Oil & Peak Expectations

Markets are rapidly repricing Middle East risk. Implied odds of a U.S. strike on Iran by March 31 have jumped to 61%, roughly double where they stood last week. Oil and gold reacted first. Brent crude is back above $70 as traders front run potential supply disruption. The move suggests risk premium is already being embedded.

Long term oil demand forecasts remain all over the map. Depending on the source, 2050 demand either collapses under electrification or holds steady on emerging market growth. The dispersion tells you less about oil and more about how uncertain the energy transition still is.

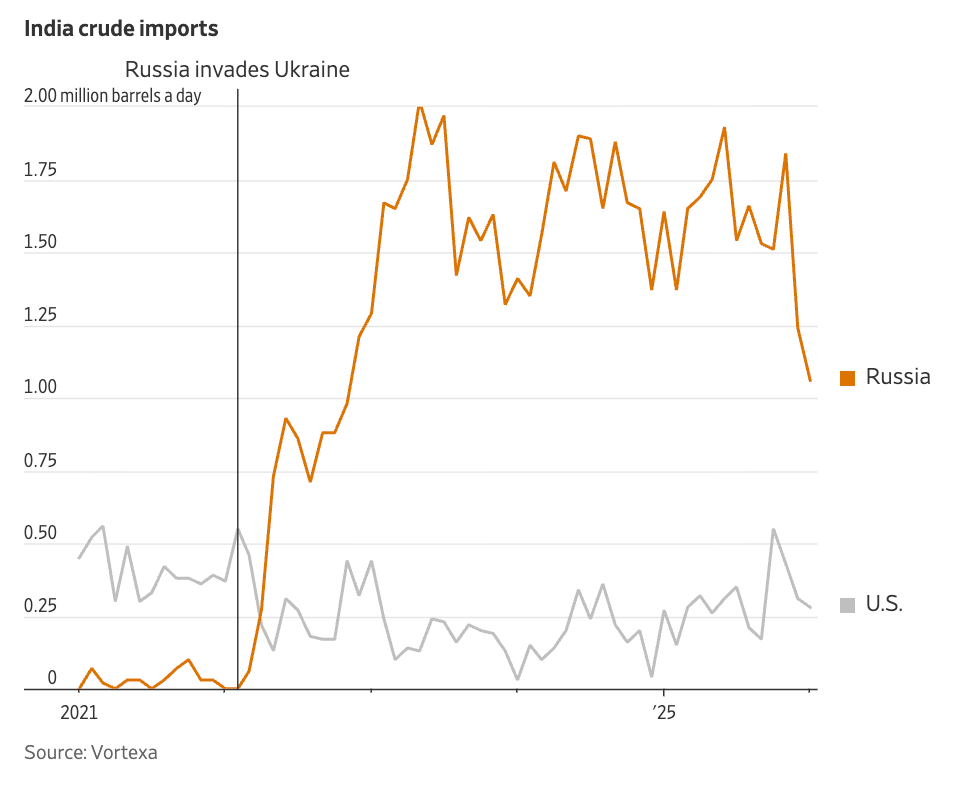

Sanctioned energy flows continue to shift east. India sourced roughly one third of its oil from Russia in early 2025, up from just 2% before 2022. January imports from Russia reached 1.1 million barrels per day versus just 0.3 million from the U.S. The spread between Brent and Russia’s Urals widened to $27.10, highlighting the steep discount Moscow must offer to keep barrels moving. (wsj)

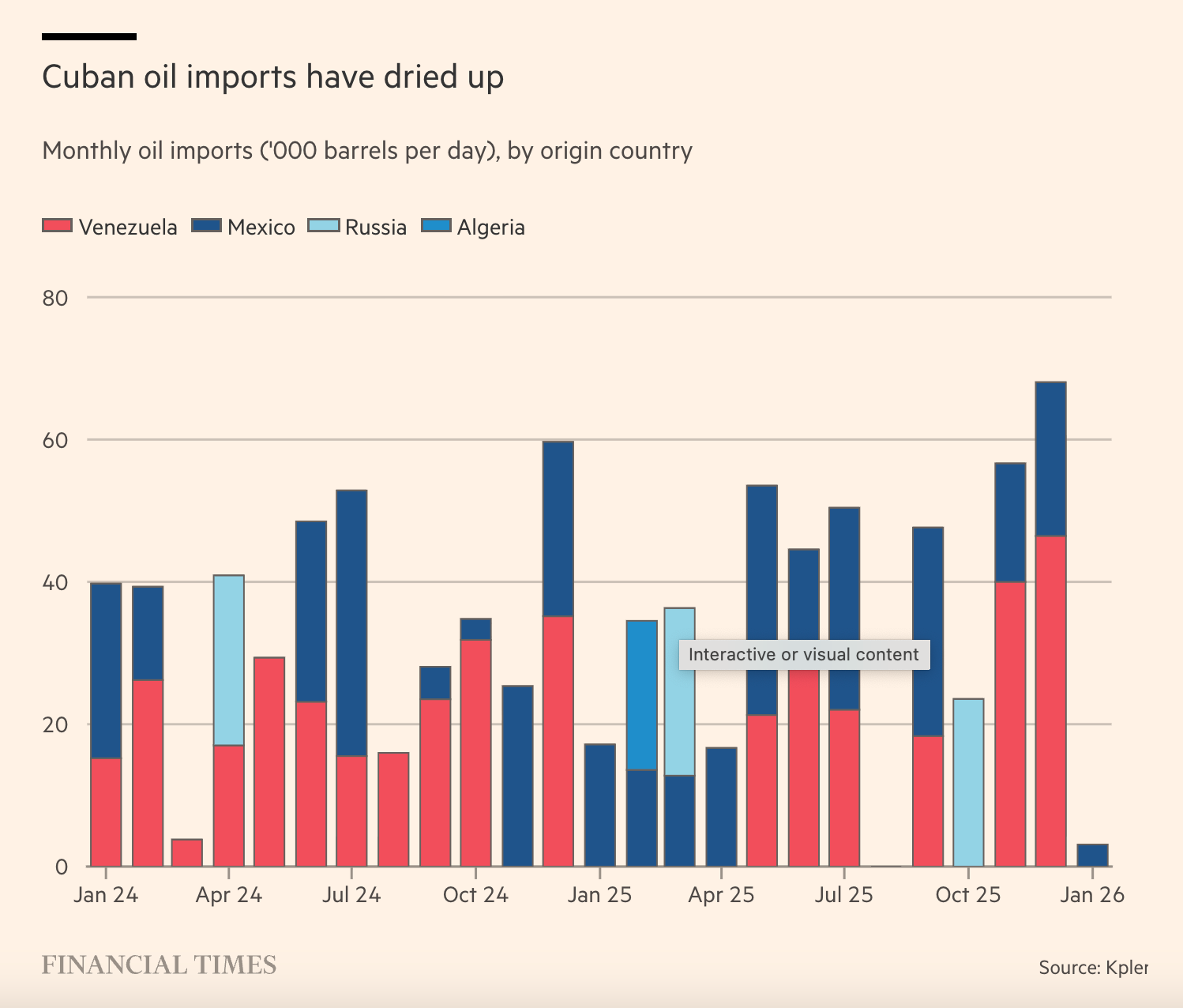

Cuba long relied on Venezuela for subsidized crude. With Caracas under renewed U.S. pressure, flows have slowed and shortages are emerging. Energy dependency is leverage. Cuba could be collateral damage.

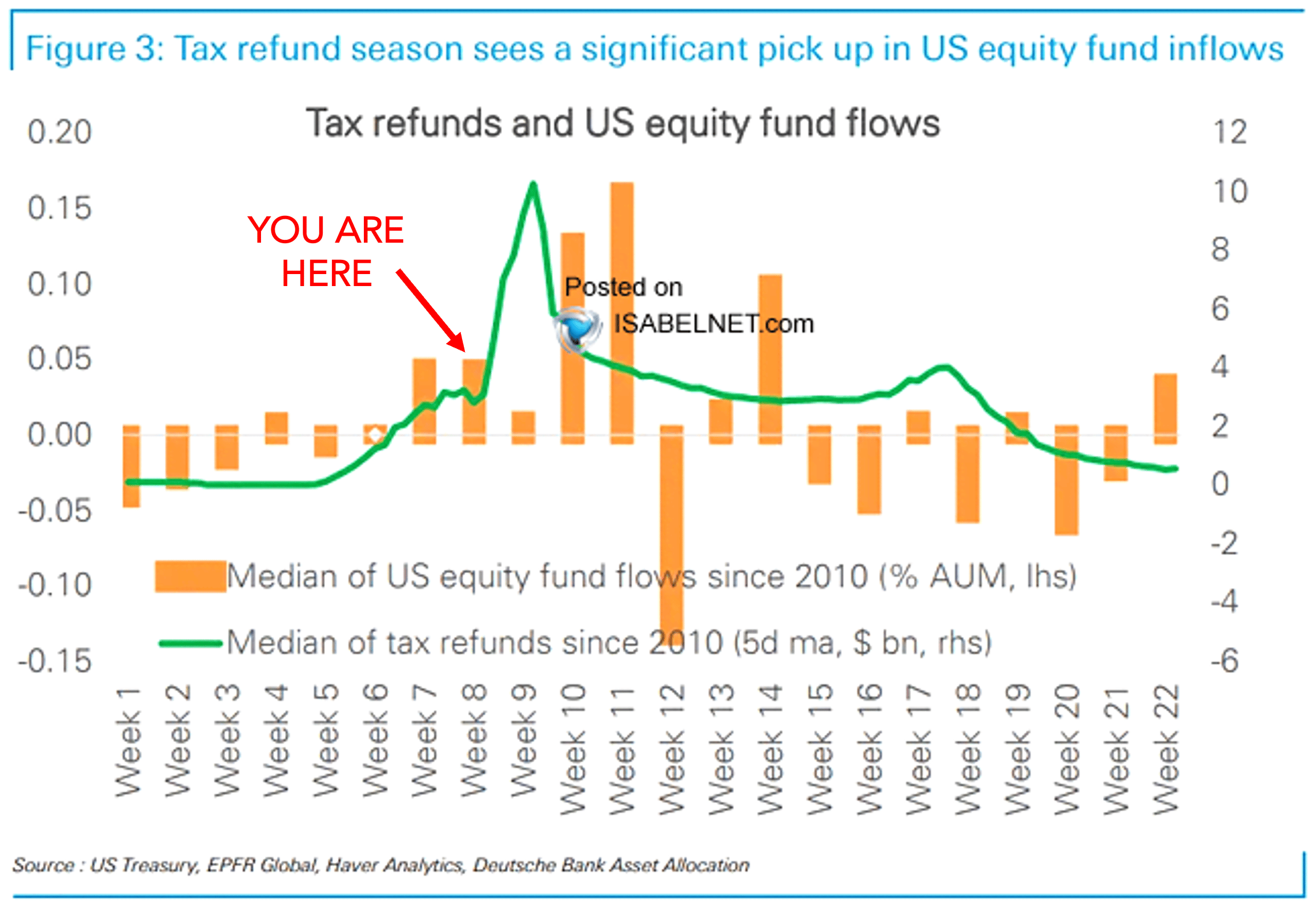

Seasonal liquidity could return. As tax refunds hit bank accounts, some of that capital historically rotates into financial assets. In a momentum driven tape, even marginal flows can amplify speculative behavior. (ISABELNET)

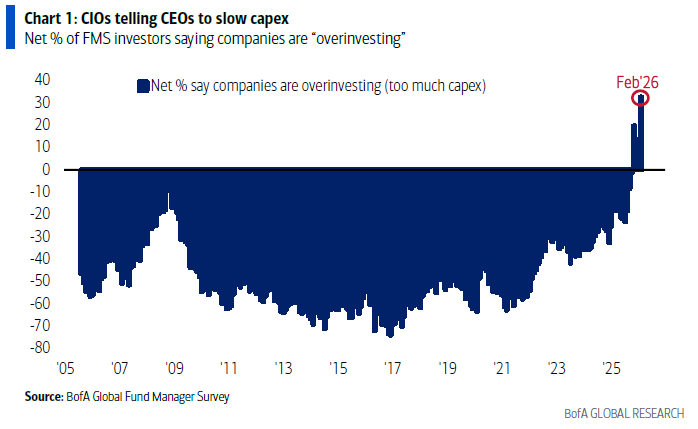

Nearly 40% of the S&P 500 sits in mega cap tech tied to the AI narrative. Yet CIO surveys suggest companies may be over allocating to capex. First markets reward spending. Then they punish excess. If budgets tighten, Nvidia feels it first, followed by the broader AI complex. (BofA)

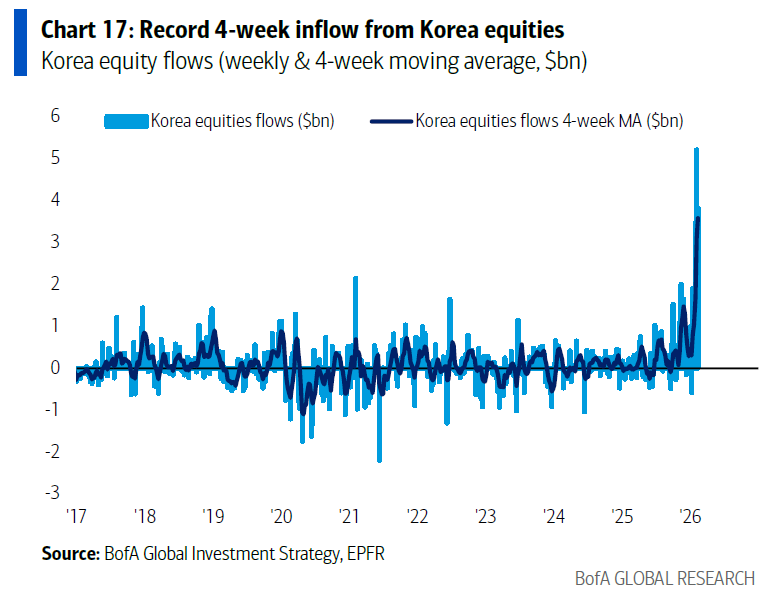

One beneficiary of the AI buildout has been South Korea. Equity inflows have reached record levels as investors position around memory and semiconductors. (BofA)

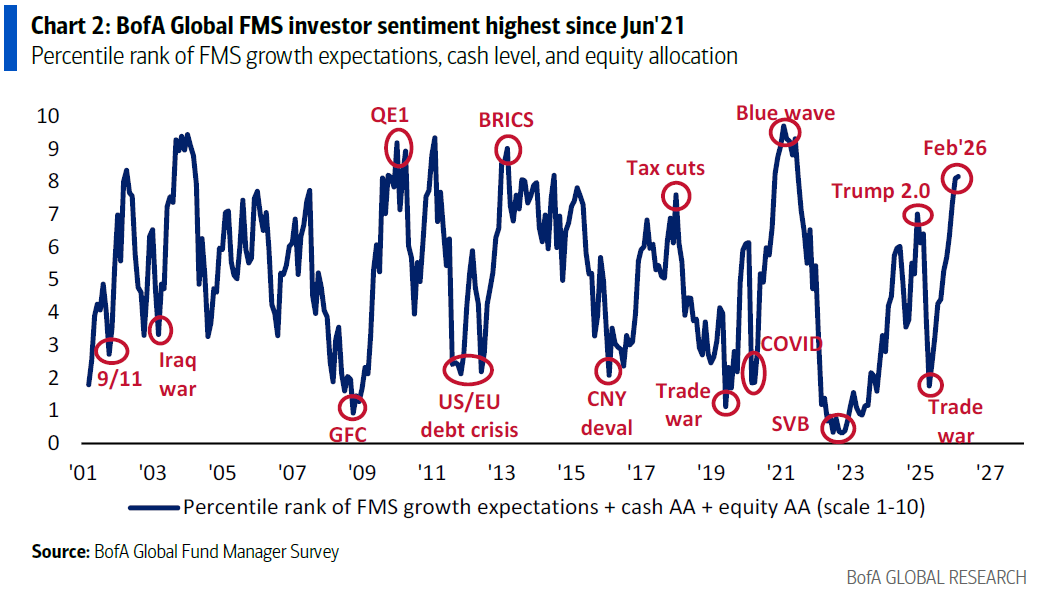

Fund manager sentiment is the most bullish since 2021, according to Bank of America. Positioning has shifted from tariff terror to bull market in a less than a year. If the economy stumbles the market could be vulnerable as investors crowd into risk assets. (BofA)

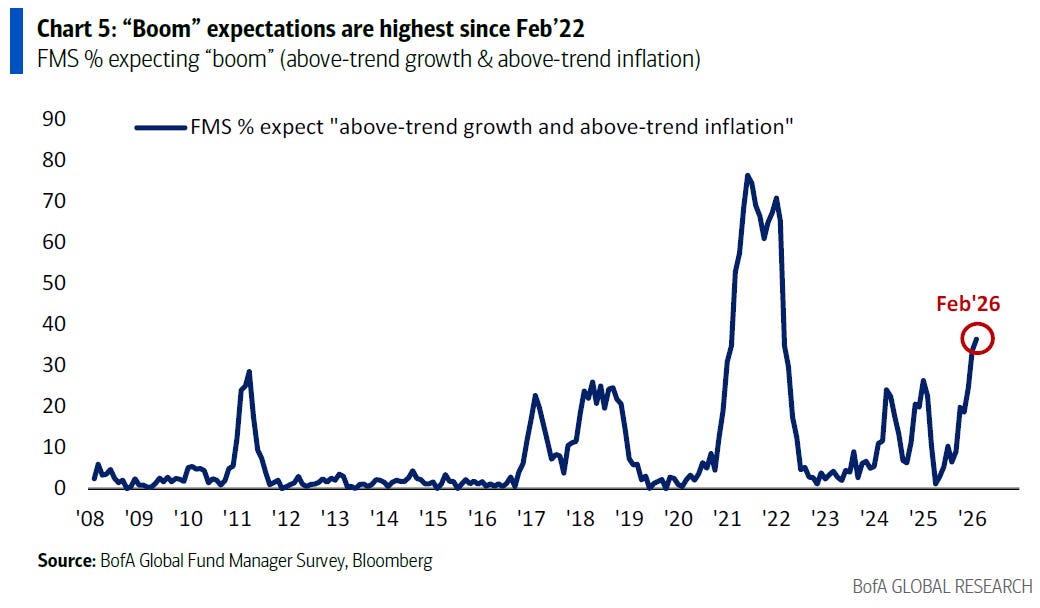

Almost 50% of surveyed investors expect an economic boom. Soft landing has quietly morphed into acceleration. (BofA)

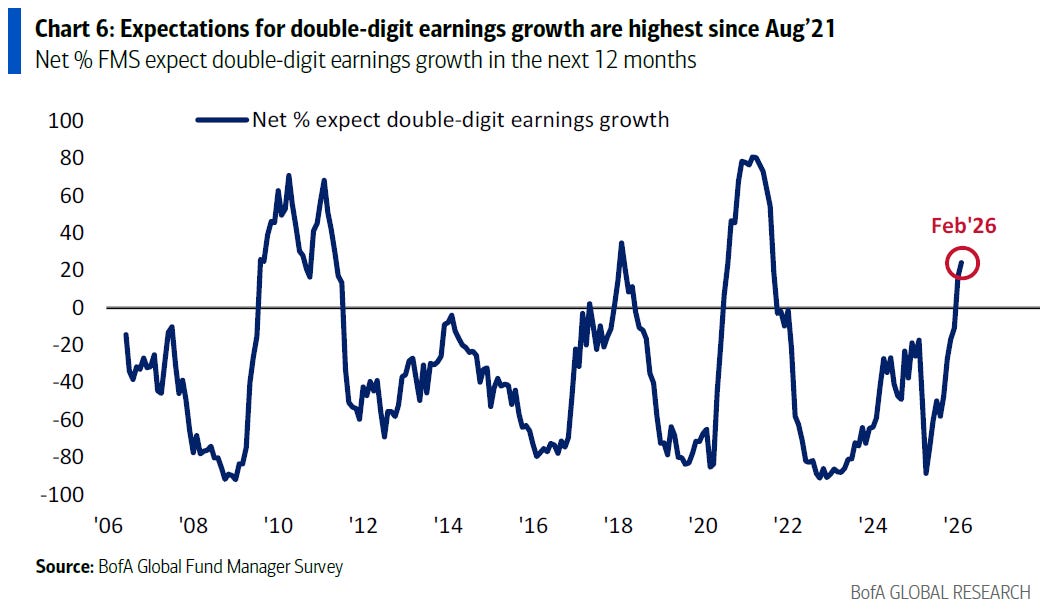

Expectations for double digit earnings growth are at their highest since 2021. (BofA)

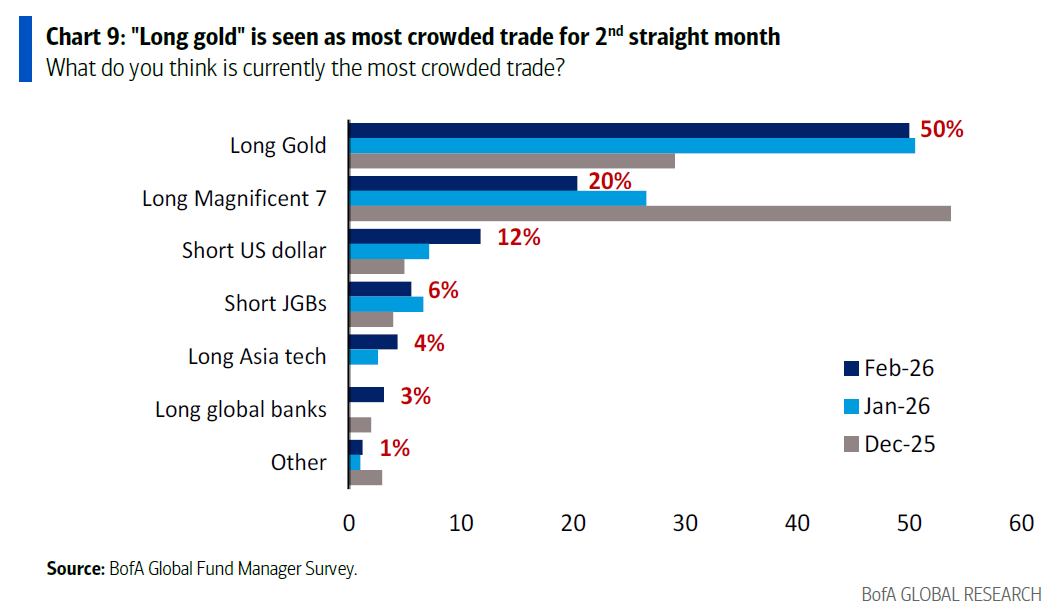

Investors now cite gold as the most crowded trade. It is difficult for equity analysts to underwrite an asset with no cash flows, yet capital keeps moving there. Crowded does not mean wrong, but it does increase vol. (BofA)

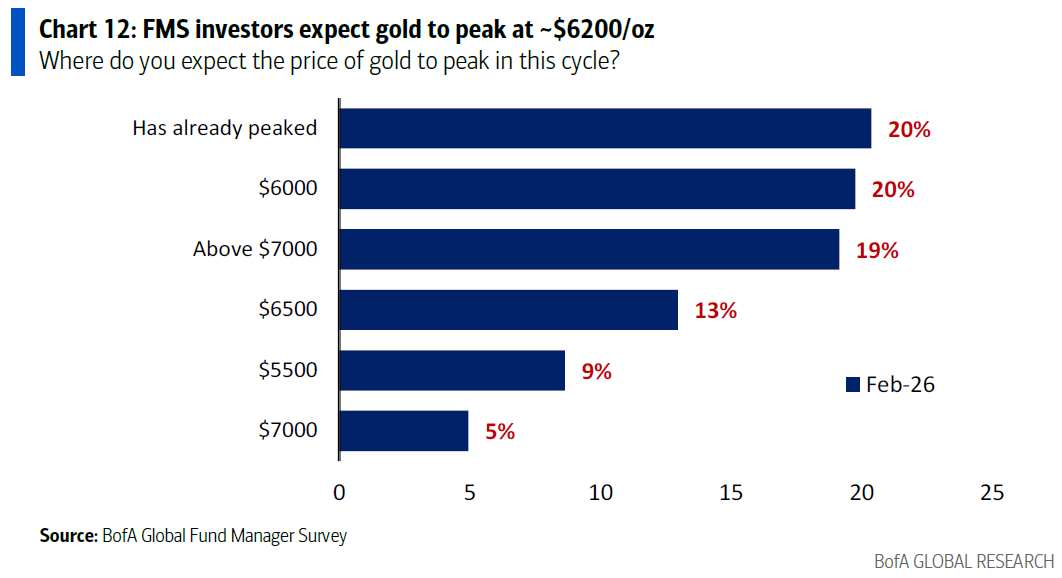

20% of investors think gold has already peaked. Another 19% see it almost doubling to above $7000. Who is right? (BofA)

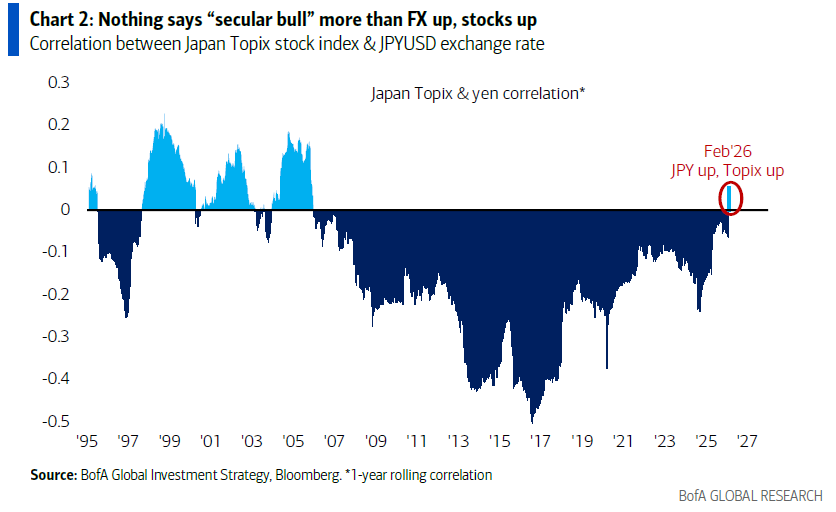

Japan is experiencing a rare combination of rising equities and a strengthening currency. This bullish alignment has not occurred since before the Global Financial Crisis. When capital returns home and markets climb together, it signals renewed confidence in domestic fundamentals. (BofA)