H4L + AI Value Capture

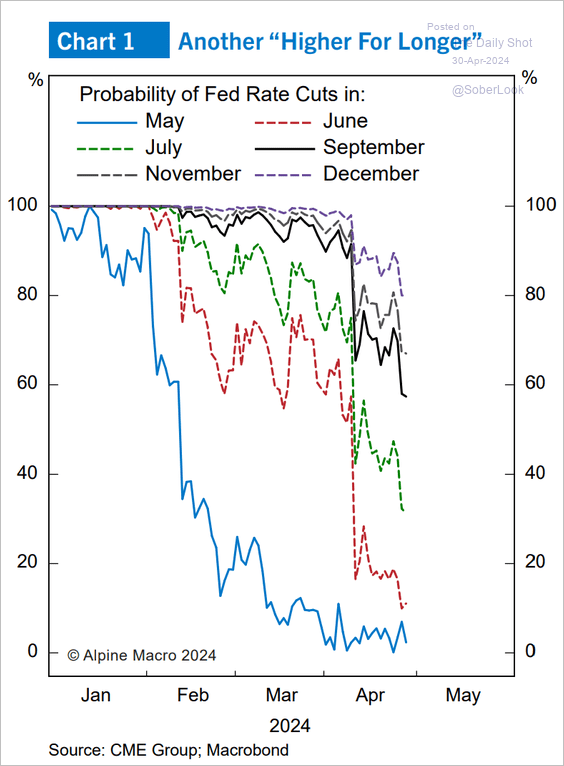

I thought they were going to pump markets into the election, seems like I will be wrong. We will get confirmation today with both the QRA and the Powell presser. Early indications from Nick Timiraos (Fed mouthpiece), suggest a more hawkish tone from Powell.

The Biden administration would have liked to have seen strong markets into the election but they overdid it on stimulus, we peaked to early and now the telegraphed pivot from December will likely be delayed.

Yields across the curve have marched up since the start of the year and are beginning to take a bite out of asset markets. The longest duration, most speculative assets are the first to fall, Bitcoin off 20% from its highs.

Market is even beginning to question rate cuts by the end of the year. The cut in June is being given less than a 20% probability

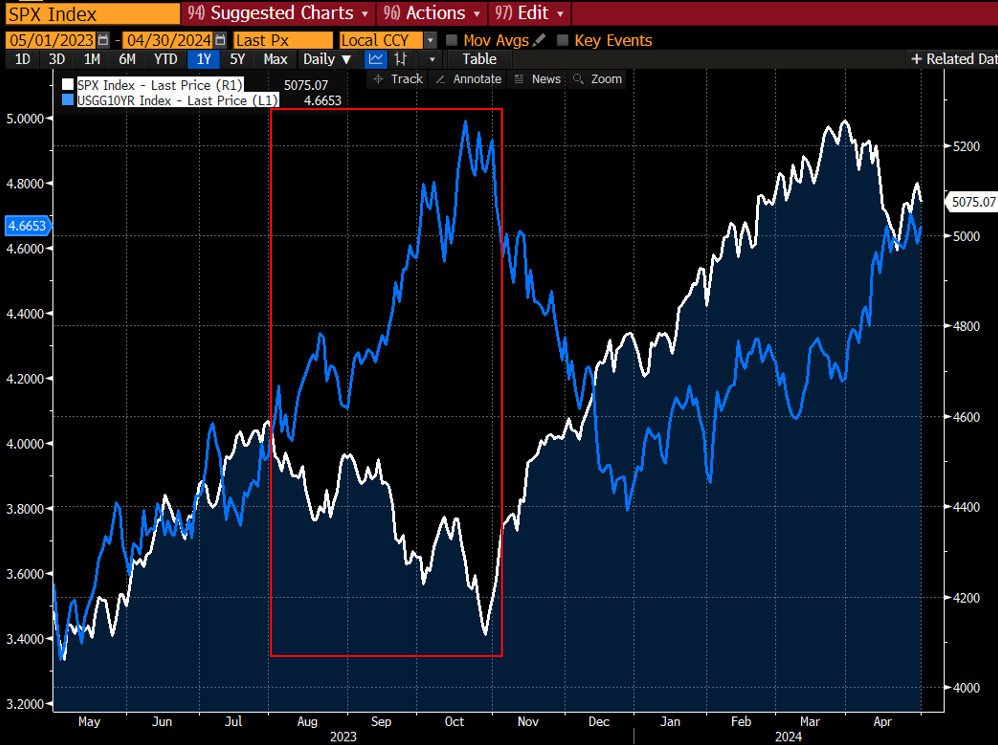

At this rate, we will continue to see price action like we saw late last summer until inflation and the economy give reason for yields to reverse or something blows up. It could be a bumpy ride until then. S&P 500 (white) and US 10Y (blue) pictured below.

Post Meta earnings I’ve been thinking about the magnitude of their capex spend. Maybe the proper analogy is the capex cycle that built the infrastructure for the modern internet. It wasn’t great for returns for those building out fiber networks but was a net benefit to society as it created the foundation for the internet. It is still very early but hard to see revenue ops today justifying the capex spend.

Moment in history, perhaps most recently incarnated in the Internet boom and bust period of 1999-2002. The capex cycle then was spent on fiber optic cable to build out huge amounts of capacity ahead of expected demand for internet services. Again, the capital spend was of epic proportions. In 1996 fiber optic cable extended one million miles in the US. This surged to 10 million miles by 2000, according to the Federal Communications Commission, with new companies like WorldCom and Global Crossing raising mountains of debt to finance the build. When WorldCom went bust in 2002 it had USD 100 billion of debt; Global Crossing had USD 25 billion.

The Dell’Oro Group anticipates USD 500 billion of datacenter capex in 2027 (Source).

The BG2 podcasts dives into some of these questions further. New Meta/Llama model is 10x cheaper than the OpenAI model and there are minimal switching costs. They also flag that Meta’s new model is free, pressuring the $20/month OpenAI charges for their newest model and that approach to monetization.

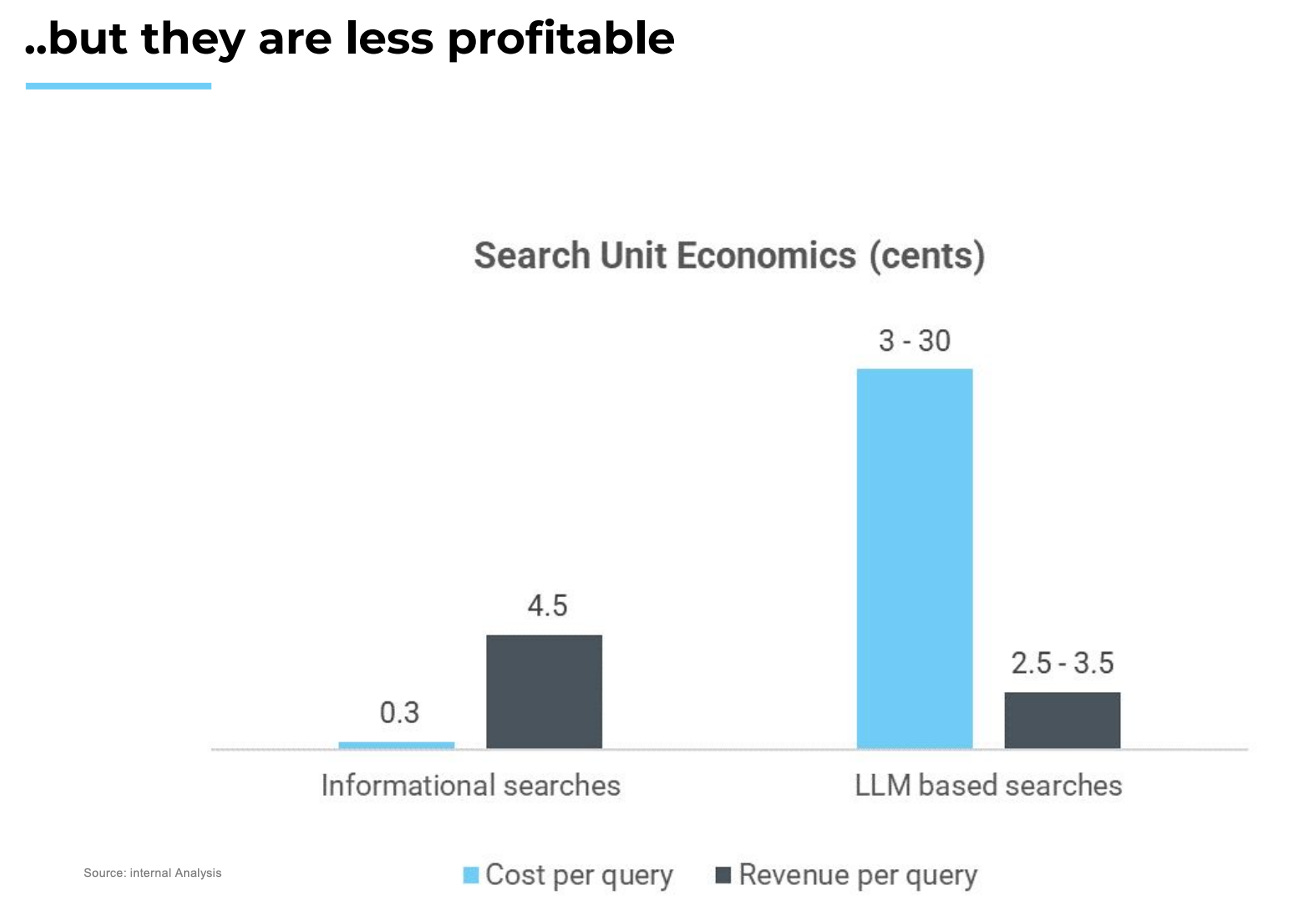

A concern some investors are beginning to focus on is the increased power consumption of AI. ChatGPT queries are 6-10x more power intensive than traditional search.

The build out of new GPU/AI dedicated data centers is expected to triple power demand from data centers from 2020 to 2030.

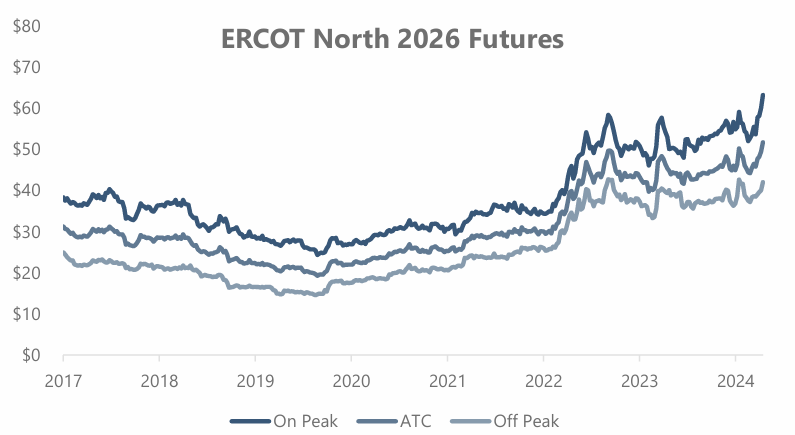

Power futures are beginning to price this reality in. Below, you are looking at the price of power in 2026 for Dallas, the second largest home to data centers in the US. This will become a bigger issue as build outs continue.

The increased power consumption means that AI queries cost much more than traditional search but tech companies also haven’t figured out how to monetize these queries with as many ads yet.

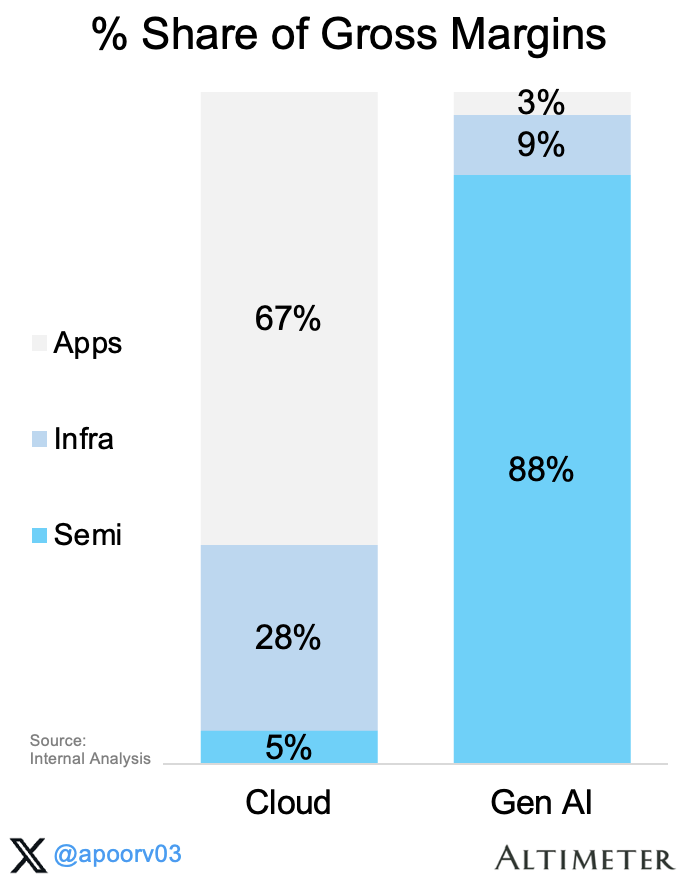

This leads us to our next question. Where does value accrue in AI? Today, the AI stack seems to be A-shaped vs V-shaped for cloud. Over time, will the GPU/semis market become more competitive or will apps figure out how to capture more value? Back to the fiber analogy, the market didn’t have a clue about the Ubers and Facebooks being built when the fiber was being laid in the ground. Nvidia/Semis are currently generating the most revenue and profits as infrastructure is being built out.

On the podcast, they discuss how competitive industries will have to pass along any AI savings to the consumer but markets where there is a dominant player will benefit adopters who can capture some of those cost savings without passing them on to the end user.

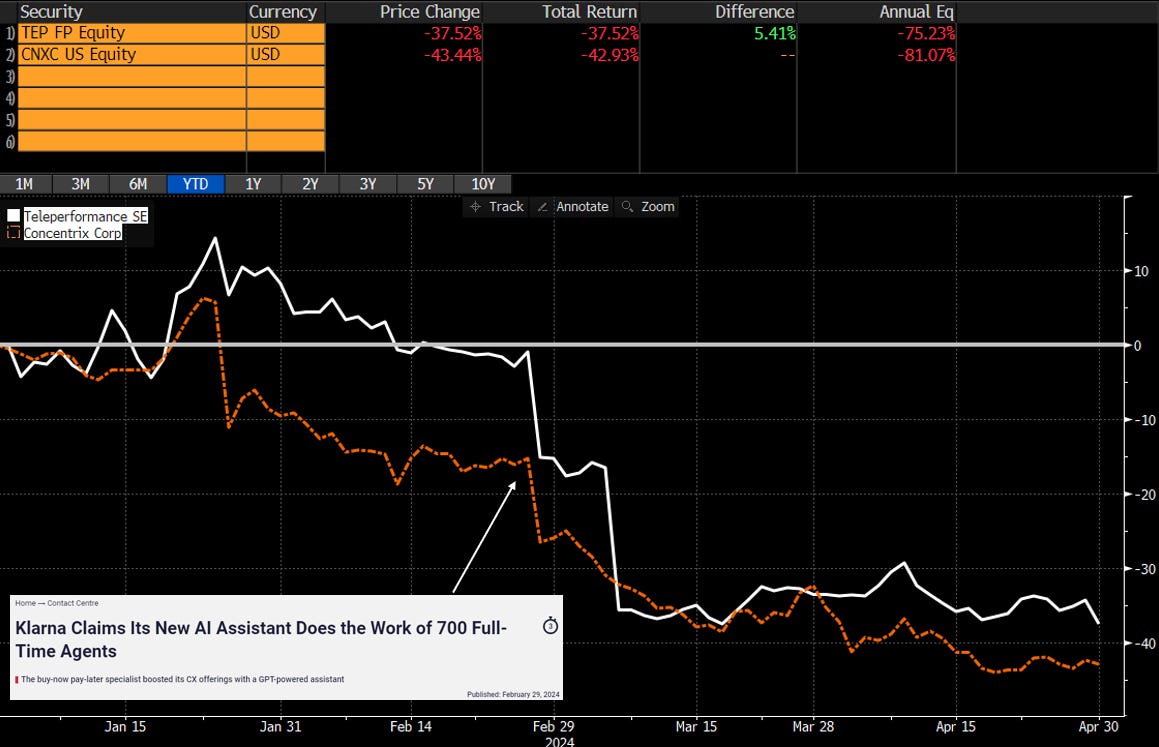

An example of value creation/destruction is associated with an early use case for AI, call centers. In late Feb., Klarna announced they were replacing call center head count with AI. Klarna reduced some costs and will capture some value but, this put serious pressure on two publicly trade call center companies, both down ~40% on the year.

Visualizing the distribution of profits through a bar chart. Can Nvidia continue to capture this much value? If the market ends up maturing similar to the cloud market, apps invented down the line will ultimately capture more of the AI markets value.

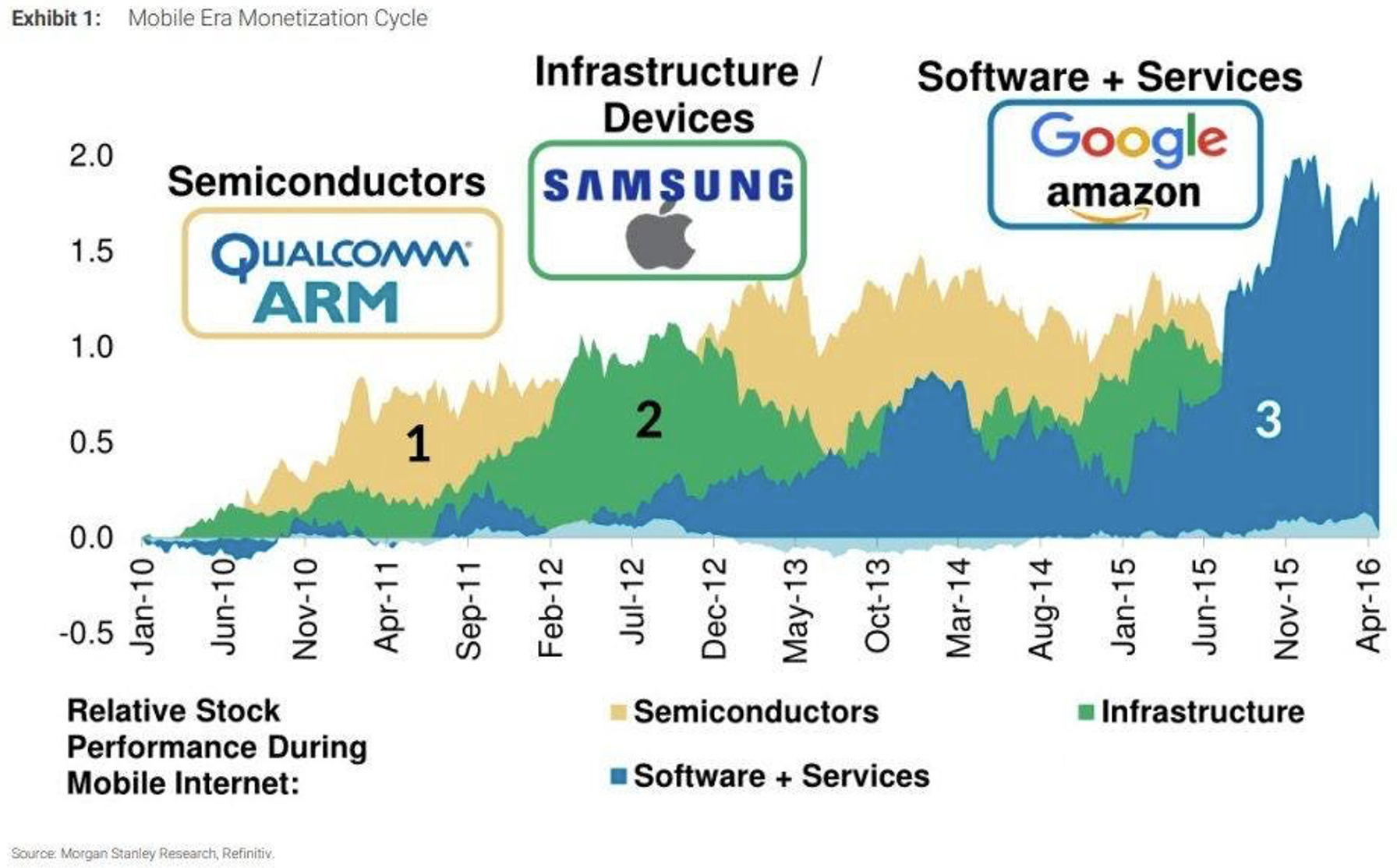

Looking at the mobile market’s monetization cycle, chips captured the value early on but eventually most of the value was captured by software and services built on top of the ecosystem.

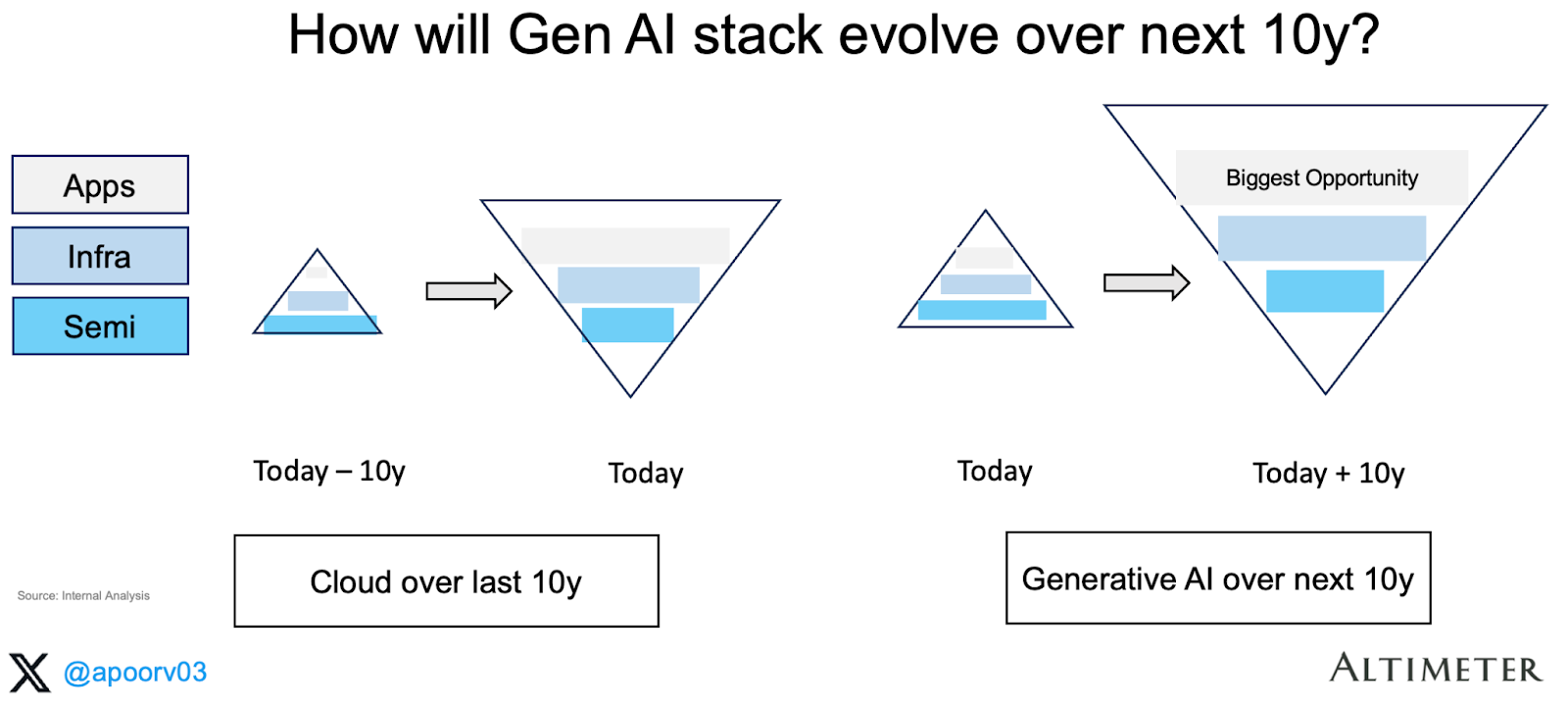

Altimeter believes the software, services and apps built on top of AI is the biggest opportunity in the future.

Very interesting topic about AI! Just my two cents regarding the accrued value of Gen AI. Maybe it's still too early. Is it possible that cloud and mobile were also in the A-shape at the beginning? Gen AI is still at it's early stage - launch/introduction, and I think the bottleneck in the industry is shifting from hardware to software. I suspect it will eventually turn V-shaped when legit use cases boom.

For AI power consumption, doesn't it look like the BitCoin, which consumes more power but generates less marginal gains?