Record Earnings. Rising Risks.

Interesting discussion with Tobi from Shopify. Talks about AI and a wide range of topics. When he talks about the AI use at Shopify, it’s clear to me, AI will accelerate some software companies. He had some interesting things to say about Canada. He argues that Canada is making a deliberate “choice” not to be the richest country on Earth, despite possessing all the natural resources needed for the next two decades. He critiques the national habit of “overfitting to niceness,” which he believes leads to “unkind lies” about the true state of the economy and contributes to a “Trump derangement syndrome” that causes Canadians to view the U.S. as a greater threat than Russia or China. Lütke highlights a historical failure to evolve past a “beaver pelt” mentality, where Canada exports raw materials and buys back finished goods and expresses frustration with an academic and social culture that he believes increasingly prioritizes “intersectionality fever dreams” over merit. Ultimately, he maintains that the only winning strategy for Canada’s prosperity is to “win by helping America win,” rather than distancing itself from its largest economic partner.

Episode 3. One question remains after this recording: will oil shortages and higher prices impact earnings or lead to inflation and higher rates, ultimately reducing equity market multiples? Alternatively, is the global economy resilient enough that markets are right to ignore these risks?

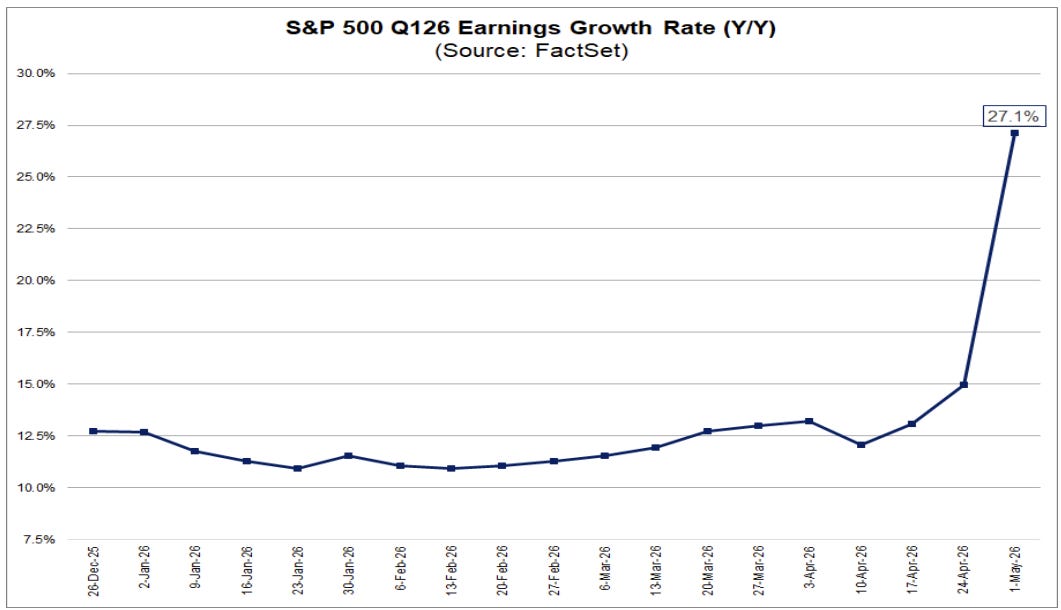

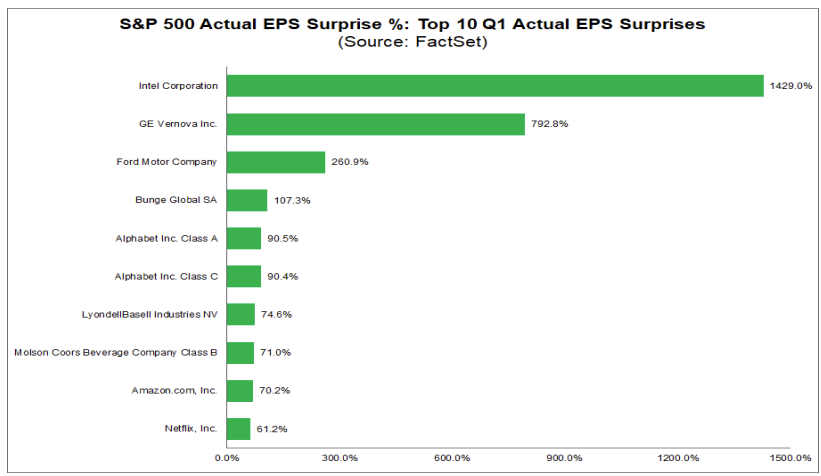

Two thirds of the S&P 500 have now reported and this is shaping up to be a quarter to remember. As recently as mid April, expectations called for solid but not spectacular growth of ~12.5%. In just two weeks, that number has surged to over 27% YoY. That is a massive revision, especially against a macro backdrop that still feels far more fragile.

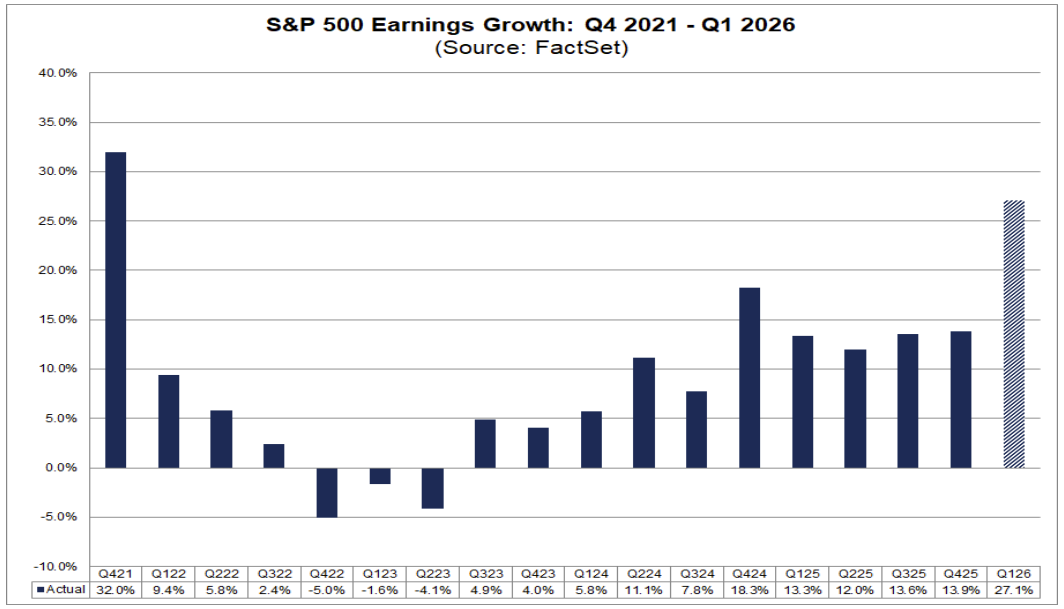

At 27%, this would mark the strongest earnings quarter since Q4 2021, coming out of the COVID reopening surge. The headline is powerful. The composition matters more.

A meaningful portion of that growth is being flattered by non-operating income. Two companies alone reported over $50B tied to non-marketable securities, largely driven by ownership stakes in Anthropic. Strip that out and the picture is still strong, but less extraordinary.

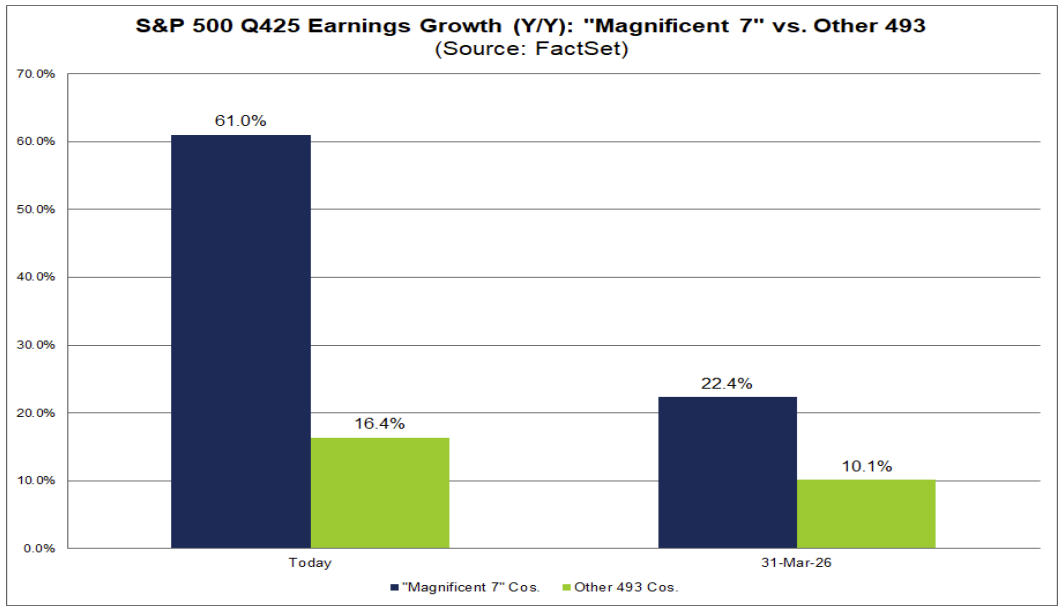

This was also a miss for the “markets are efficient” crowd. Analysts had penciled in ~22% growth for the Magnificent 7 just a month ago. The reality is closer to 61%. Even more telling, they underestimated the rest of the market as well. The scale of the revision speaks to how quickly the earnings engine is being repriced.

Unsurprisingly, most of the upside came from the AI complex. That continues to be the center of gravity for both earnings and market leadership. Tech, at least for now, is delivering near flawless results.

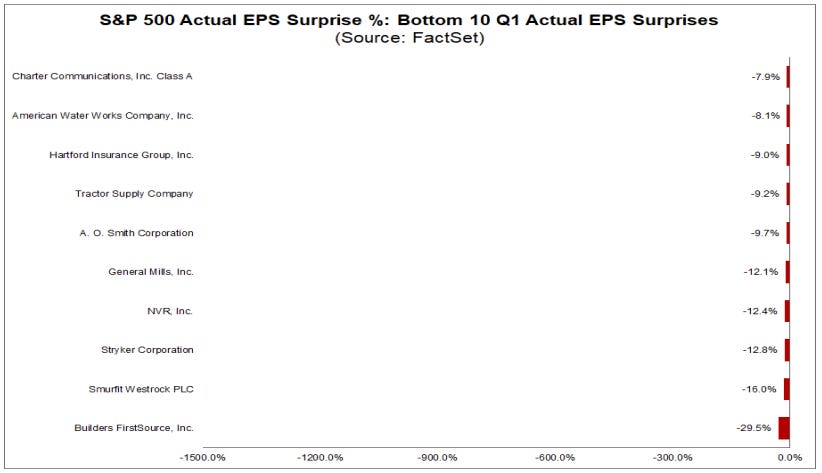

Outside of that, the story is less clean. The “boring middle” of the economy is showed a bit of weakness.

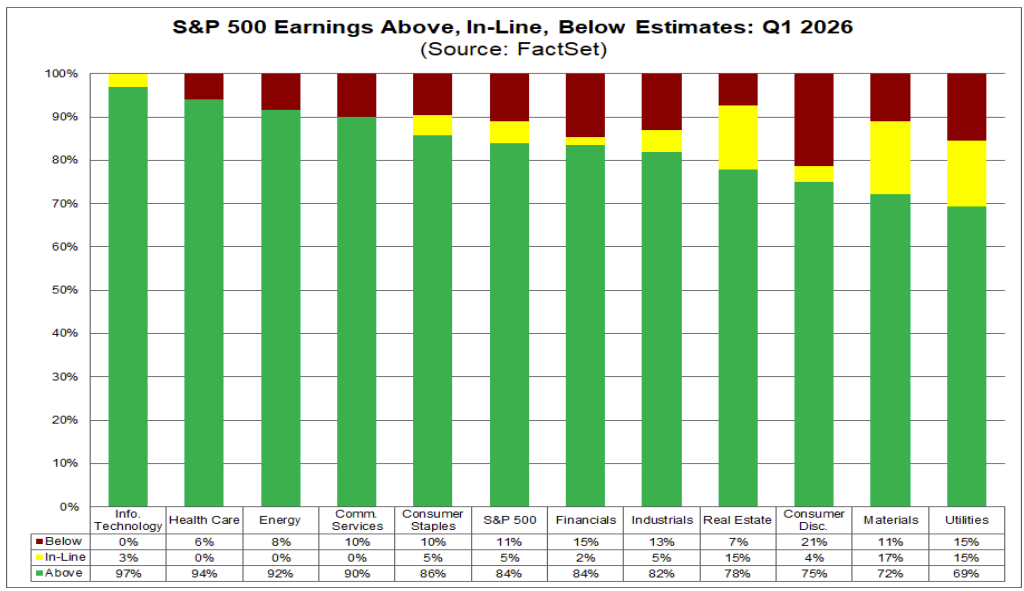

Tech has shown flawless earnings.

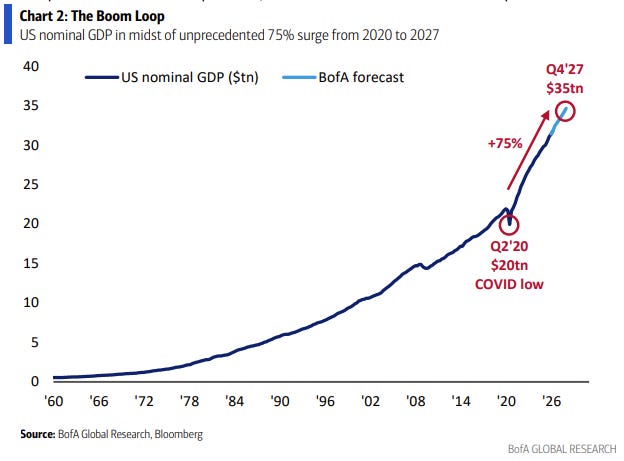

Part of the strength is nominal. The economy has simply gotten bigger. Bank of America estimates GDP will have grown 75% from COVID lows in under seven years. That tailwind is real and it is lifting earnings across sectors.

Geopolitics is starting to creep back into the tape. Europe has sold off in recent weeks as energy security concerns resurface amid Middle East tensions.

Asia looks the most exposed to higher gasoline prices since February. The transmission is uneven, and the move in North America has been surprisingly sharp. Anyone know why gas oline prices have risen more here than in Europe?

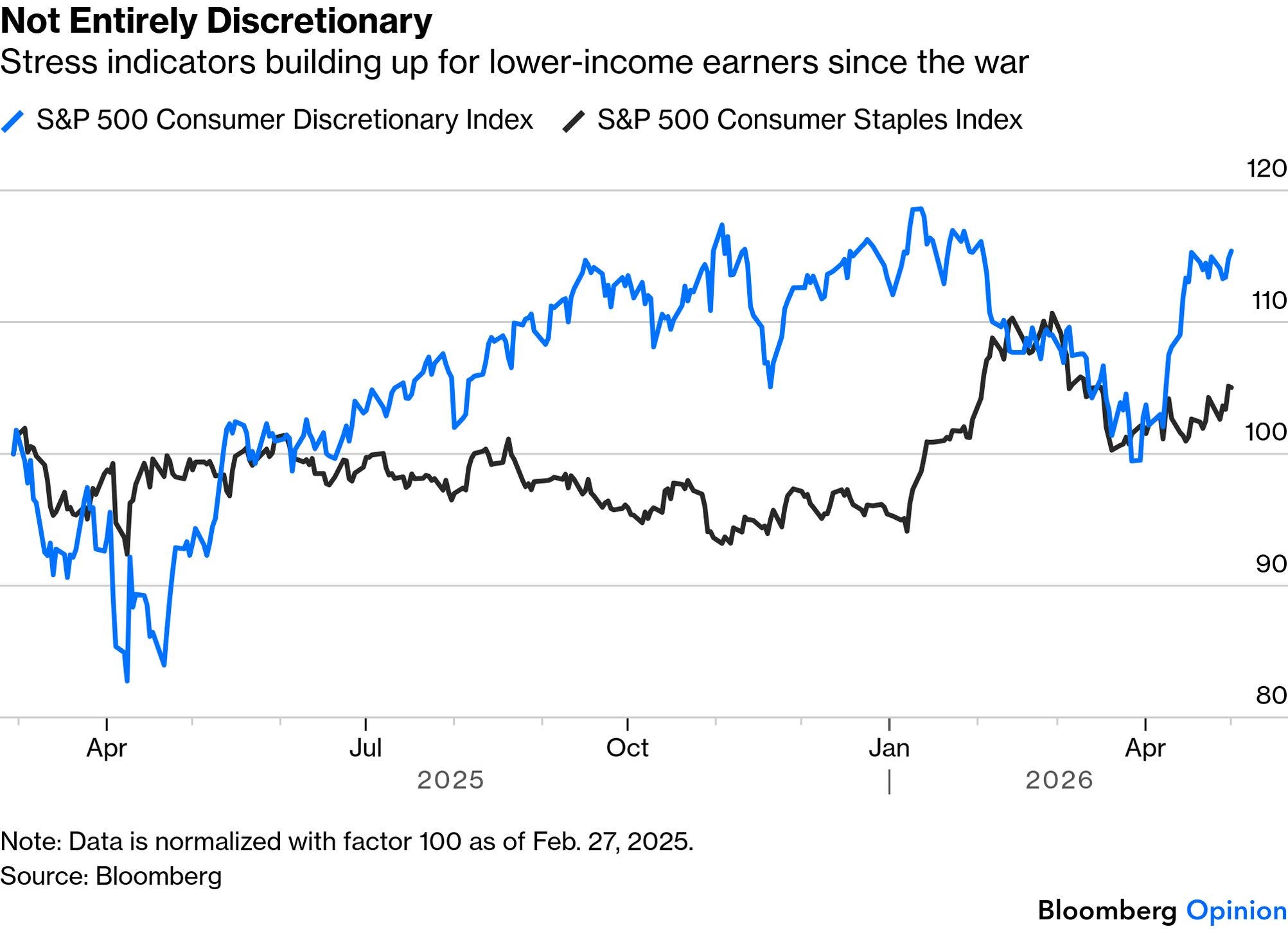

The second order effect is already visible. Higher energy prices hit lower income consumers harder. That widens the gap between the top and the bottom of the economy. Another data point reinforcing the K shaped recovery. Consumer Staples lagging Consumer Discretionary.