Private Equity's Waiting Game

On Wednesday, Kevin Warsh takes the hot seat for his first Fed day as chair. History is not on his side. Since 1994, when the central bank began announcing policy decisions on the day of the meeting, the S&P 500 has never managed an up day during a new chair’s debut (@bespokeinvest)

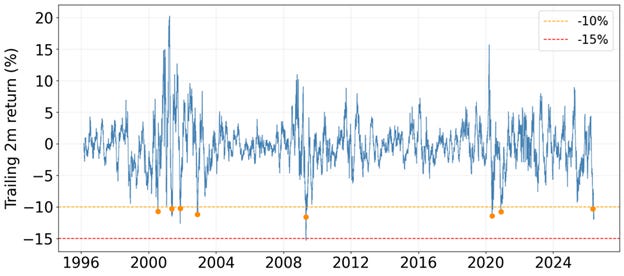

The low-volatility factor is experiencing an incredibly rare collapse. This level of underperformance sits in the 0.5th percentile of trailing two-month windows since 1996, making it about as extreme as historical data gets. Historically, this massive outperformance of high-beta over low-volatility stocks concentrates in just two distinct environments: aggressive risk-on rebounds off a market bottom, or late-cycle junk rallies leading into a blow-off top. (Verdad)

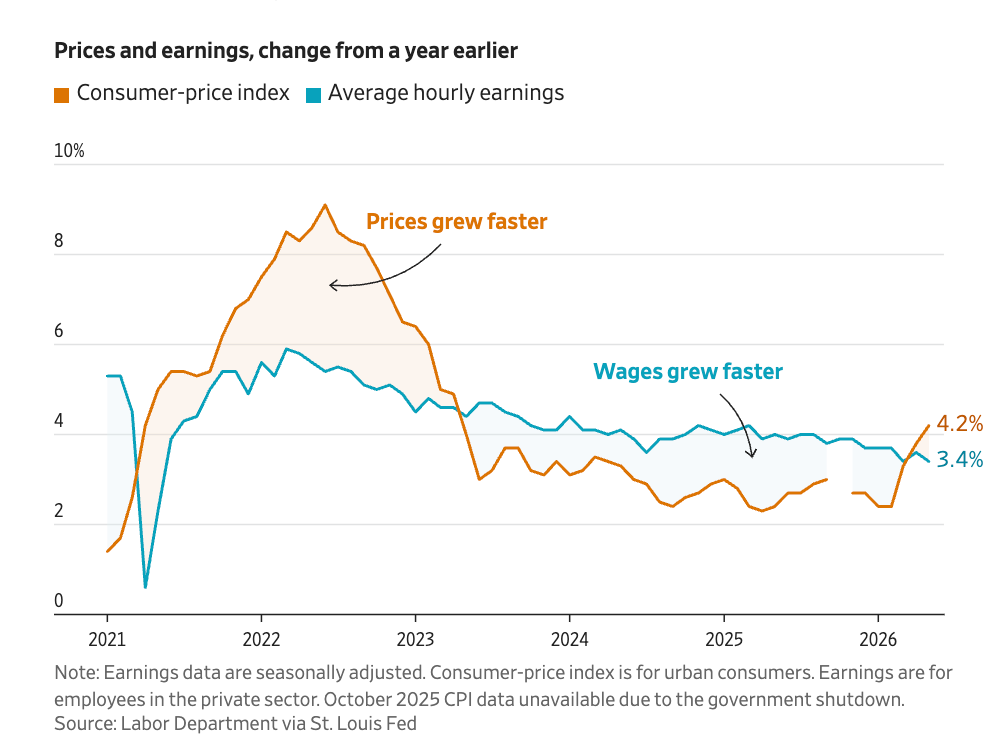

With last week's inflation report, prices are now growing faster than wages in the U.S. for the first time since 2023. (wsj)

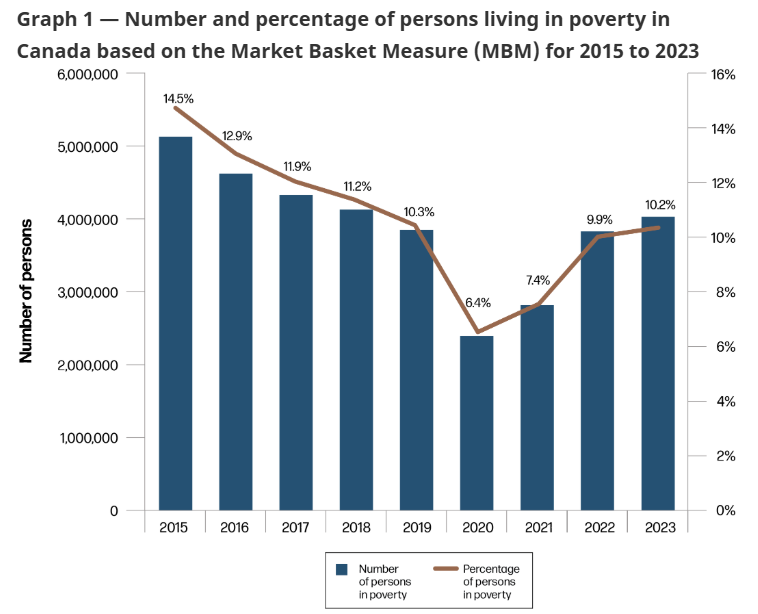

On a similar note, recent data out of Canada perfectly encapsulates the environment above. Poverty has consistently risen since 2020. Unlike past cycles where job losses drove poverty, this current trend is strictly a cost of living crisis where wages simply cannot keep pace with expenses. The report points to housing costs as the main culprit, though there is finally some relief on that front as rents begin to fall. (Gov Canada)

Looking at the 3-month GLD put skew versus call skew, investors are showing a massive preference for downside protection over upside optionality. I didn’t realize the market is surprisingly bearish on gold right now.

Check out our latest episode, where we discuss the most important headlines across markets in the past week.

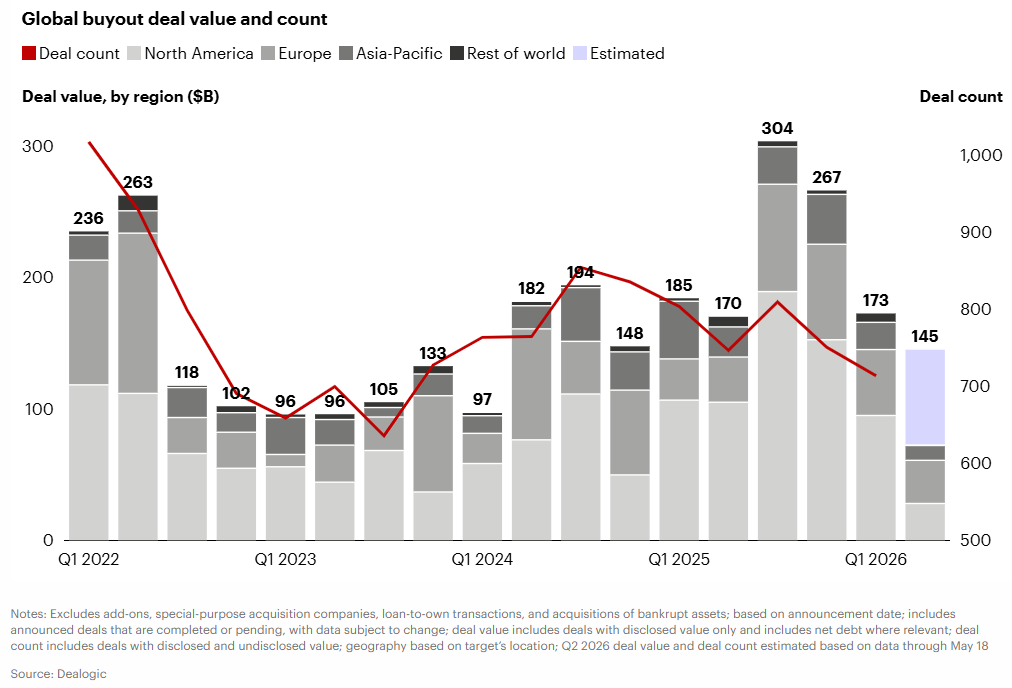

Private Equity deal count and value are projected to return toward post-covid lows, reversing the spike seen in the second half of 2025. Data suggests we are returning to a "wait-and-see" environment, where marks are held steady and portfolio companies are staying on the sidelines. (Bain)

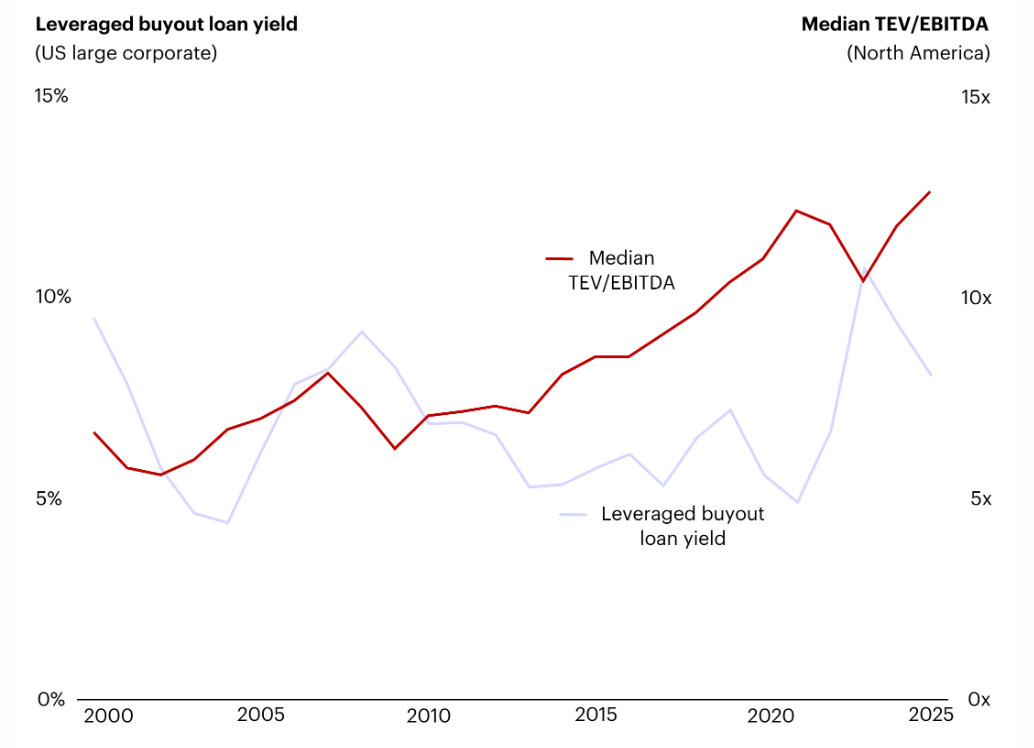

Deal valuations and financing costs remain elevated, keeping the broader market expensive. (Bain)

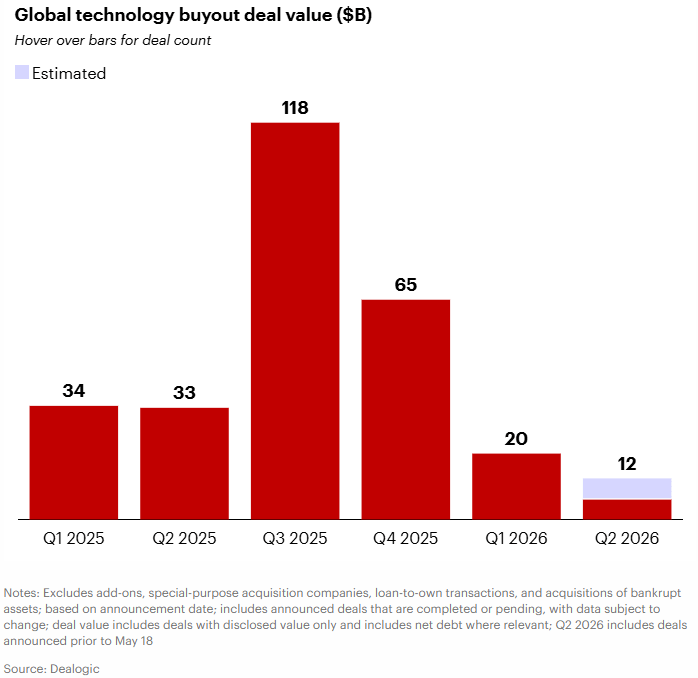

Part of this decline stems from a visible slowdown in private equity investments across the technology sector. (Bain)

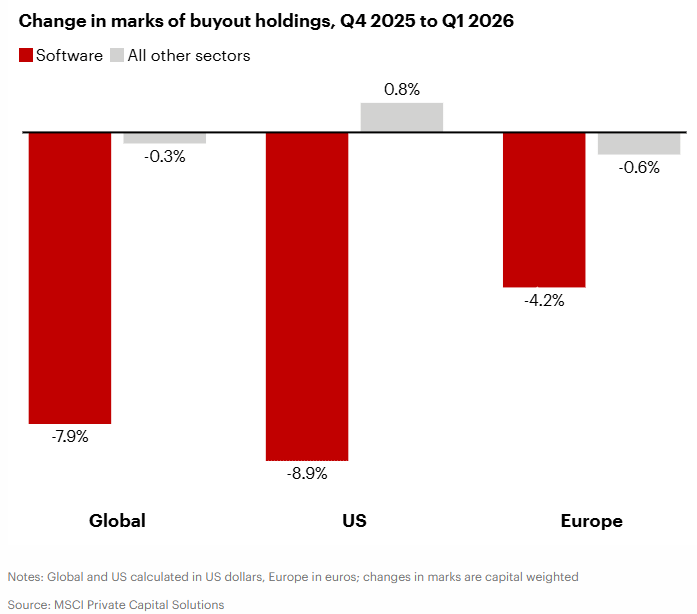

Consequently, private equity firms marked down their software holdings in Q1 of this year. This correction still looks somewhat disconnected from the public software market, which tends to be higher-quality businesses, and the public BDC market, which continues to trade at a discount of more than 20% to NAV. (Bain)

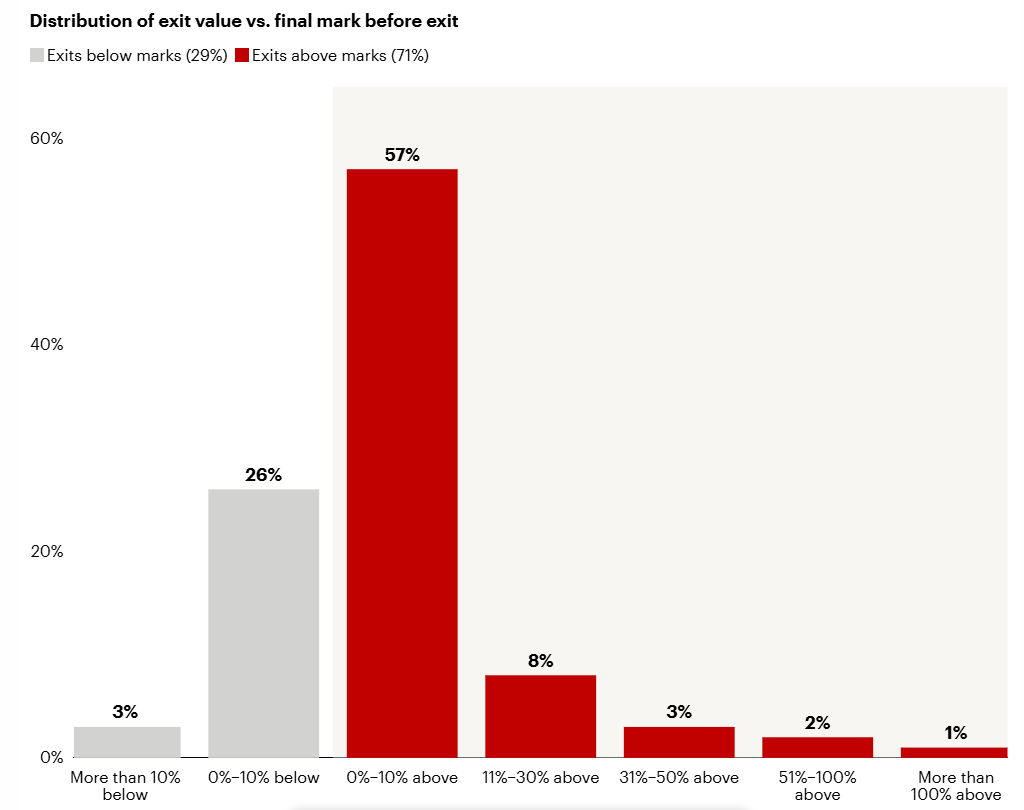

Despite the markdowns, private equity investors are definitely not panicking. 71% of exits are still transacting at prices above their current marks. (Bain)

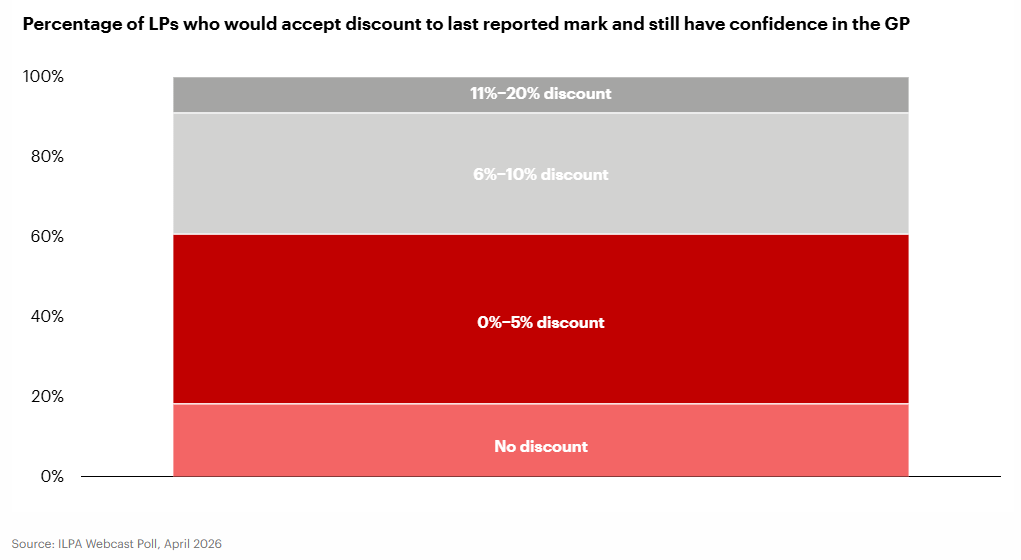

Furthermore, the majority of LPs remain unwilling to accept a discount of more than 5% to execute a secondary transaction. (Bain)

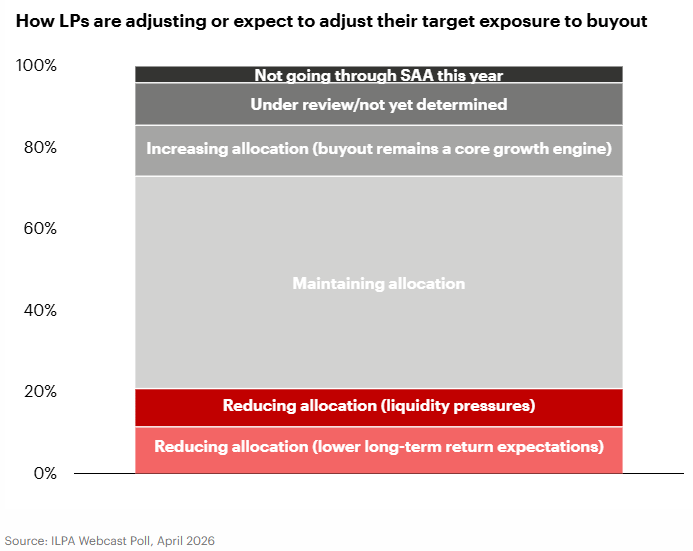

And institutional investors are not materially cutting allocations to the asset class yet. (Bain)