Electrons Shaping our Future

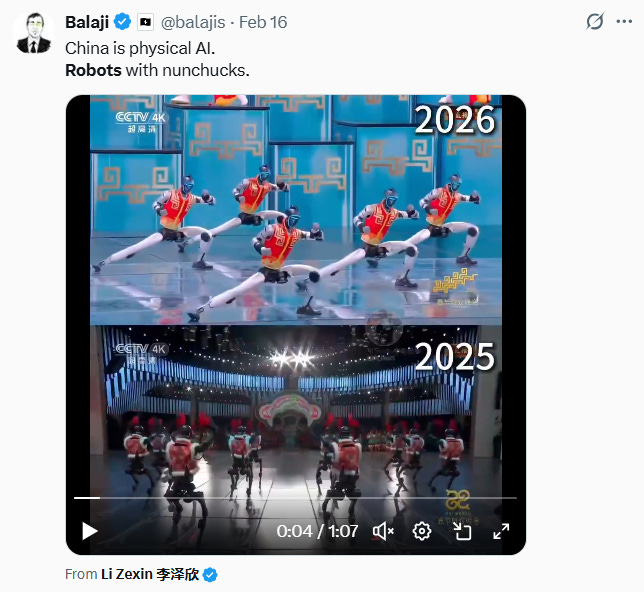

Videos from Lunar New Year went viral as humanoid robots performed flips and swung nunchucks with precision. The routine was preprogrammed, but the signal matters. This is a preview of where industrial automation is headed. Do we really think the U.S. will allow Chinese-built robots to operate inside domestic factories and public infrastructure? Highly unlikely. The next industrial race will be about control as much as capability. (link to video)

Some economists argue this is the new class divide. Those who learn to orchestrate AI compound their productivity and income. Those competing directly with it, operating below the API layer, face structural wage pressure. Technology has always created winners and losers. This cycle may move faster than the last. (@milesdeutscher)

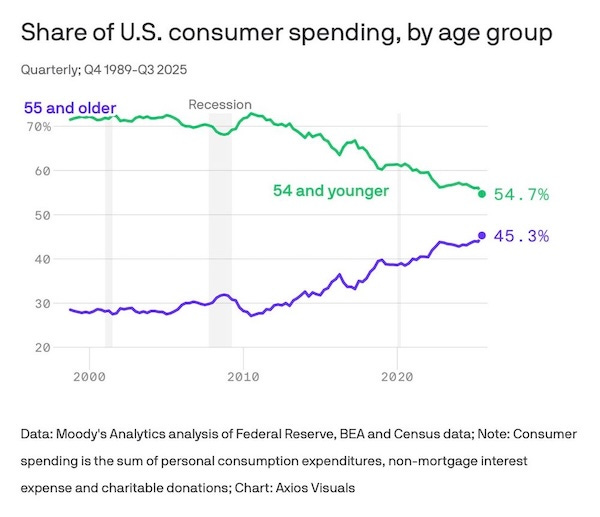

If you are starting a business, follow the demographics. Americans aged 55 and older account for 45.3% of total consumption. The spending power is aging. Build for where the demand already is. (Axios)

More jobs are being replaced by electrons than by people. Goldman estimates data centers now represent 7% of total U.S. power demand. Capital intensity is rising. Labour intensity is falling. The grid is becoming the new office floor. (@econcallum)

Virginia power demand +50% since 2020. Data centers are not theoretical. They are physical, power hungry, and scaling fast. (@MikeZaccardi)

Building an EV manufacturer is capital intensive and brutally competitive. Caught between the innovator’s dilemma and foreign competition, few survive the scale phase. Tesla remains one of the rare players to reach breakeven. Survival in this industry requires both technology and balance sheet endurance. (@alojoh)

The wave of capital raised by private equity has to be deployed. That has kept acquisition activity elevated, even after the 2021 surge. Buyout funds now hold roughly twice as many portfolio companies as they did in 2019. What has slowed is the rate of exits. Inventory is building. Liquidity is not. (iCapital)

The 2021 to 2022 window was defined by buyers willing to pay peak multiples. Global buyout firms paid an average of 11.5x EV to EBITDA in 2021, a record entry valuation. Since then, entry multiples have remained elevated. When assets are eventually sold, return compression becomes a real risk. Slower distributions make the next fundraising cycle more challenging.

Looking at the data on a five year lag highlights the shift. The 6.9x average entry multiple in 2010 aligned with a 10.9x exit multiple in 2015. From 2010 through 2020, exit spreads averaged roughly four turns of multiple expansion. Since 2020, that spread has compressed to about 1.6 turns. (iCapital)

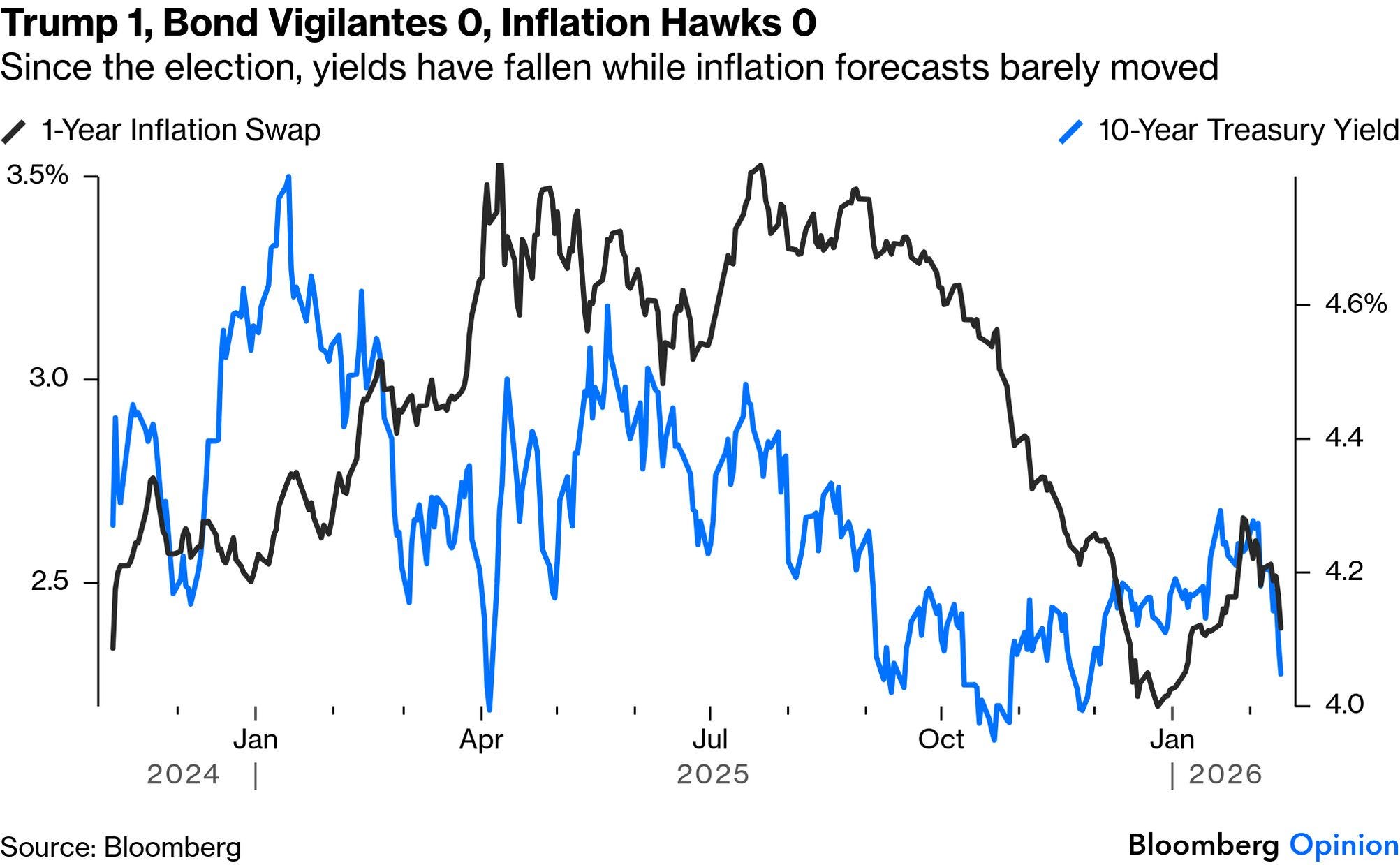

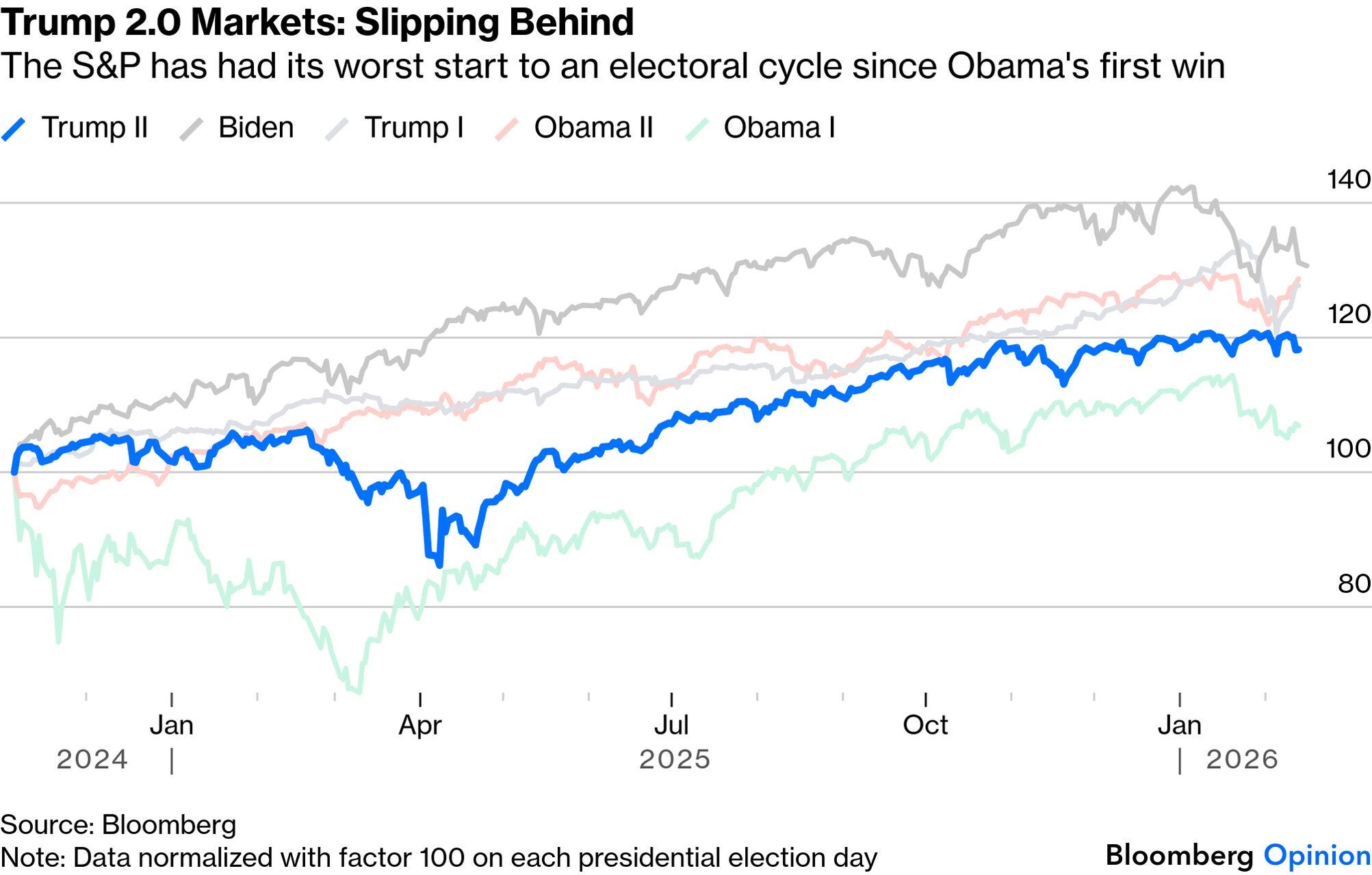

Since his election, Trump has managed to suppress inflation expectations and keep 10 year yields contained. Bond markets, at least for now, are not signaling panic. (John Authers)

Equity markets, however, have underperformed relative to the early periods of prior presidencies. Bonds have stabilized. Stocks have not re-rated in the same way. (John Authers)

The world may be drifting back toward TINA. There is no alternative. With 87 percent of global bonds yielding less than 5%, income investors are being pushed out the risk curve again. (Apollo)

The Toronto condo market looks like it is in real trouble, and it is hard to argue the bottom is in.

I still remember being told in 2021 that lending against Toronto condos was the safest asset class on earth. You tend to hear statements like that near the peak of a housing cycle. (Steve Saretsky)

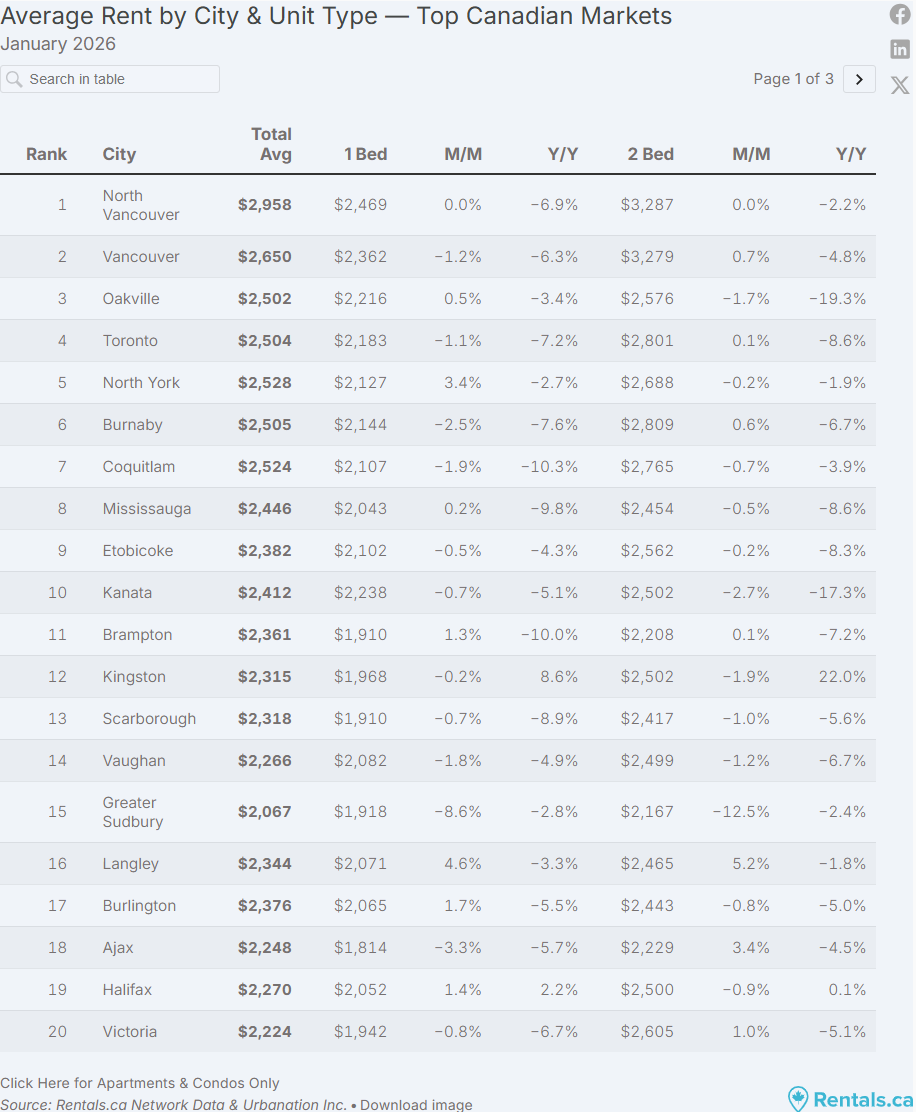

As population growth slows in Canada, rents are starting to fall. Housing affordability was never a market mystery despite political unaccountability. Policy choices shaped the imbalance, and policy choices are reversing it. (Rentals.ca)