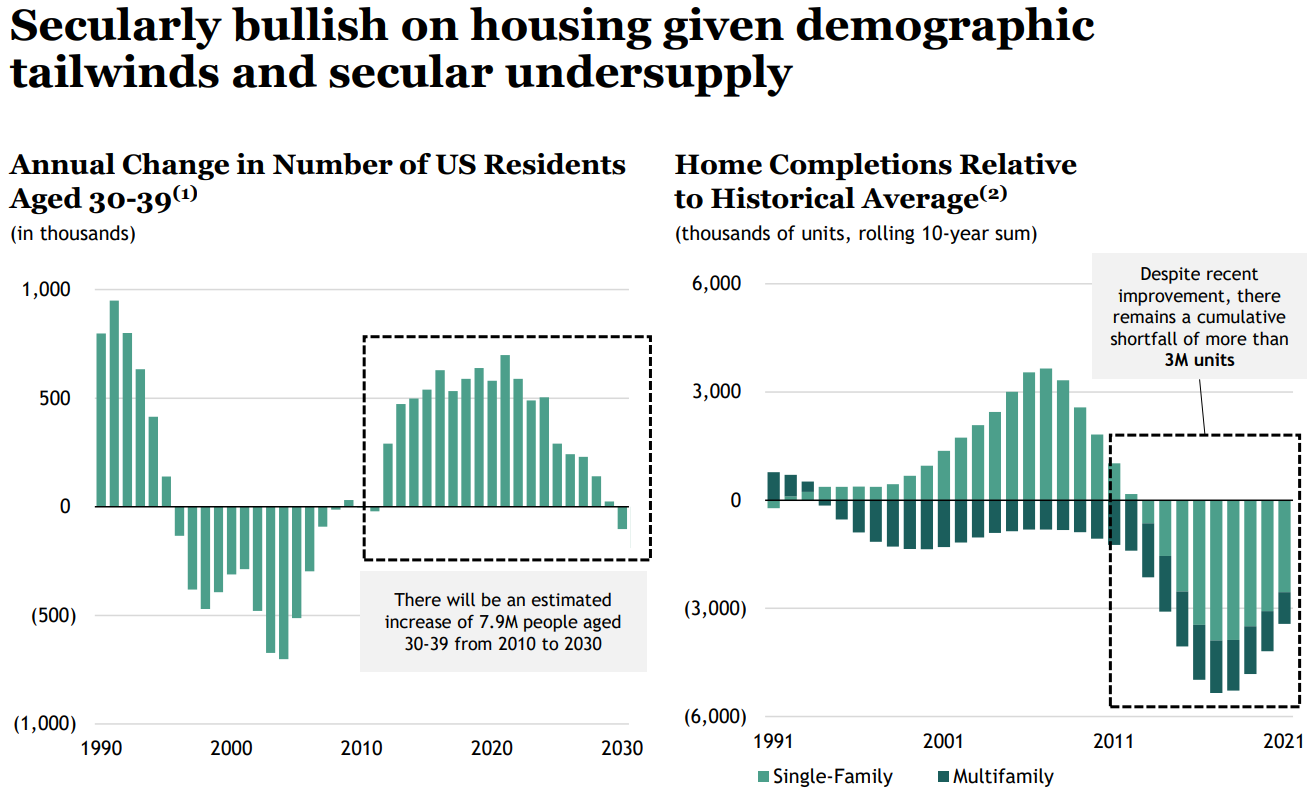

They are bullish US housing due to supply constraints. They also raised a $24 billion fund to target this opportunity. You could apply a similar thesis to Canada but US consumers have a larger ability to support current valuations.