Fading Headlines

Oil markets are currently pricing in a short-term disruption, as reflected in the current term structure. The move has been concentrated in near-term maturities, with prices for end-of-year contracts rising only about $3 per barrel.(@MikeZaccardi)

Goldman expects shipping through the Strait of Hormuz to resume next week, with operations fully normalizing by mid-April. (@MikeZaccardi)

Equity markets took their cue from oil and rebounded yesterday as investors faded the latest escalation. Being bearish can sound smart, but buying the dip and fading geopolitical risk has worked repeatedly in recent years. In reality, it is difficult to have a clear edge in moments like this.

Below is an excerpt from PauloMacro:

On the day of the Russia invasion, the S&P 500 gapped down but somehow finished up +1.5%, retested those lows, and then rallied into the end of the quarter. Only then did it absolutely crater through mid-2022.

and Oil spiked ~$8/bbl from $92 to $100, but gave it all back to close flat. The very next day, it was trading at $90—lower than the night before the invasion. Then, just 6 days later, it touched $130.

The big difference here? Russia was exporting 4-5 mb/d back then with zero actual supply loss; they actually pushed more crude onto the water throughout 2022.

Meanwhile the Middle East exports ~15 mb/d through Hormuz, and right now, flows have basically stopped. And unlike Russia, there’s no floating storage to act as a buffer.

That’s the whole story. We should probably stop getting so bogged down in the daily noise and focus on what's actually going down in the real world.

History doesn't have to repeat the 2022 playbook, but it’s definitely something to chew on.

Spiking oil prices have historically been capable of pushing the global economy into recession. (ISABELNET)

It was the best of times…

The past 3.5 years have been about as good as it gets for S&P 500 investors relative to the past 100 years. (@MikeZaccardi)

It was the worst of times… For Tech investors.

At the same time, this has been some of the worst relative underperformance for Tech investors in the past 50 years. (@MikeZaccardi)

Even with the recent outperformance, European equities continue to trade at a significant discount to U.S. markets. (@MikeZaccardi)

Euro area unemployment is at over 25 year lows. (@neilksethi)

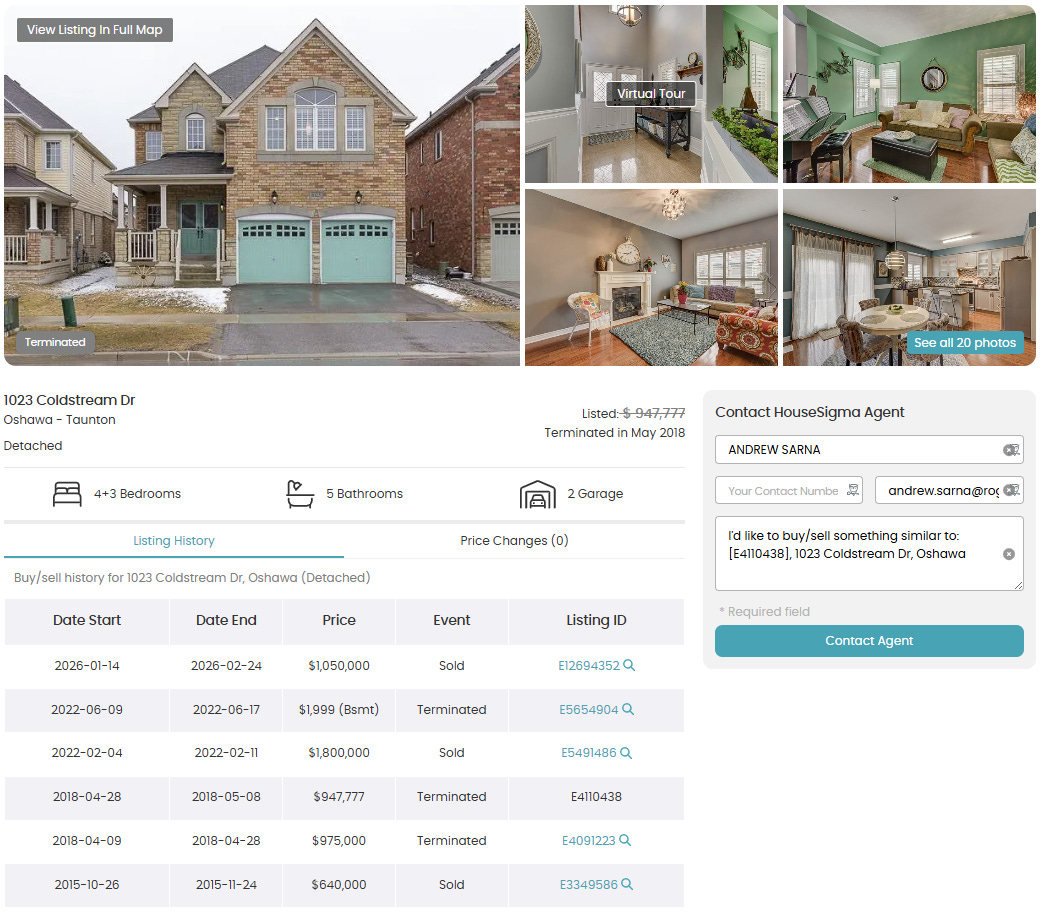

This is wild. A house in Oshawa (Greater Toronto Area) sold at a $750k loss, changing hands for $1.05M just 3.5 years later.

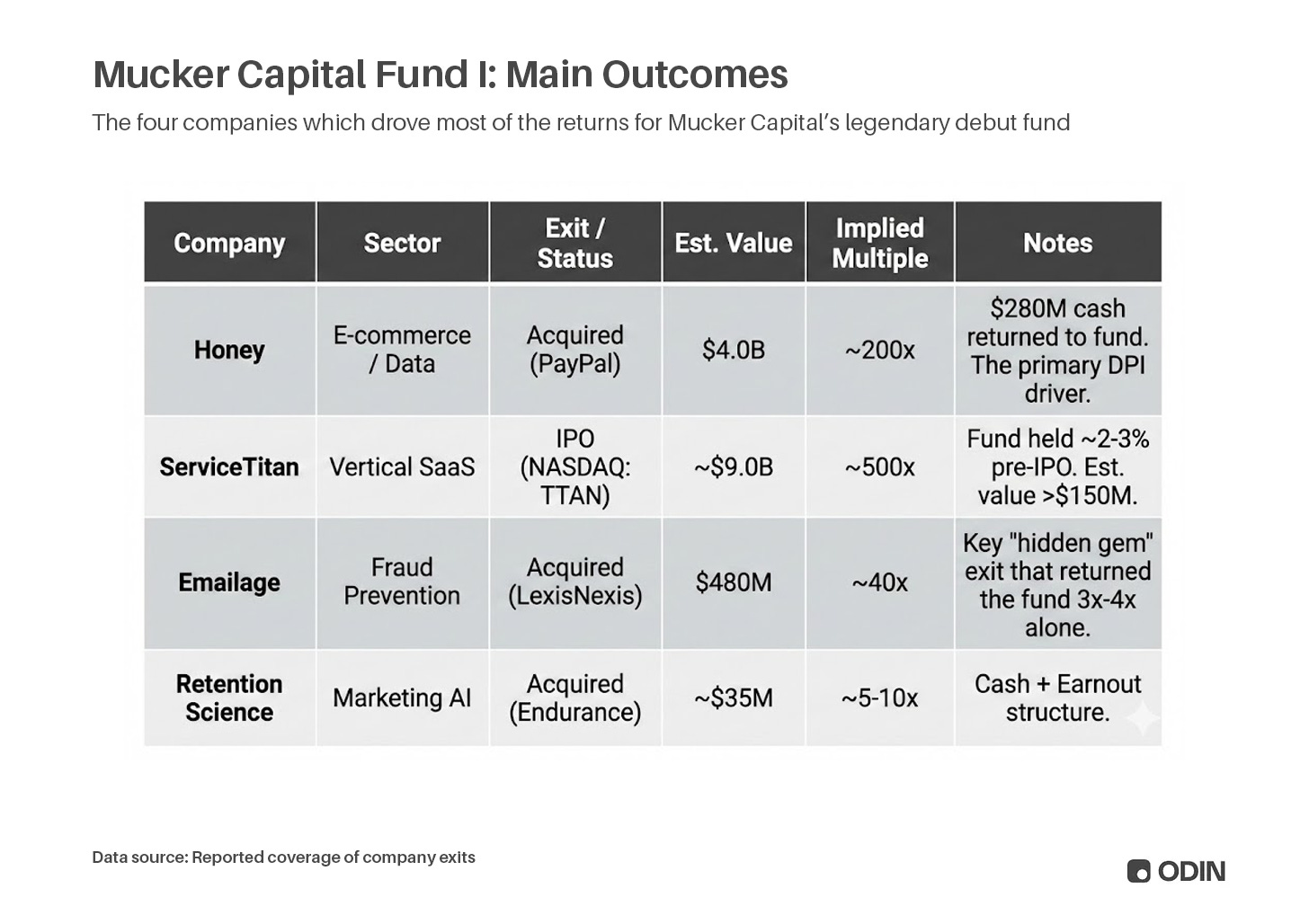

Interesting story about one of the best Venture funds ever, you have never heard of (estimated 43-53x).

The fund produced both a 200-bagger and a 500-bagger inside a $12M vehicle fund.

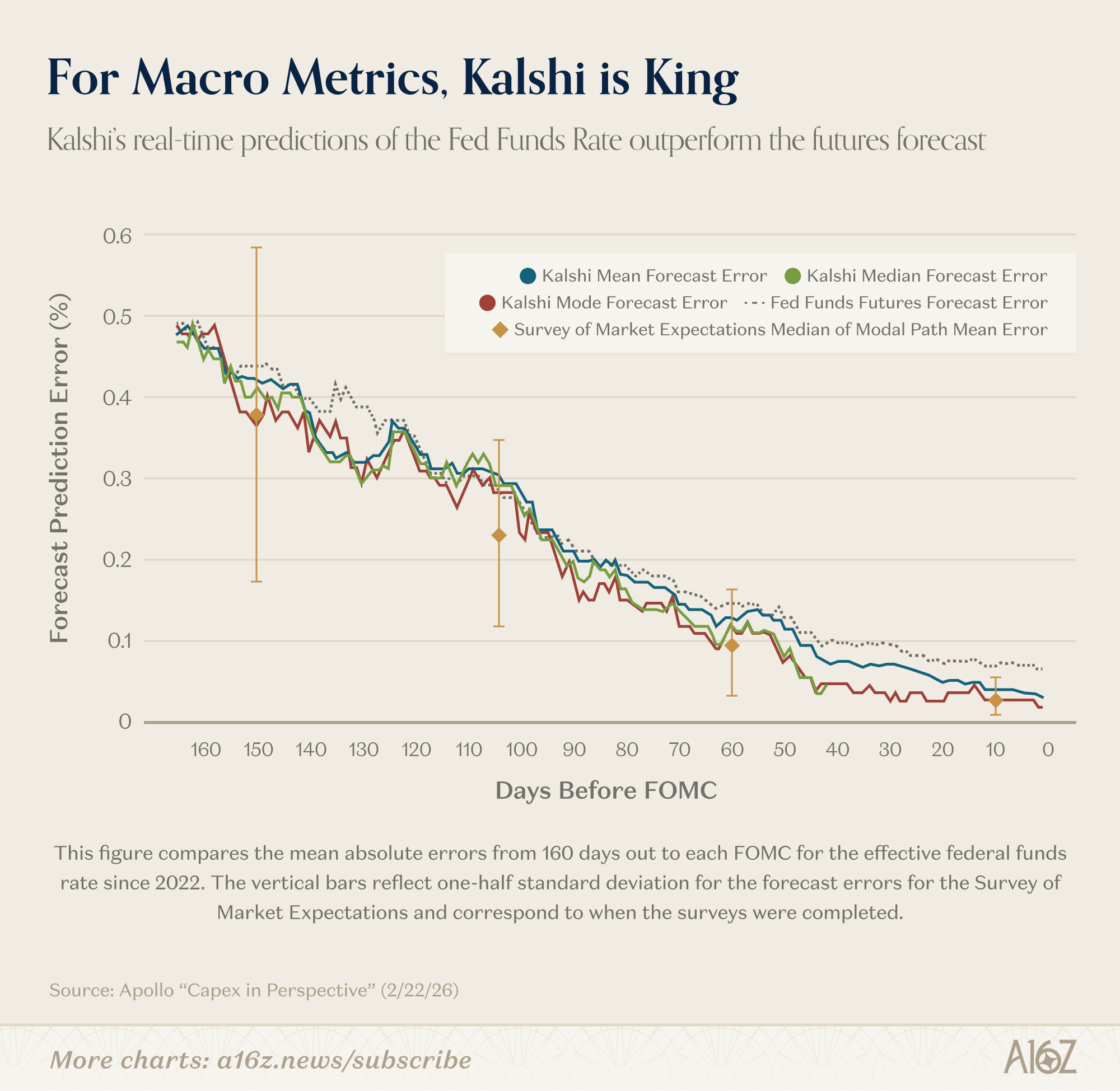

Prediction markets are doing a better job pricing economic forecasts better than the pros:

For the federal funds rate forecasts 150 days (3 FOMC meetings) ahead, Kalshi’s mean absolute error is very similar to that of professional forecasters. But unlike the survey—which provides a snapshot every six weeks of a modal path—Kalshi offers a continuously updating full distribution

. . . We find the Kalshi median and mode have a perfect forecast record on the day before the FOMC meeting, which represents a statistically significant improvement over the fed funds futures forecast.

In other words, while all the forecasters start out about the same, Kalshi’s “continuously updating” forecasts get better and better over time, culminating in a “perfect forecast record” on the day before rates are officially declared. Plus, Kalshi did better than the futures forecast. (a16z)

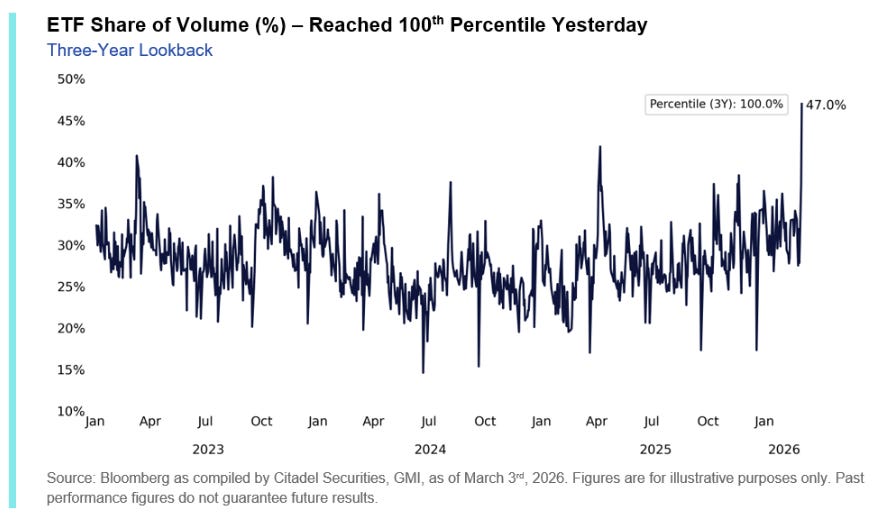

ETF volumes reached 47% of total market trading yesterday, marking a new five-year high. This suggests investors are increasingly using ETFs for hedging and tactical positioning while maintaining their core exposures.