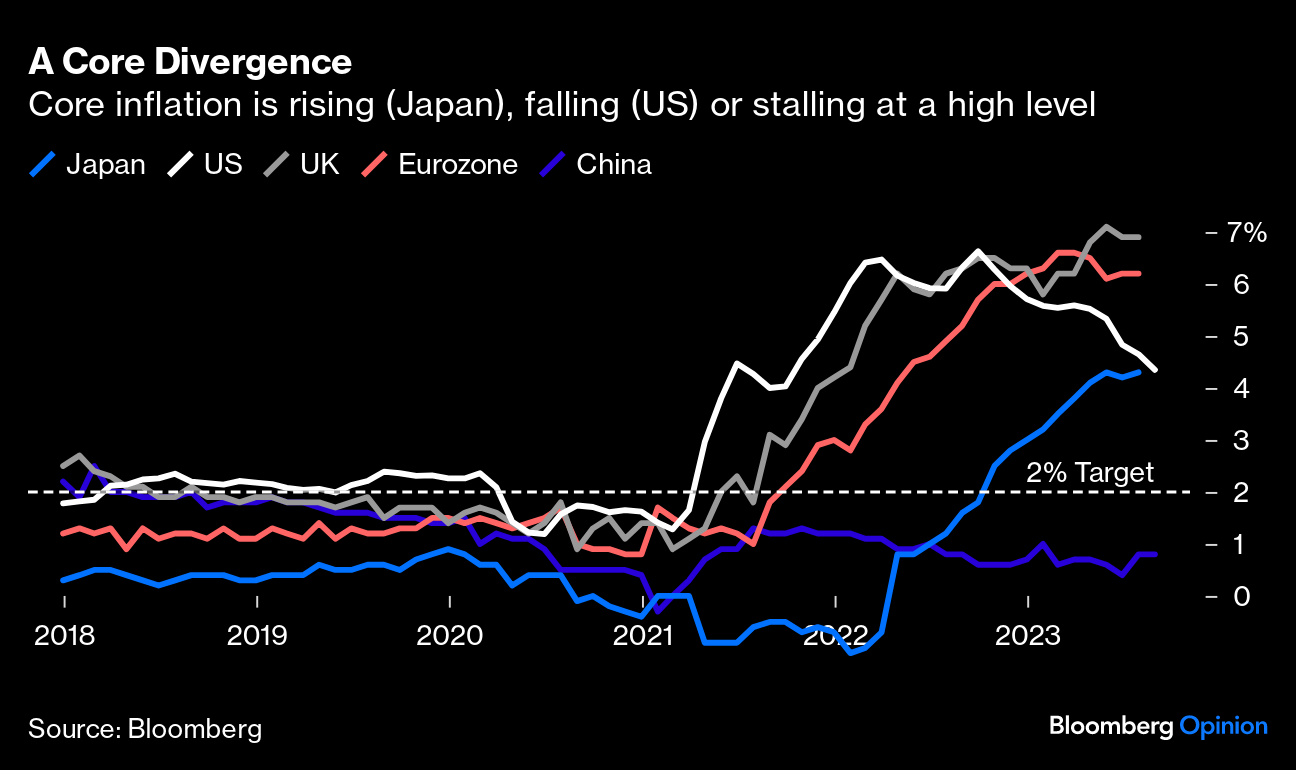

Daily Charts - Inflation Around the World

US 10Y yields briefly topped 4.5% for the first time since 2007. The S&P 500 notched its worst week since March. Markets struggled as they seemed to accept rates will be higher for longer following the Fed meeting. Speculative tech (ARK) was hardest hit but equity markets struggled across sectors. China was the lone bright spot on the week.

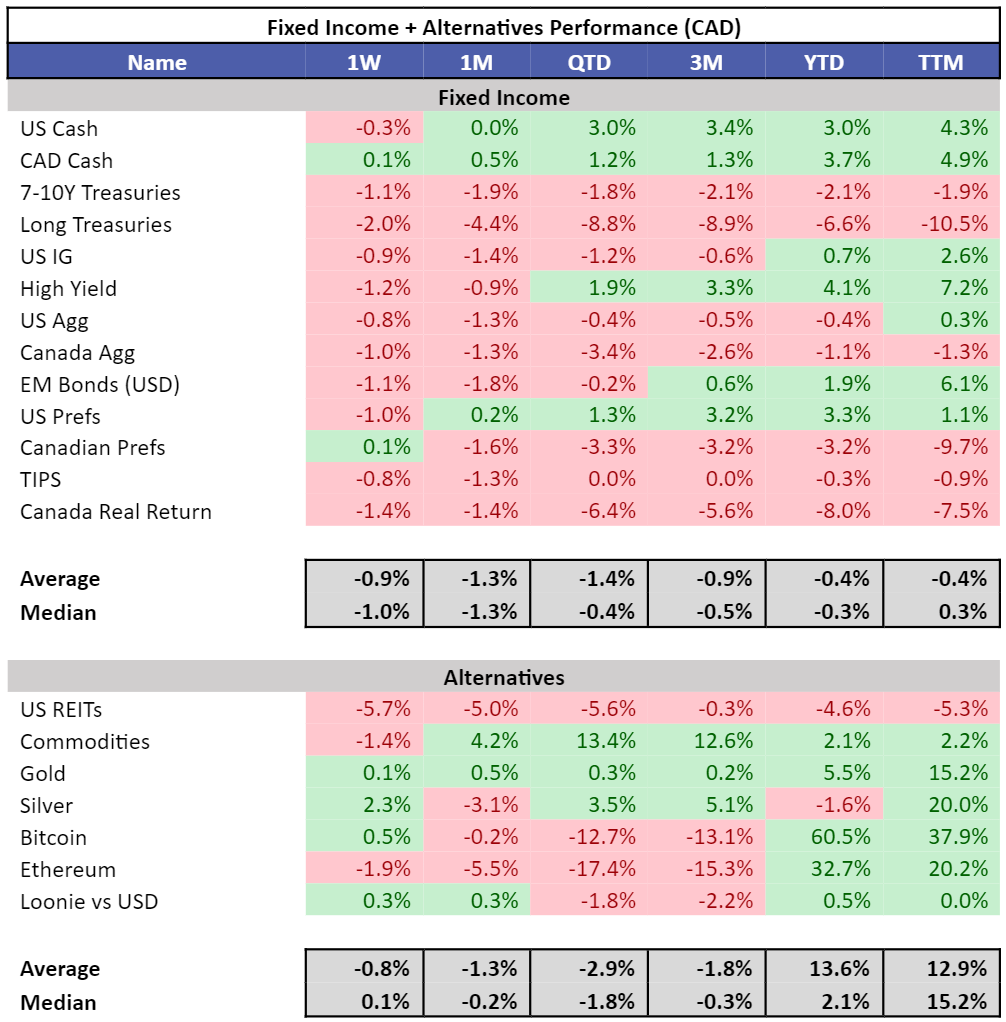

Rough week for fixed income, the Canadian 10Y was up 17 bps WoW on the back of Canadian CPI, US 10Y was up 10 bps WoW. REITS struggled, commodities took a pause.

Last week we saw the biggest daily surge in equity market vol since March, measured by the VIX.

US equities saw their largest weekly outflows ($17.9bn) since December 2022.

Outflows have been more pronounced in the S&P 493, the S&P 500 excluding mega cap tech.

As fears of a strong US economy and stickier than expected inflation appear, bonds and long duration treasuries are correlating again. Danger for traditional 60/40 portfolios.

Eyes are on the Bank of Japan as they decided to leave their yield curve control policy unchanged with inflation an issue. This will put pressure on the Japanese Yen, that is already down 11% against the USD this year.. A sign that their overly indebted government can’t support interests rates above 1%. The end game.

The Bank of Japan is the exception below who have hardly raised interest rates in an attempt to battle inflation.

Many components of the US inflation basket are still above the Fed’s target.

This is why you still have some of the banks forecasting a final rate hike in November.

The IMF released a paper exploring past inflationary regimes (FT Summary).

We document that only in 60 percent of the episodes was inflation brought back down (or “resolved”) within 5 years, and that even in these “successful” cases resolving inflation took, on average, over 3 years. Success rates were lower and resolution times longer for episodes induced by terms-of-trade shocks during the 1973—79 oil crises. Most unresolved episodes involved “premature celebrations”, where inflation declined initially, only to plateau at an elevated level or re-accelerate. Сountries that resolved inflation had tighter monetary policy that was maintained more consistently over time, lower nominal wage growth, and less currency depreciation, compared to unresolved cases. Successful disinflations were associated with short-term output losses, but not with larger output, employment, or real wage losses over a 5-year horizon, potentially indicating the value of policy credibility and macroeconomic stability.

Inflation only returned to pre-shock levels after a year in 12 out of the 111 inflationary episodes that the IMF examined, and in most of those cases it only happened because of a massive economic shock like the 2007-08 financial crisis or the Asian financial crisis of 1997-98. In other words they were not examples of “immaculate disinflation”. In 47 episodes examined, inflation still hadn’t returned to normal after five years, and for the balance the average time it took to bring inflation back to pre-shock levels was three years.

Another major wave of inflation is what the Fed is trying to avoid at all costs.

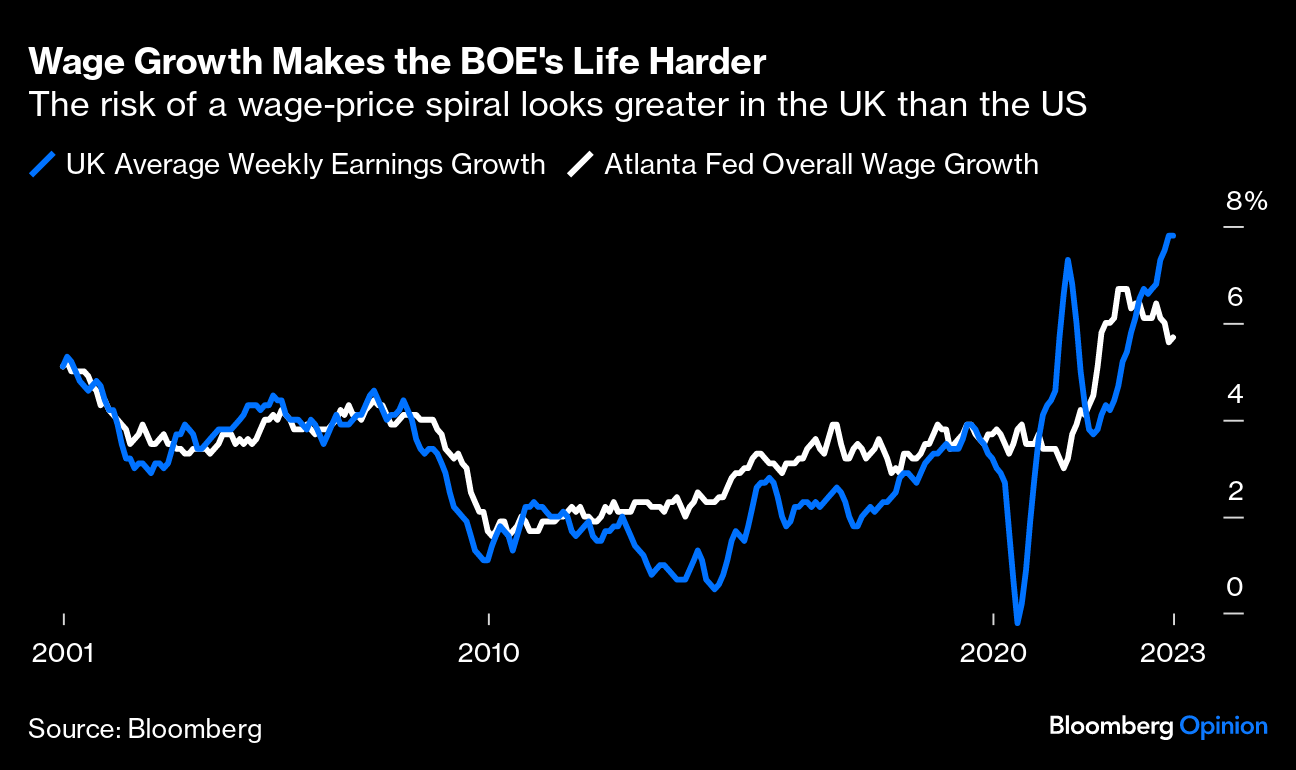

Situation is a bit more concerning in the UK where wage inflation is trending in the wrong direction. The US is still looking ok but the recent wave of strikes is cause for concern.