Priced for Growth

Strange data out of China. BYD sales are collapsing. Capacity utilization has fallen below 50% and sales are down 41% YoY. That is not noise. (@alojoh)

As flagged last week, Consumer Staples are trading more expensively than the Mag 7. The nuance is cash flow. The Mag 7 are deep in an investment cycle, and the market is starting to question the return profile of that capex. Still interesting. (@MikeZaccardi)

Over the past 30 days, the S&P 500 is down 1.4%, yet the average stock has moved 10% in absolute terms. The index looks calm. Underneath, it is anything but. (@BarbarianCap)

Consensus is still calling for double-digit earnings growth. That optimism is already priced in. With the S&P 500 flat on the year and the Nasdaq down, there is little room for disappointment. (@MikeZaccardi)

The next two weeks are seasonally strong for the S&P 500. (@neilksethi)

European wholesale gas prices jumped more than 20% today. In historical context it is a blip, and still below January levels. Pricing implies the market expects a short conflict. Summer contracts remain far cheaper. Warmer weather is a relief valve.(@DanielKral1)

Historically, geopolitical conflicts have had limited lasting impact on the S&P 500. Markets discount duration, not headlines. (BCA)

This is a granular look at the data but includes some non geopolitical events.

Investors are punishing U.S. sectors most exposed to AI-driven automation. The market is betting that vulnerable business models will struggle to adapt, even if current fundamentals remain stable. (ISABELNET)

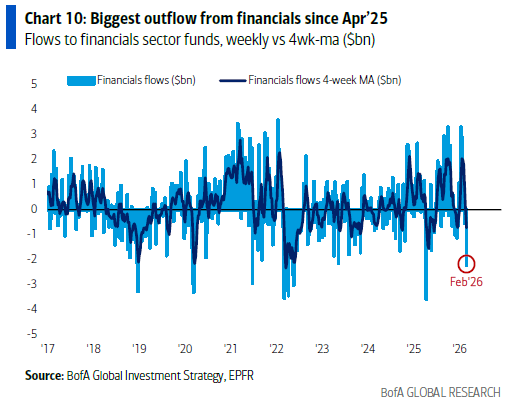

Financials were hit last week amid renewed scrutiny of the Private Credit complex. Contagion fears are resurfacing. (BofA)

The average tenure of companies in the S&P 500 keeps falling. Creative destruction is accelerating. AI will likely compress that cycle further. (Apollo)

Despite the noise, fears of a broad rotation out of U.S. equities have not materialized. Capital is rotating within, not necessarily leaving. (Apollo)

Stan Druckenmiller’s positioning:

Long Korea, Japan, and Brazil

Long copper on AI demand and tight supply

Long gold on geopolitics

Short bonds

The portfolio is no longer AI beta. He is bearish on the dollar but constructive on U.S. growth with disinflation.

He also admits to puking weekly from stress during drawdowns.