Private Equity in 2026

Catching up on Bain’s Annual Private Equity report to talk about something other than energy and war.

It is strange that the media has fixated on private credit. If there are real credit problems, equity should be getting wiped out first. That is how the capital structure works. The only alternative is sponsor on creditor violence that allow equity investors to survive, or the wider dispersion of outcomes in private equity that gives managers flexibility to take write offs, while the portfolio makes it out ok.

The headlines were effective. Apollo’s private BDC announced 11% redemptions yesterday. The media may or may not be right, but they did create a run.

Based on Bain’s report, private equity looks fine. Not booming, not broken. I’m not rushing to allocate capital to generic managers charging 2 & 20. After capital flooded the space, alpha to compensate for high fees is scarcer than it once was. Like everything in investing, you need to find the pockets of inefficiency.

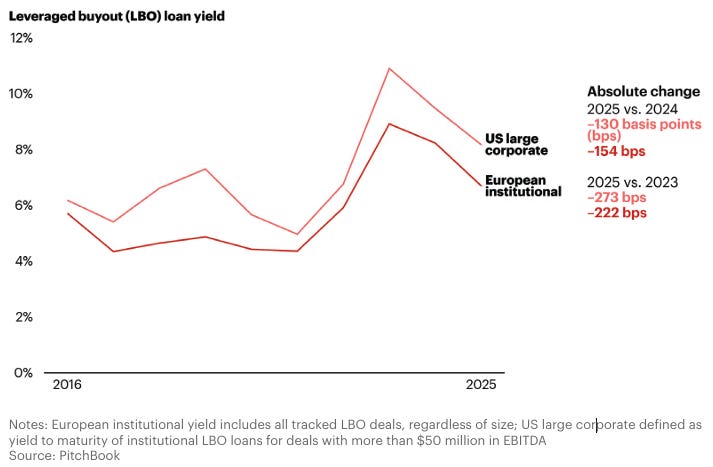

Leveraged loan markets seem to be identifying the real pressure point. Software. If you are an LP in a software focused PE fund like Vista or Thoma Bravo, you might be sweating. Still, most of the stress is tied to AI disruption speculation rather than deteriorating fundamentals. A lot can change.

Still, if there is a downturn, it is likely slow motion. Most portfolio companies are still going concerns. Losses will probably come through disappointing returns as multiples revert to reality rather than a blow up.

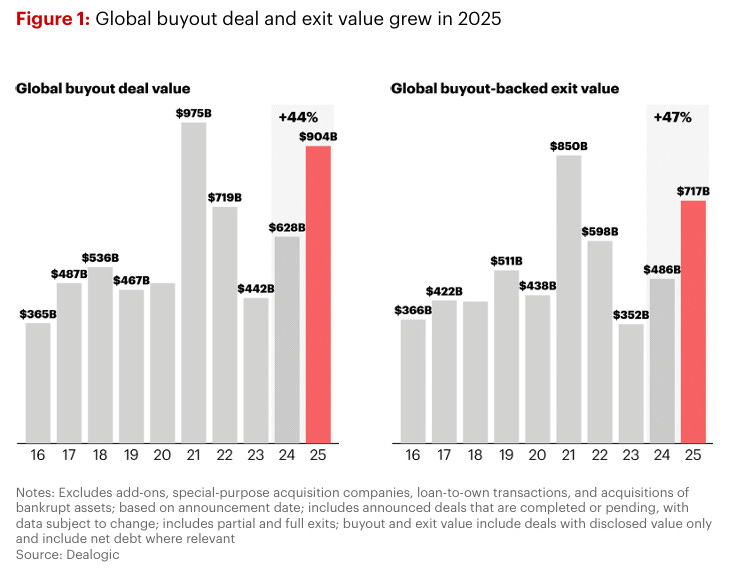

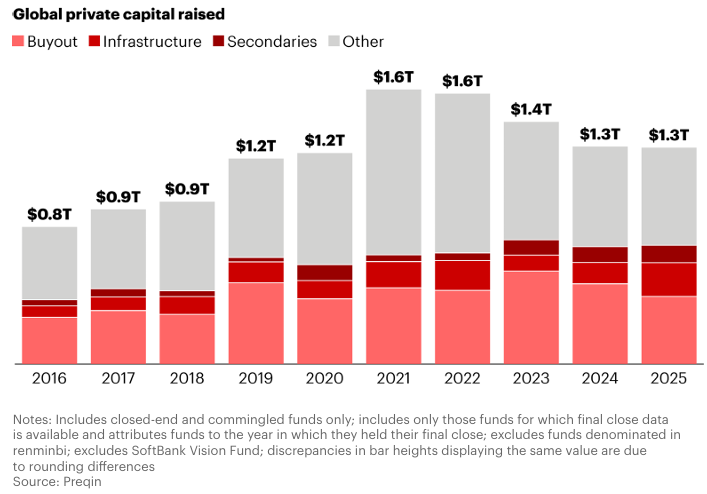

Deal value rose 44% in 2025. Exit value increased 47%.

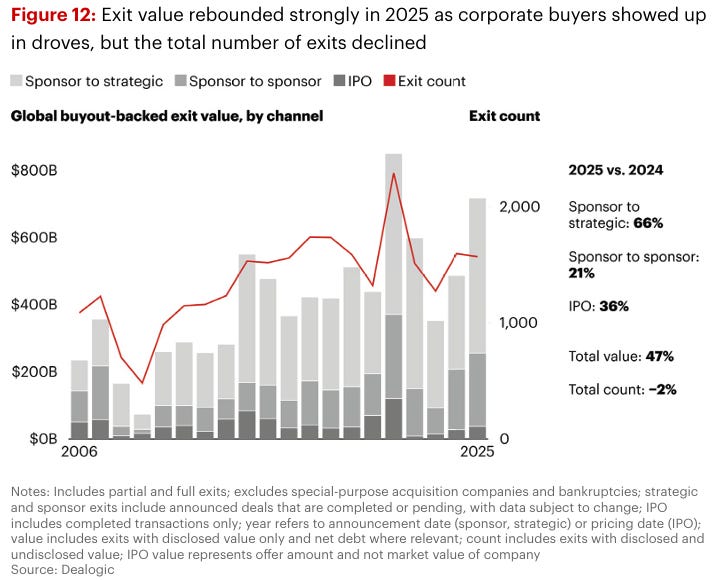

Exit mix looks historically normal. Sponsor to sponsor deals remain elevated versus pre 2020 levels.

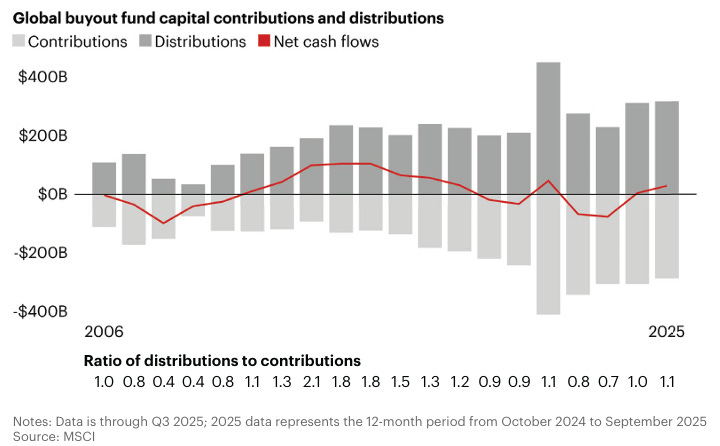

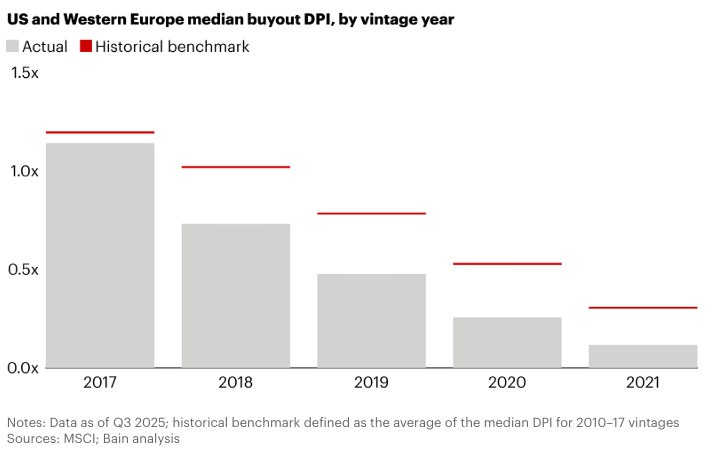

The real issue remains exits. There is now $4 trillion of unrealized private equity value. Over $1.5 trillion of that is more than five years old and looking for liquidity.

Cash flow dynamics matter. When investors receive more distributions than they deploy, capital gets recycled. That is not happening.

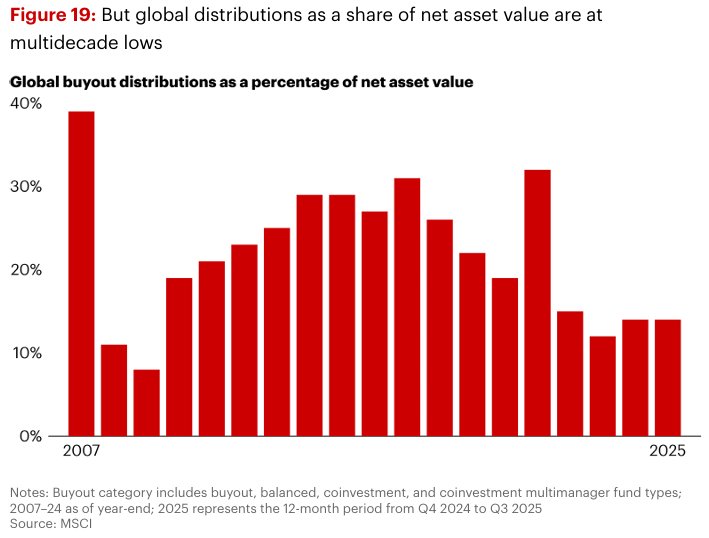

Distributions relative to total assets are roughly one third of peak 2010s levels.

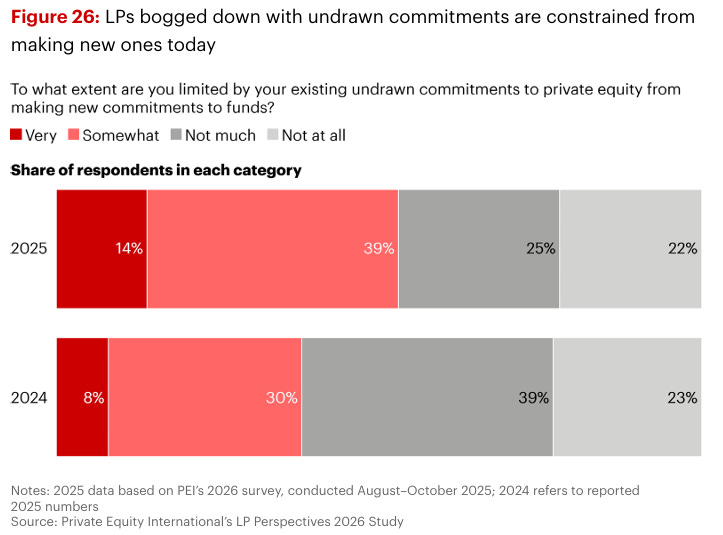

Investors overcommitted and now feel stuck with undrawn commitments.

No matter how you measure it, distributions remain below historical averages.

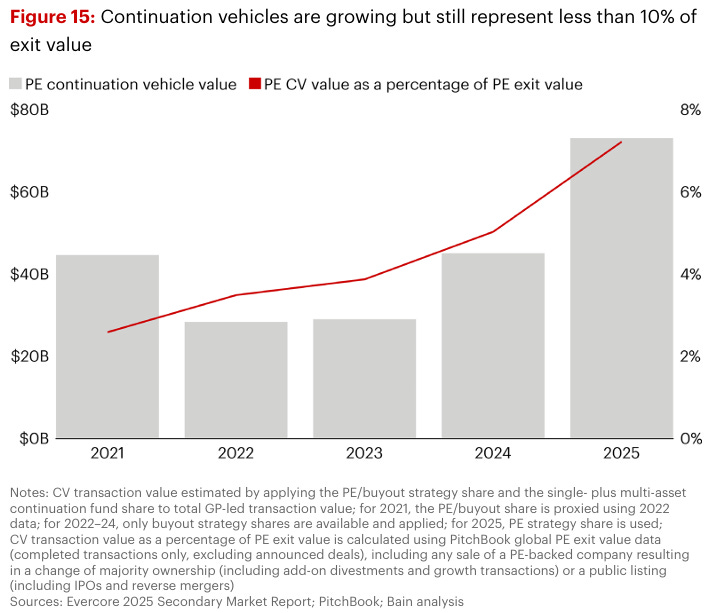

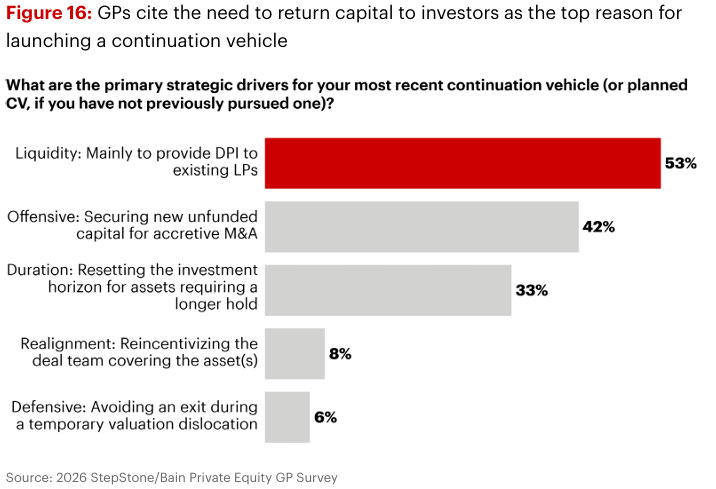

GPs are increasingly turning to continuation vehicles. Usage has doubled over the past five years.

These structures are meant to return capital, but investors should be getting paid a premium for providing liquidity. It is not clear that is happening.

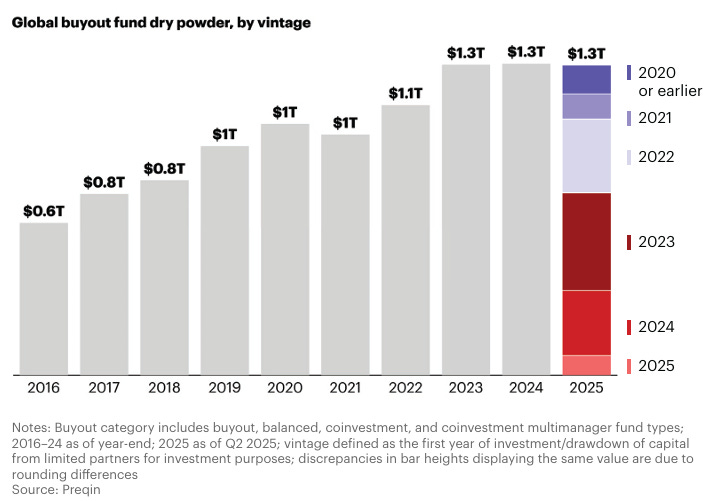

Dry powder remains near record levels. Deployment tends to lag fundraising, so capital will still be put to work even if fundraising slows.

Buyout fundraising has declined from recent highs but looks average over the past decade.

Before the energy shock, falling rates were expected to provide relief. That support may now be in question.

As usual the narrative has overshot the problem. I don’t like PC, but the lockups are a feature not a bug. In 2008, hedge funds were supposed to be liquid and when THEY gated it was a sign of crisis. The things they invested into suddenly were not liquid, including funds and securities held at Lehman. PC learned that lesson and recognized the risk-so gating was provided for intended to be used from the start, to address the fact their book is illiquid. This protects long term investors from hot money causing a fire sale situation in the fund. The issue is that these were sold to the wrong people, that didn’t understand that those gates were likely to be employed like they are now. Down the road they might be grateful after this passes, as these funds might be the only thing NOT liquidated at a discount when (if) the stock market loses 50%.