Hostage to Hormuz

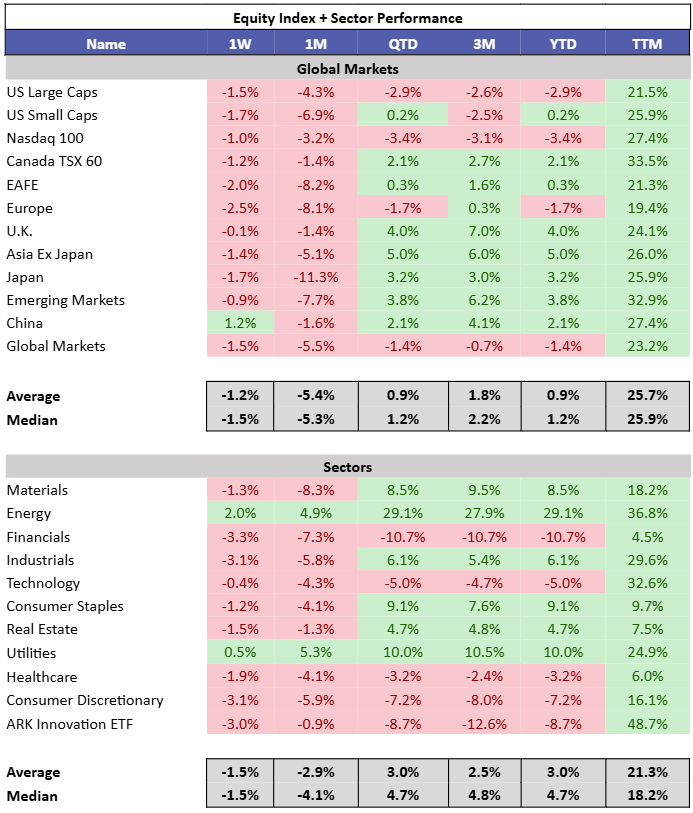

Back in the saddle after watching markets from afar last week. It was a tough stretch for global equities. Energy and Utilities were the only sectors that managed to finish in the green.

Right now it feels like markets care about only one thing: the magnitude and duration of the disruption coming out of the Persian Gulf.

The immediate impact on oil markets is obvious. The second-order effects are where things start to get interesting. Aluminum smelting, fertilizer production, semiconductor manufacturing. All supply chains that rely on exports from the Persian Gulf.

For now, markets still seem to be betting on resolution rather than a prolonged blockade of the Strait of Hormuz.

If that proves correct, the narrative likely snaps right back to the regularly scheduled programming: the global AI capex arms race. Reuters reports that Meta may consider layoffs affecting up to 20% of the workforce to fund AI infrastructure. Oracle was one of the first companies to openly acknowledge a similar reallocation of capital, rationalizing parts of the business to redirect spending toward AI buildout.

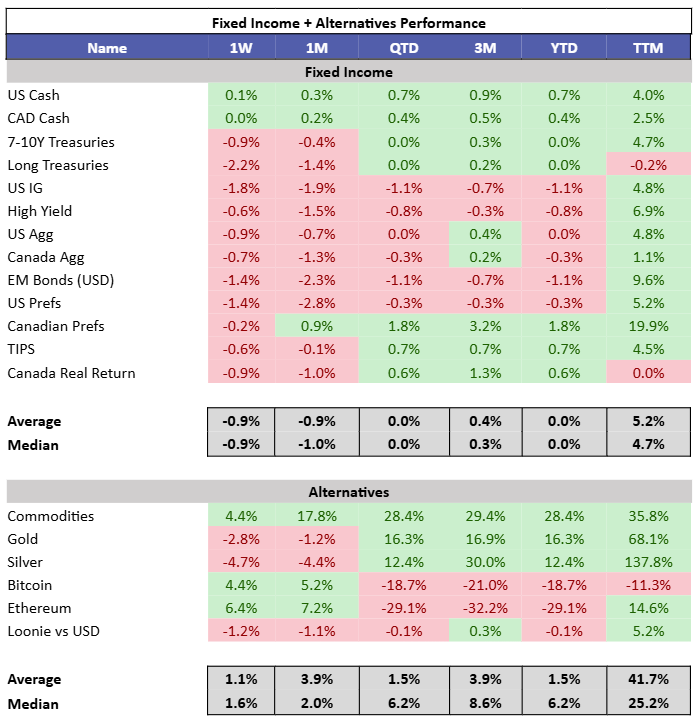

There were very few places to hide last week. Bonds sold off alongside equities. U.S. 10-year yields rose 14 bps while Canadian yields climbed roughly 10 bps. Precious metals pulled back. Crypto, somewhat surprisingly, moved higher. Commodities broadly rallied on the back of Energy.

Unsurprisingly, the disruption to global crude exports has been significant. Roughly a quarter of global exports have been affected. (JPM)

The next concern is duration. Gulf nations may eventually be forced to shut in production if exports remain constrained. JPMorgan estimates that meaningful shut-ins become increasingly likely if the situation remains unresolved over the next two weeks. (JPM)

My initial assumption was that the U.S. would work quickly to prevent this conflict from dragging out. One of the first consequences of sustained higher oil prices is rising inflation, something that is politically toxic heading into midterm elections. (@TKL_Adam)

Households will feel it first at the pump. U.S. gasoline prices are already up 24% over the past two weeks. (Jim Bianco)

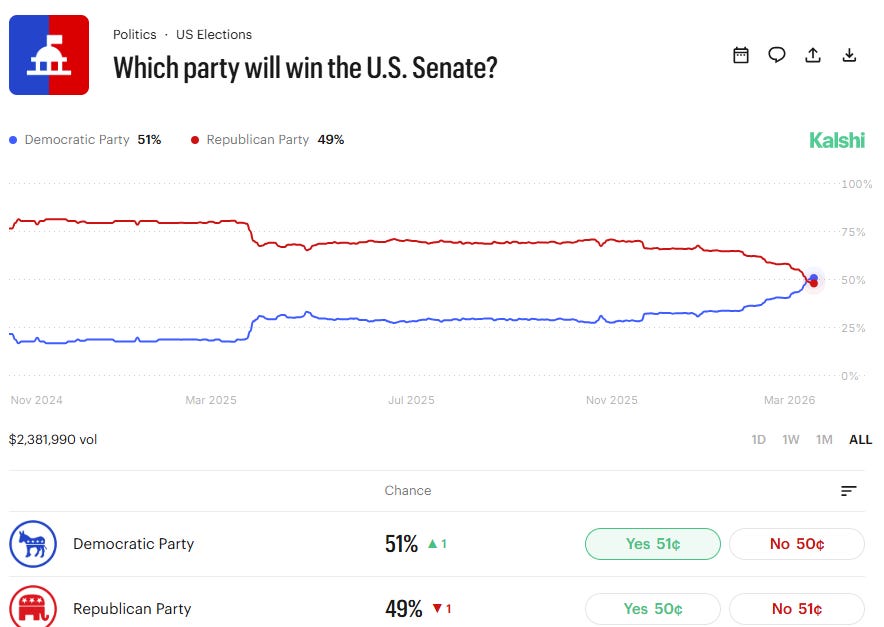

Prediction markets are beginning to reflect the political implications, with odds shifting toward a Democratic Senate. That said, the U.S. economy likely has the greatest capacity to absorb higher oil prices compared with energy importers across Europe and Asia.

In fact, U.S. households are spending near 70-year lows as a share of disposable income on gasoline. That provides some buffer against rising pump prices. (@OilHeadlineNews)

It will also be interesting to see the longer-term implications for the Gulf economies themselves. The UAE and Saudi Arabia were expected to host some of the largest planned data-center buildouts globally. Prolonged instability could complicate those ambitions. (Luke Gromen)

Meanwhile, positioning in oil markets has become extremely crowded. Hedge funds, likely dominated by CTAs, are now the most net long Brent crude futures in five years.(Augur Digest)

And the secondary effects continue to ripple outward. Shipping fuel prices have surged to record highs as maritime routes adjust to the disruption. (Bloomberg)

One interesting historical observation: when crude oil rallies 25% in a week, the average gain for energy equities is only about 4.3%. (Bespoke Investment Group)

The U.S. and much of the Middle East ultimately need this war to end, which makes it hard to chase energy markets here. If the conflict de-escalates, oil likely retraces most of the move. But if it escalates, it raises bigger questions about the U.S.’ ability to contain Iran as American state capacity declines and the nature of warfare evolves. A changing world order.

Michael Every discusses the broader implications in the podcast below.