Semis In, Software Out

Out with the old, in with the new. According to Goldman Sachs’ hedge fund net exposure data, the rotation is official: software is out, and semiconductors are firmly in.

The shift away from software carries heavy implications for private credit. Approximately 16% of loans across major Business Development Companies (BDCs) are tied to software firms. The risk here is structural; these loans are collateralized against cash flows rather than hard assets. If these business models face disruption, recovery values could be negligible. I will say, the fears of the software apocalypse seem a bit overdone. (@pvtcreditguy)

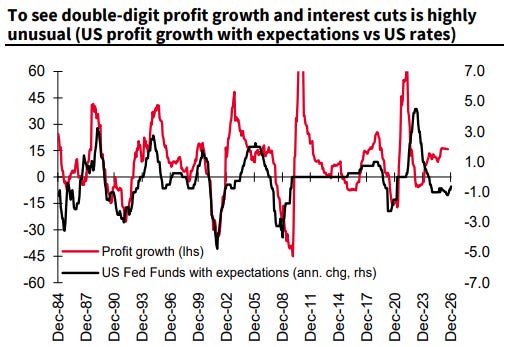

As the market digests Kevin Warsh’s nomination, all eyes are on the Federal Reserve’s next move. We are navigating a "K-shaped" economy where corporate profits are expanding even as the market clamors for rate cuts. However, while the wealthy remain resilient, the struggling low-end consumer sees little relief from lower rates, suggesting that current policy may be targeting the wrong side of the divide. (SocGen)

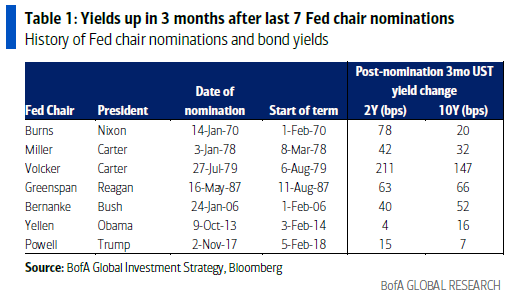

The appointment of a new Fed Chair is typically a headwind for bond markets, often acting as a catalyst for rising yields. (BofA)

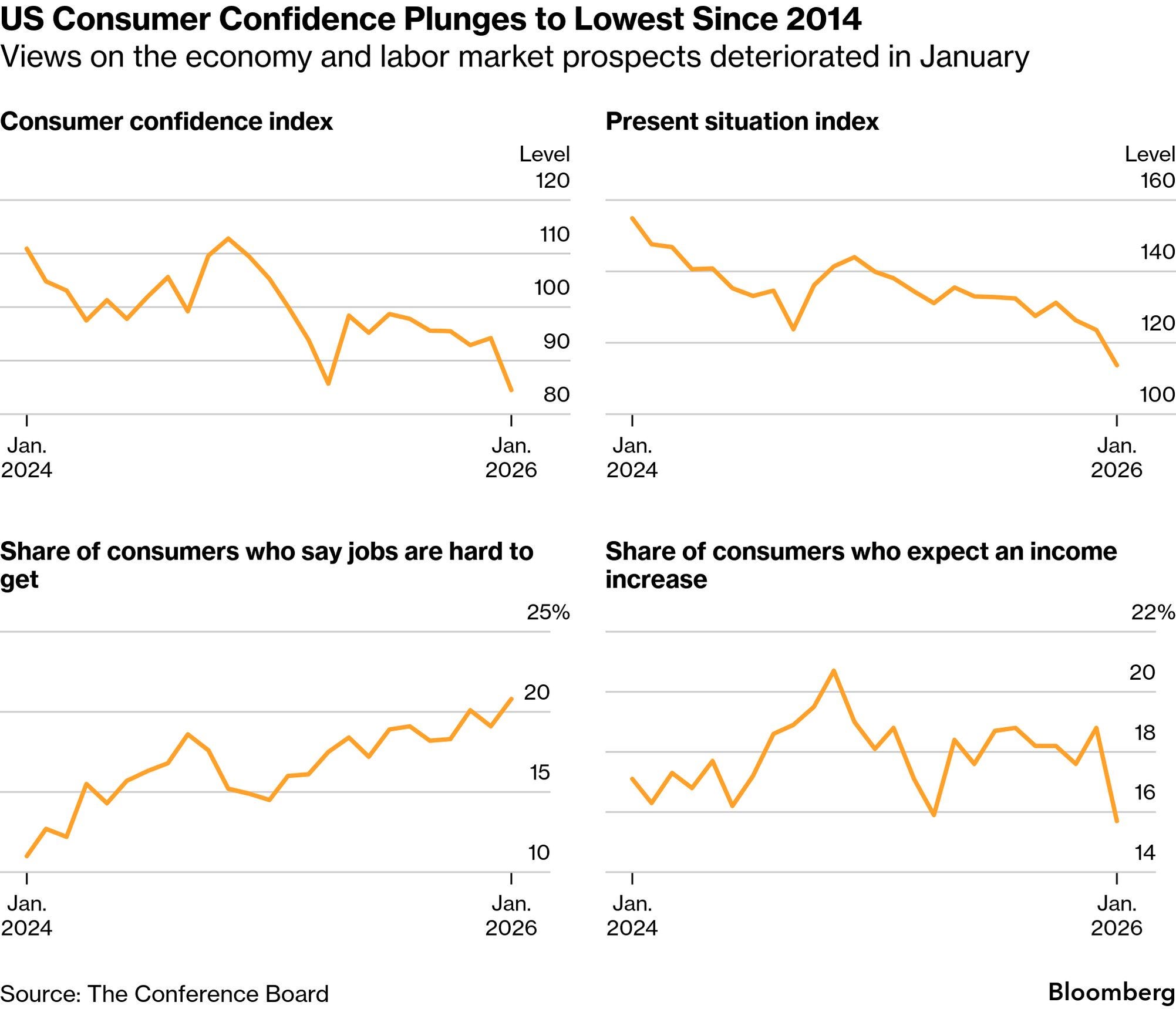

Despite decent macro data, consumer sentiment indicators remain in the doldrums. This persistent gloom may be more reflective of a polarized political climate than actual economic health. (Bloomberg)

ISM US Manufacturing Tops Expectations Activity surged to 52.6 (vs. 48.6 expected), marking the fastest expansion in four years. This unexpected jump signals a significant rebound in industrial momentum.

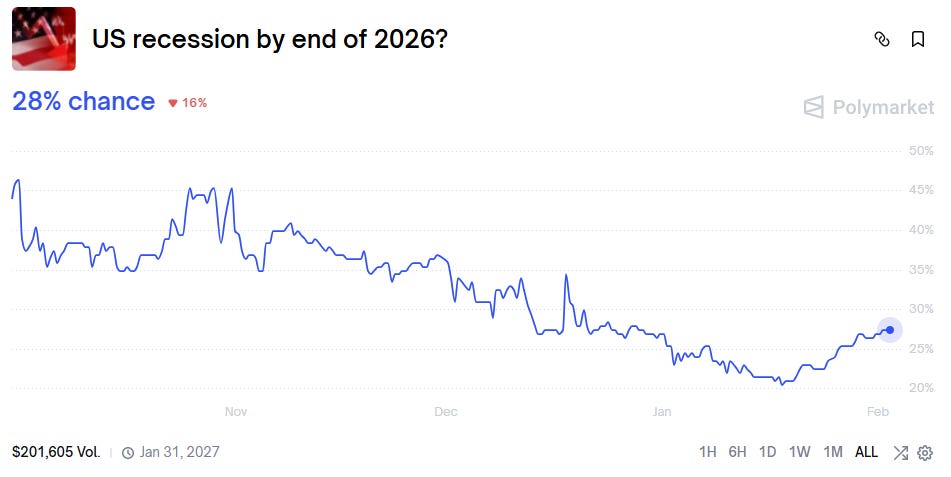

Polymarket 2026 recession odds had ground down to 20% since Q4 of last year but recently began rising.

Fund manager recession expectations are now at the lows. (BofA)

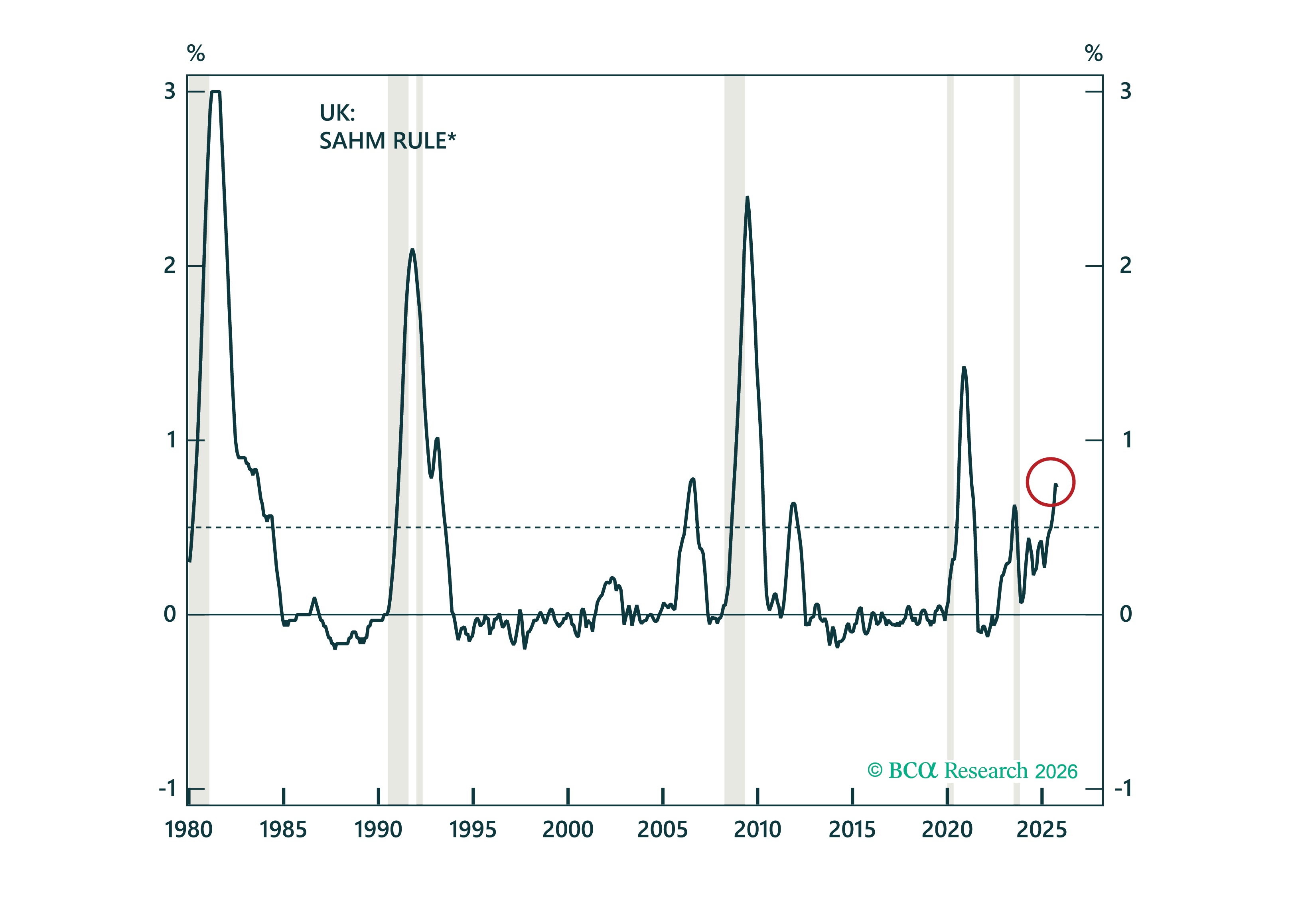

The US continues to show relative strength compared to its peers. While the domestic outlook remains stable, the UK is grappling with a fresh acceleration in unemployment. (BCA)

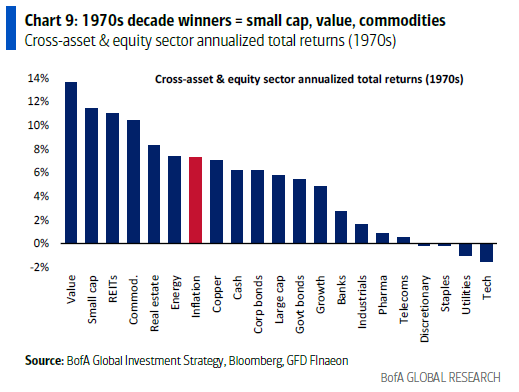

If we see a sustained reacceleration of inflation, the 1970s provide the definitive playbook. During that decade, Value stocks, Real Estate, and Commodities were the undisputed champions. (BofA)

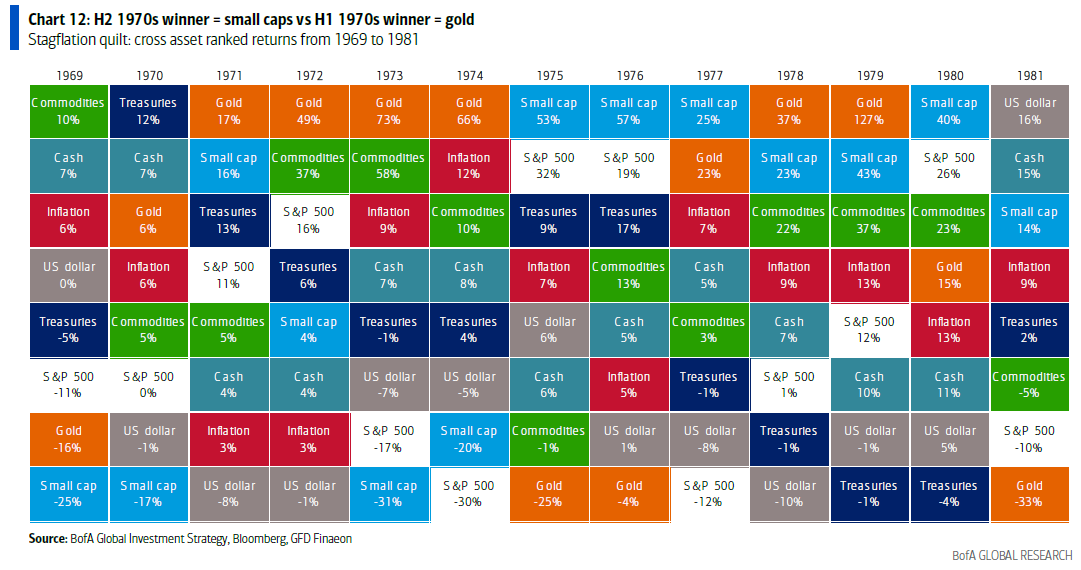

And this is asset class performance in the 70s broken out by year. (BofA)

Musk once again is making headlines, he says he will merge xAI with SpaceX.

Good podcast. The thing that stood out to me. “From a macro perspective you just need to get a few big things right” For him that big thing is no bonds due to financial repression.