Expensive Again

Strong earnings, solid economic data, and early visibility into 2027 capex supported equities. Initial jobless claims fell to their lowest level since the 1960s. MS AI Tech Beneficiaries posted their best month on record with MSXXAIB +40%. The Fed narrative shifted this week. The Committee moved away from an easing bias toward a more neutral stance. Global equities were up across the board last week, other than the U.K. Energy was the top performing sector, Materials was the worst.

10Y yields rose 7 bps in both Canada and the US. Brent crude climbed 10% on the week, lifting commodities. Precious metals sold off. Crypto was mixed. CAD may be starting to catch a petro currency bid.

Despite the law of large numbers suggesting growth limits, some of the fastest-growing companies in the U.S. are also the largest.

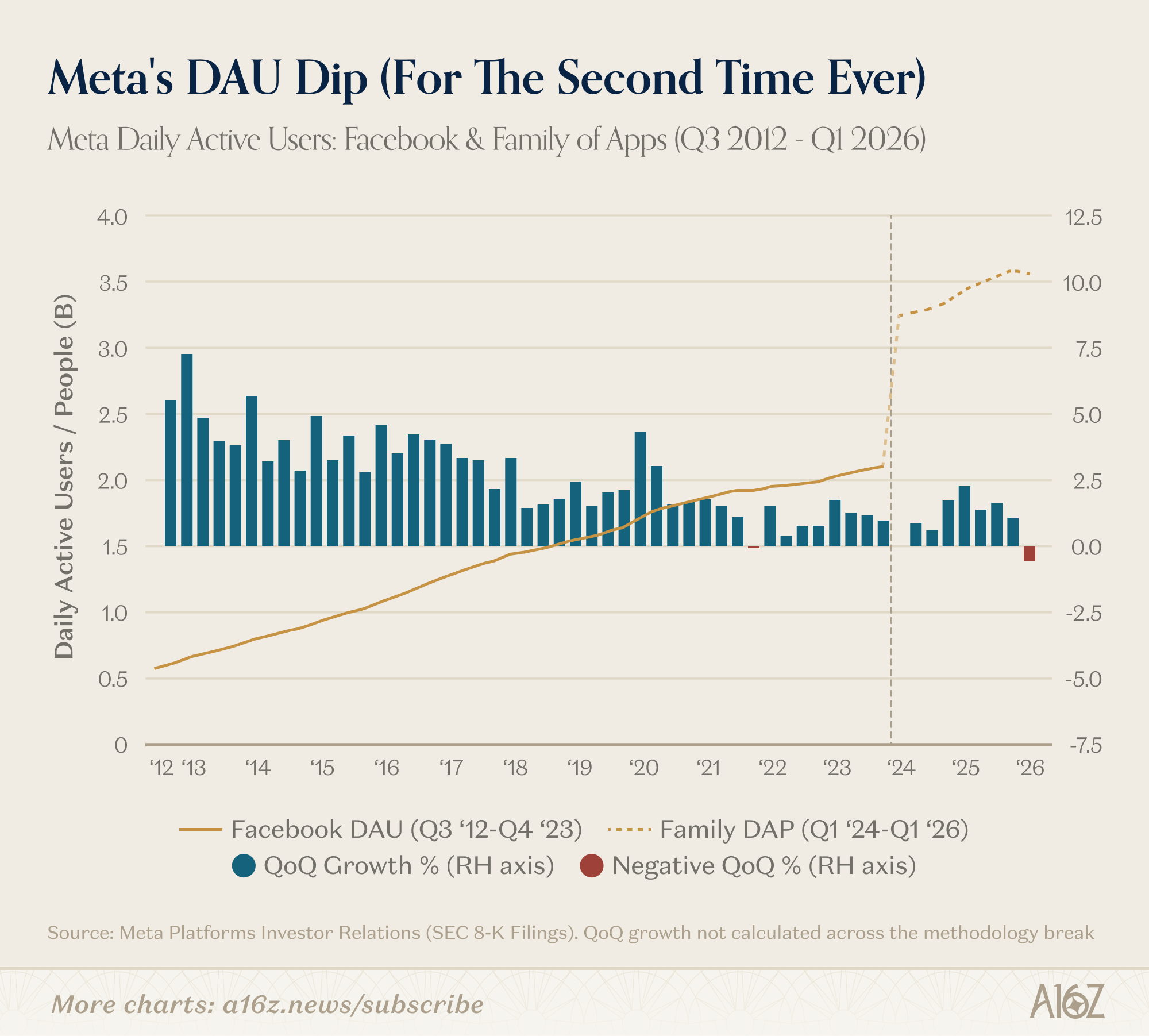

Meta’s users declined for only the second time ever. (a16z)

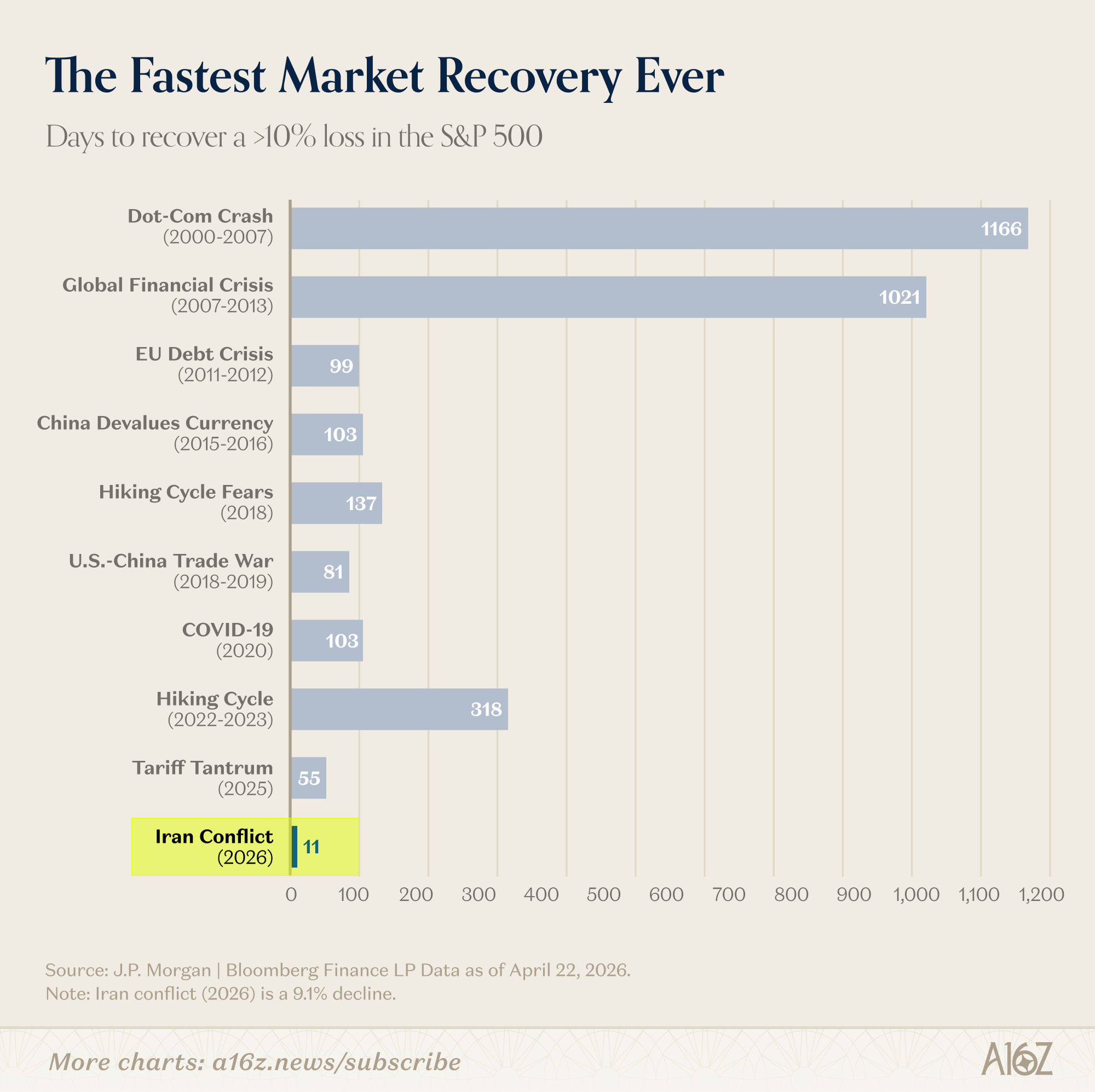

We just lived through one of the fastest recoveries from a sell-off on record. I imagine this reinforces dip buying behavior. When that dynamic eventually reverses, the unwind can be more severe.

Valuations are stretched again. A difficult setup for top down investors. It has not paid to be negative on equities, but when markets do correct there is little margin of safety.

Looking across valuation measures, the S&P 500 is approaching record levels. Not a call on timing, just a reminder of the starting point.

Markets have pushed higher even as Big Tech reallocates cash flow toward capex over buybacks. (@crescatkevin)

Industrials have overtaken Technology as the largest recipient of flows over the past 12 months.

They are now trading rich relative to history.

Amid the sharp rebound in April, global fundamental long short managers delivered their best monthly performance since 2016. There is clearly beta across these managers. Performance dispersion also widened meaningfully. Systematic long short strategies have shown a more consistent, less directional return profile.

Tech layoffs picked up in Q1.

Oracle was the largest trimmer. The question is whether other hyperscalers follow by cutting lower priority projects to fund capex.