Sentiment Turning Cautious

Concerns the US economy has peaked due to policy uncertainty undermining confidence and stalling investment. Government job cuts having a significant multiplier effect from consultants, while private spending in DC is frozen. Microsoft has been the first to signal a peak in AI capital expenditures, and a new coronavirus development emerged on Friday all contributing to a rough week for equity markets.

Walmart Inc., the first major big-box retailer to announce holiday results, fell 6.5%. Its CFO noted uncertainties regarding consumer behavior and global economic and geopolitical conditions.

Speculative tech was hit the hardest.

US 10Y yields down 4 bps on the week, the 10Y was unchanged in Canada; mixed week for fixed income. Precious metals continued to rally and crypto struggled.

Interesting data point. Since Trump's second inauguration, the US has ranked as the worst-performing G7 equity market and is one of the few down during this period. China has been the top performing.

xAI released their latest model last week, despite the late start, they have caught up to the competition. However, the first cracks in the AI bull market thesis are forming after Satya Nadella appeared on a podcast last week. Gavin Baker (VC) had a post breaking down the news, takeaways below:

Early Lead Narrowing: OpenAI’s initial dominance, gained from aggressively scaling pre-training since summer 2022, has diminished as competitors like Google, Anthropic, and xAI have caught up, with the first-mover advantage in reasoning proving only temporary.

Data as the Differentiator: Future competitive advantage hinges on access to unique, valuable data. Companies like Google, xAI, and potentially Meta are positioned to leverage their proprietary data sources, suggesting that models without such access could quickly depreciate.

Strategic Shifts in Investment and Infrastructure: Reflecting these dynamics, leaders like Satya Nadella are shifting strategies—opting out of massive pre-training investments in favor of cost-effective inference services—and signaling a future where a few players dominate frontier models and infrastructure becomes more specialized for low-latency, cost-effective inference.

TD claims that Microsoft is paying penalties to exit certain data center contracts and power agreements, indicating a significant shift in its stance on CAPEX growth. Here is a post explaining why investors could be overreacting to the surface level bad news.

Hedge Funds de-risked Tech exposure aggressively during last week’s sell off. The de-grossing over the past 2 weeks was the largest since July and ranks in the top 4 “risk off” events in the past 5 years.

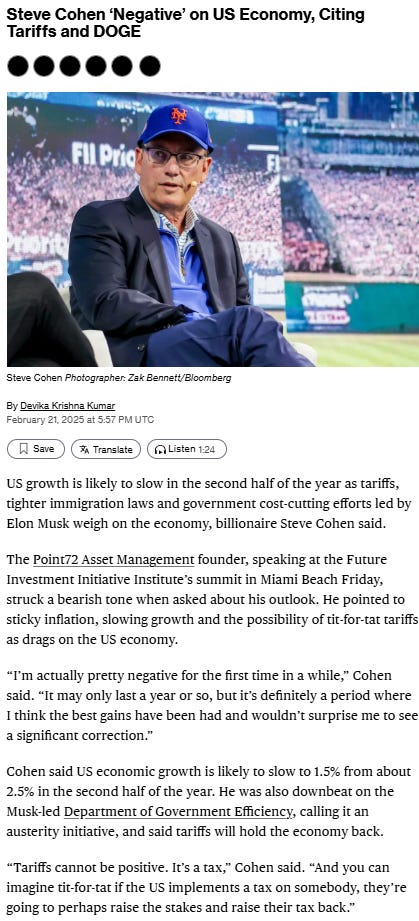

Steve Cohen and other investors starting to realize that Trump’s plans might be negative for the US economy and market.

S&P 500 forward earnings estimates have fallen to their lowest point since early 2023, although they still indicate approximately 13% year-over-year growth for 2025.

Market is still very expensive and vulnerable to negative news. S&P 500 free cash flow yield is at its lowest level over the past 20 years.

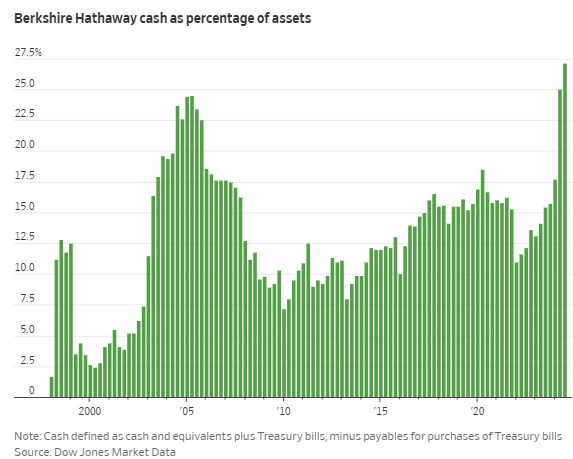

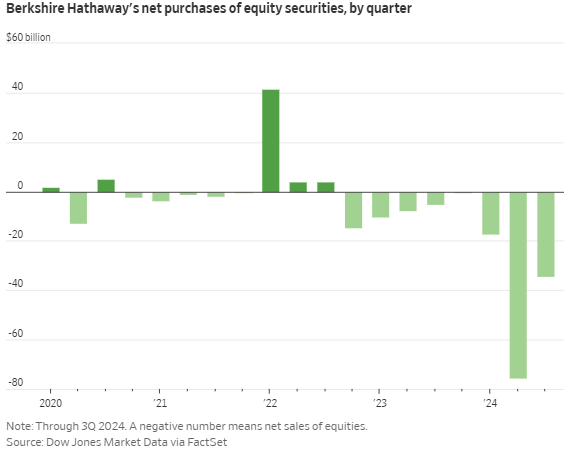

Berkshire released their annual letter, Buffett continues to build a cash war chest.

He has been a net seller of securities over the past 2 years.

Why does the housing market matter? Housing Starts since 1970 indicate that a decline often reliably predicts a recession.

The recent appreciation of housing prices has priced young people out of the market. The median homebuyer is now 56. Up from the mid 30s in the mid 2000s.