Double Trouble

It has been a horrible decade for value investors. This is a great example of a strategy outperforming for decades until it stops working one day. Will higher rates bring a renaissance for value strategies?

Busy day today with the CPI release and the Fed rate decision. Core inflation is expected to be flattish in May, with the median forecast of 0.28% MoM, 3.5% YoY.

JPMorgan’s S&P 500 reaction based upon where CPI comes in below. As expected, market only gets shocked if inflation surprises us.

Later this afternoon we get the Fed rate decision. No expectations of a cut until September. I’d expect Powell to be dovish as per usual.

Concerns around inflation running hot seem to have faded as oil prices have fallen. For now, risks of a resurgence in inflation like the 70s are in the rear view.

We aren’t completely out of the woods. According to Zillow, rent growth has picked up in recent months and who knows what will happen post election.

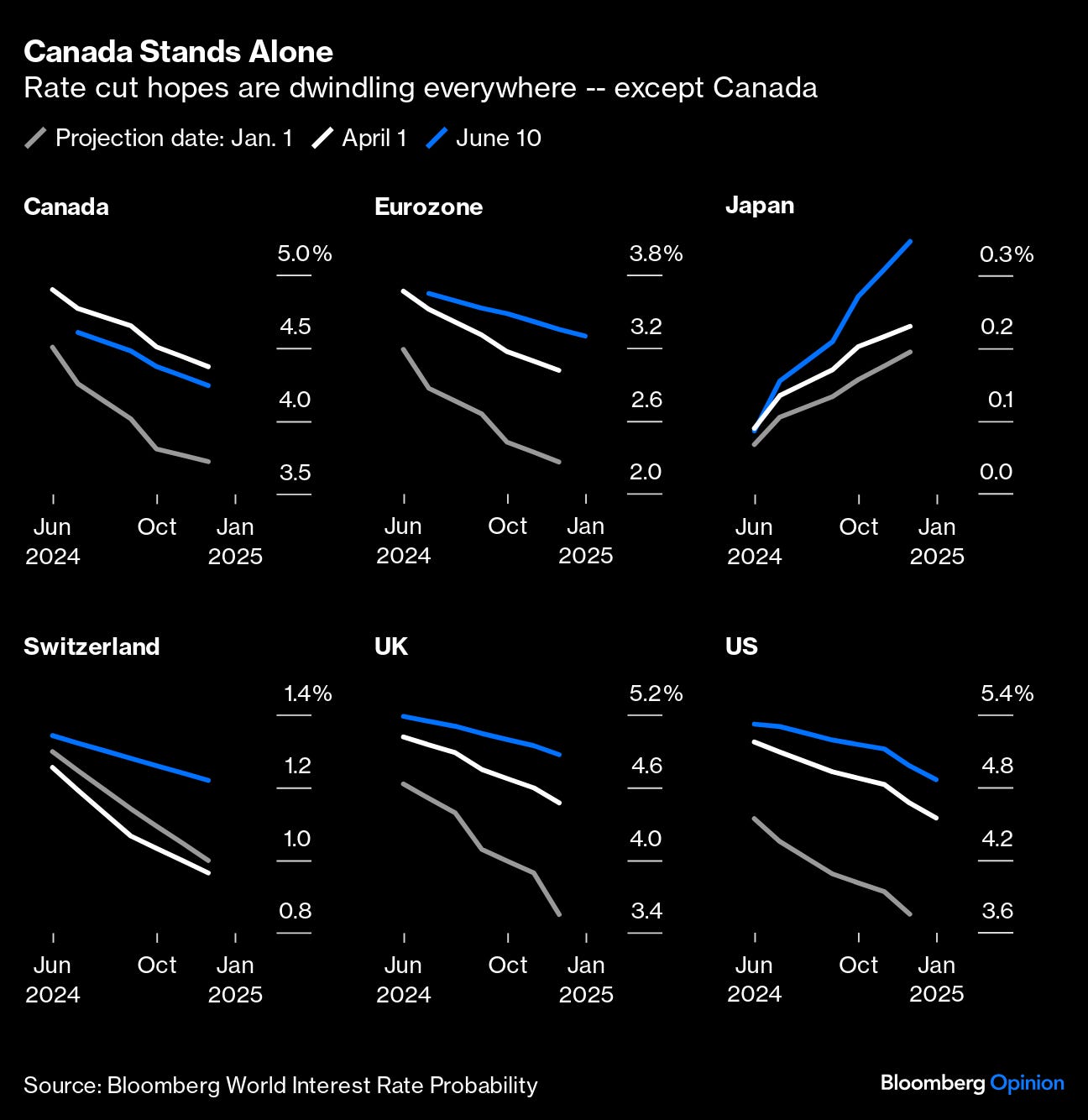

Canada is the only G7 nation where rate expectations are currently below where they were on April 1.

One thing economists have been consistently wrong about is the strength of the consumer. About 20% of survey respondents, about double the historic average plan to vacation abroad.

Auto sales remain strong, showing consumers are not delaying big ticket purchases.

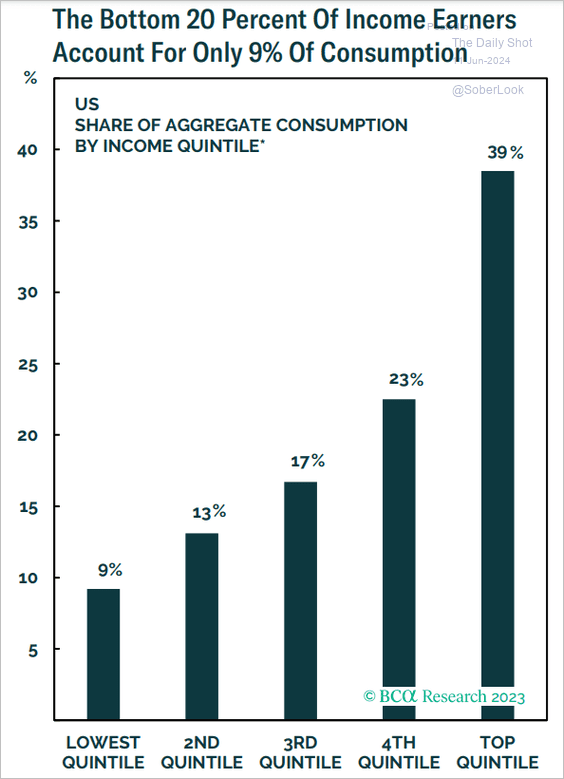

This is likely driven by the strength of higher earning consumers who make up the majority of consumption. Top 40% of consumers represent 62% of consumption.

Apple stopped innovating and consumers stopped upgrading. Majority of iPhone owners own older devices.

The US office vacancy rate hits a fresh record high of 19%, surpassing levels seen in both 2008 and 2020. Office would get annihilated if we see an unemployment cycle.

Even without a recession, real estate faces a steep maturity wall. They will try to extend and pretend wherever possible.

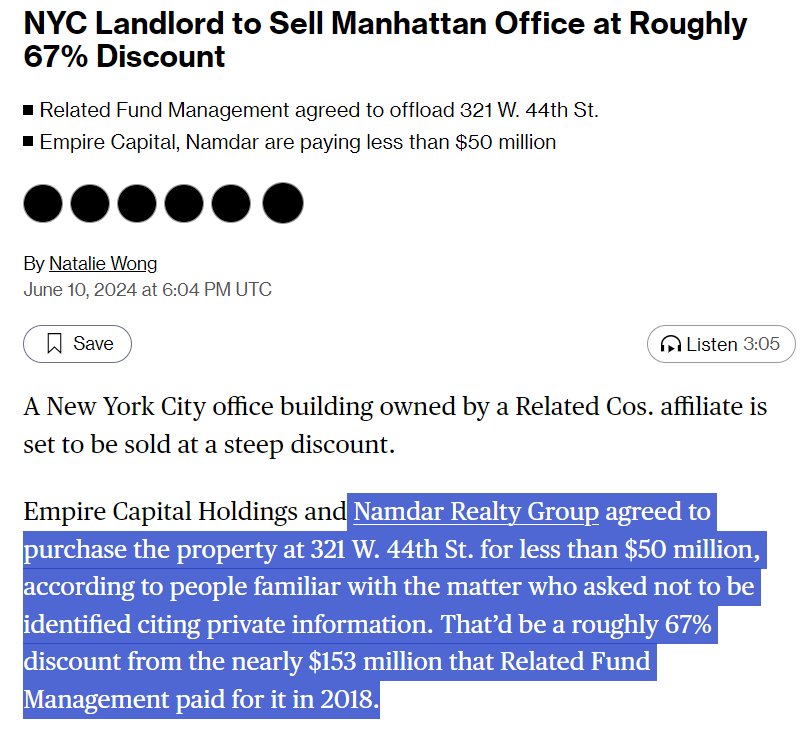

Not all properties will escape. We will continue to see headlines like this as long as rates remain elevated. Another Manhattan office building sells at a steep discount.

High yield spreads remain historically tight but the real yield investors are receiving is quite attractive compared to the past decade, driven by elevated base rates.