Thanksgiving Rebound 📈

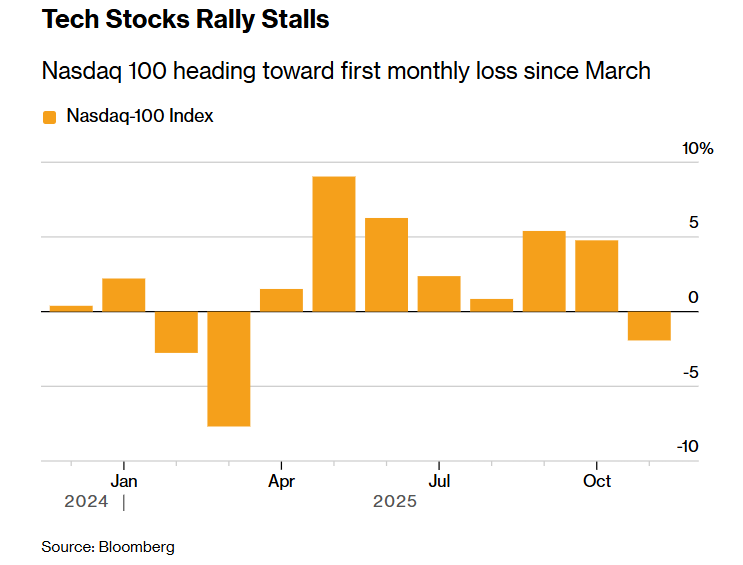

Broad US stocks had been down as much as 4.7% in November barely 10 days ago, as worries over stretched technology valuations rattled traders, but a slow holiday week saw markets rebound and finish the month roughly flat. Tech and Consumer Discretionary led the move higher, though gains were broadly distributed across sectors.

Yields fell 5 bps in both the US and Canada, supporting fixed income markets. Commodities and precious metals were strong, with silver up 13% on the week and close to doubling YTD, while crypto appears to have finally found a bottom

Investors rotated out of artificial intelligence winners and into more defensive sectors such as health care, leading the tech-heavy Nasdaq 100 to record its first monthly loss since March.

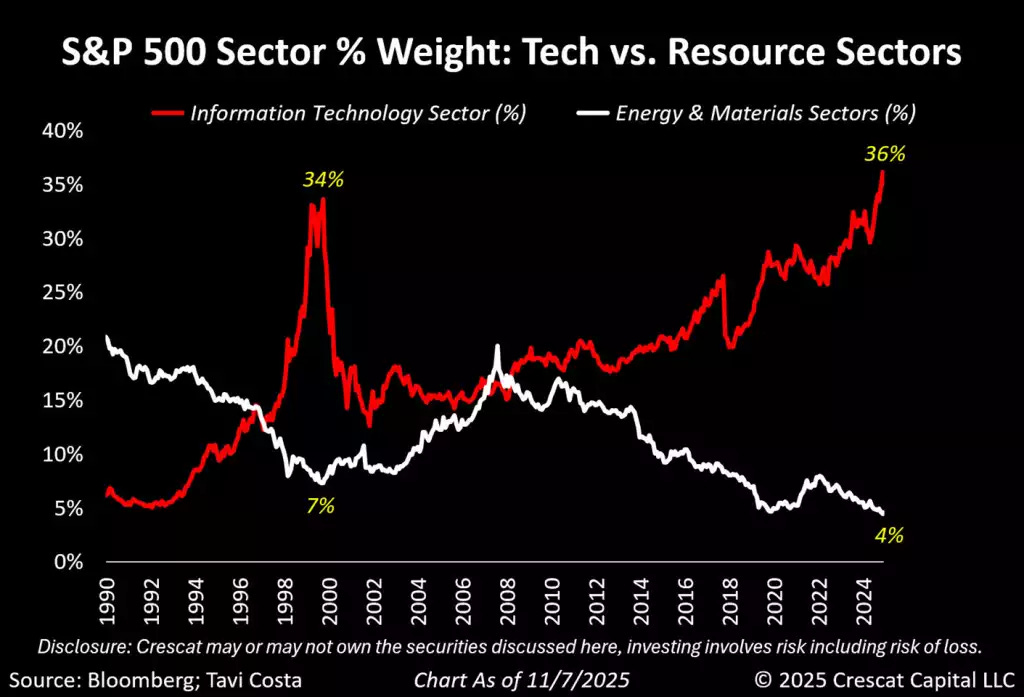

Tech stocks continue to dominate real assets. The question is whether the shift toward more capital-intensive, real-world investment by these tech giants could eventually trigger some mean reversion in relative performance. (Crescat)

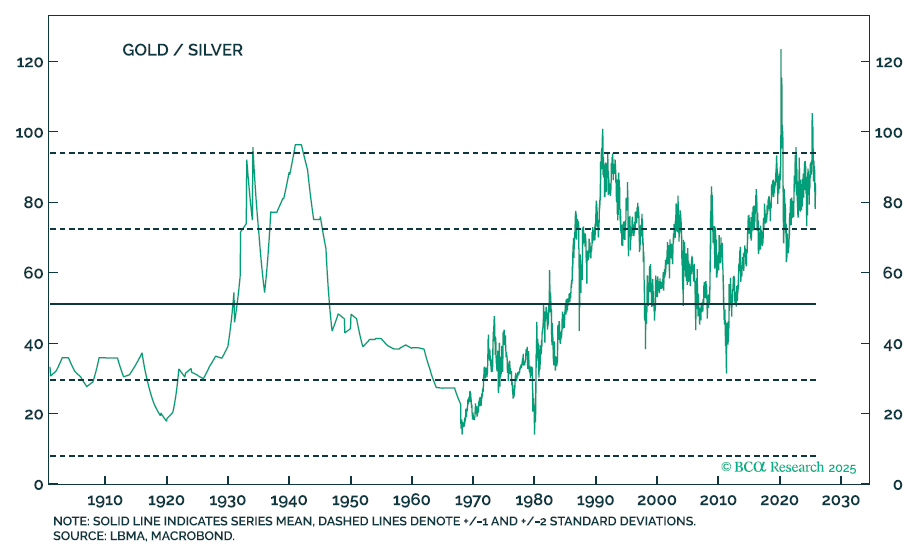

The gold-to-silver ratio had become stretched, and silver played catch-up last week. Some speculative capital that might once have gone into silver now appears to be diverted into crypto as an alternative store of value. (BCA)

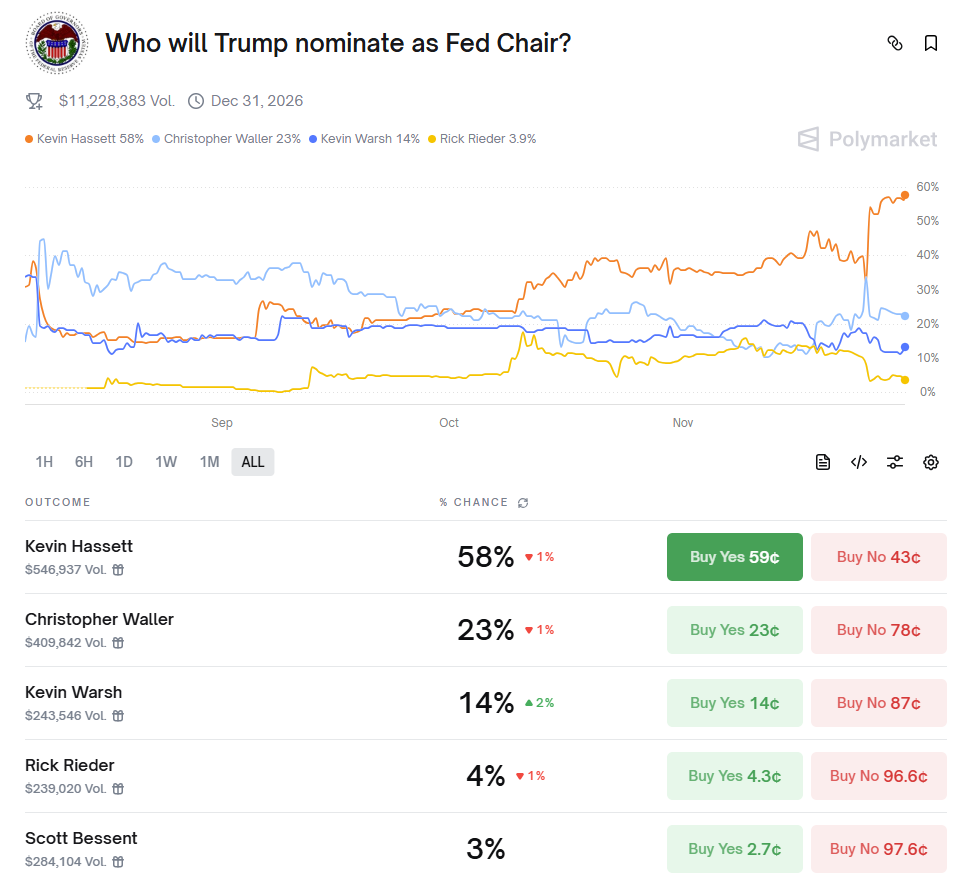

White House National Economic Council Director Kevin Hassett is seen as the frontrunner for Trump’s nomination of the next Federal Reserve chair. Hassett is seen to have an easier monetary stance, be more tolerant of inflation, align with fiscal stimulus, and introduce more policy uncertainty. Expectations are that the nominee will be aligned with current administration’s objectives. All of this pushes real yields lower and supports gold.

Interesting to see Dalio advocating for a tax on unrealized capital gains because he doesn’t see any better options out there. I don’t see how this works for the pre-IPO tech industry though. (link)

The United States and all the other countries’ governments that have overborrowed and are democratically run are now in a position where they a) can’t increase their debts as they did before, b) can’t raise taxes enough, and c) can’t cut spending enough to prevent running deficits and increasing their debts. They are stuck.

To explain in more detail:

They can’t borrow enough because there isn’t adequate free-market demand for their debt. (This is because they are already overindebted, and the holders of their debt already have too much of it.) Also, international holders of debt assets of other countries (e.g., China) worry that the war-like conflicts could lead to them not being paid back, so their buying of bonds is waning and they are shifting their debt assets into gold.

They can’t raise taxes enough because if they raise taxes on the top 1-10% of people (who have most of the wealth), a) these people will leave, taking their tax paying with them, or b) the politicians will lose the support of the top 1-10% (which is important to fund expensive campaigns), or c) they will pop the bubble.

And they can’t cut spending and cut benefits enough because that’s politically and, perhaps, morally unacceptable, especially as those cuts will disproportionately affect those in the bottom 60%…

…so they are stuck.

For these reasons, all democratic governments in countries that have big debt, big wealth, and big values differences are in trouble.

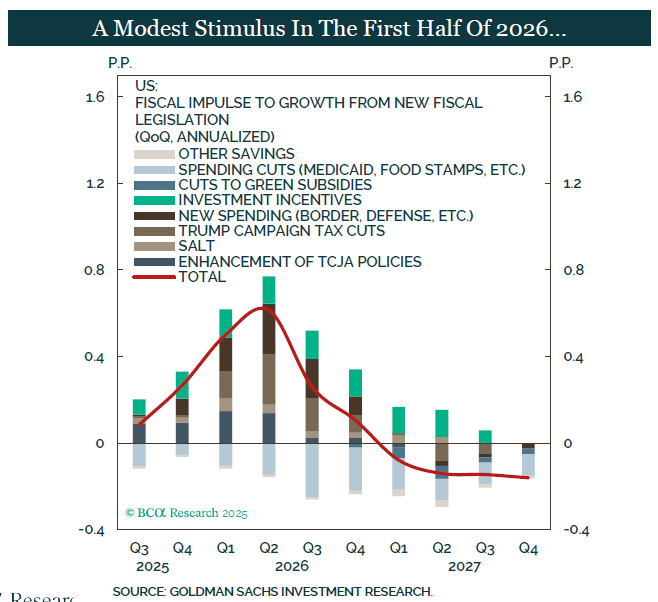

Goldman expects fiscal policy to remain stimulative into the first half of next year, which should help support growth, although underlying economic momentum still looks soft.

It is striking how small a role the stock market plays in household net worth outside of high-net-worth families. For lower-income households, net worth is far more dependent on the value of the primary residence. The majority of voters care more about housing market values than the stock market. (Apollo)

JP Morgan argues that with GPUs currently running near full capacity, AI infrastructure risks are more contained than in the dot-com era, when fiber build-outs were chronically underutilized. (@Mayhem4Markets)

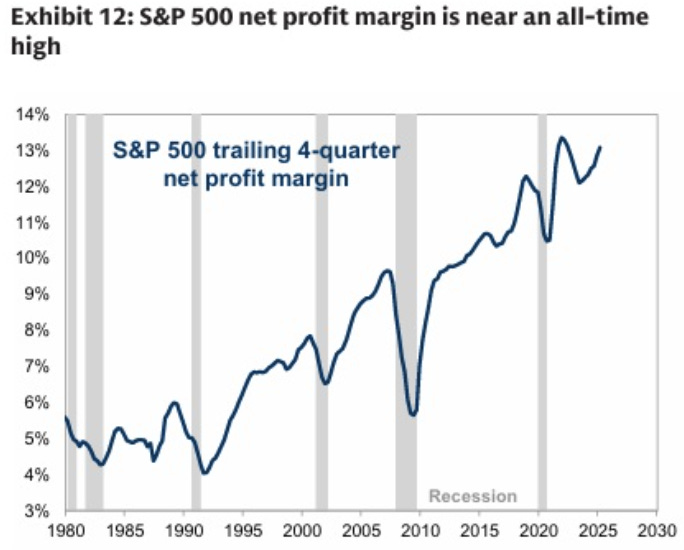

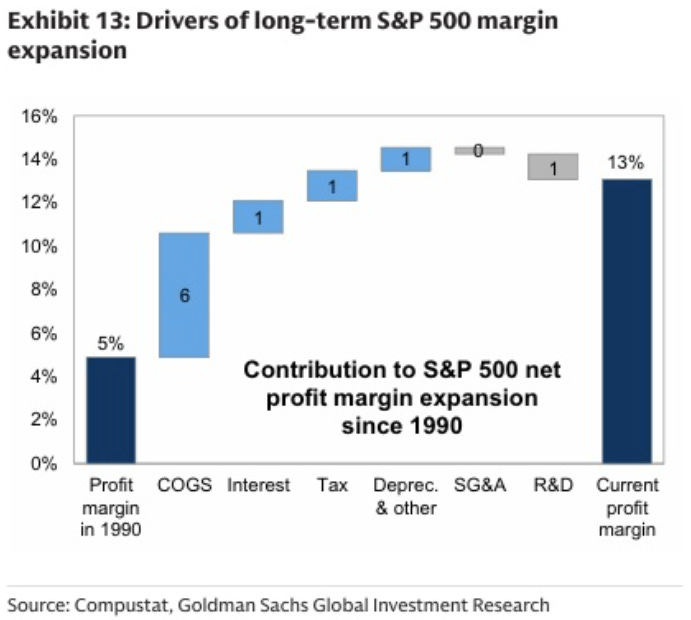

Profit margins never reverted and only have expanded since the early 90s. (Goldman)

A reduction in COGS has been the largest contributor. (Goldman)

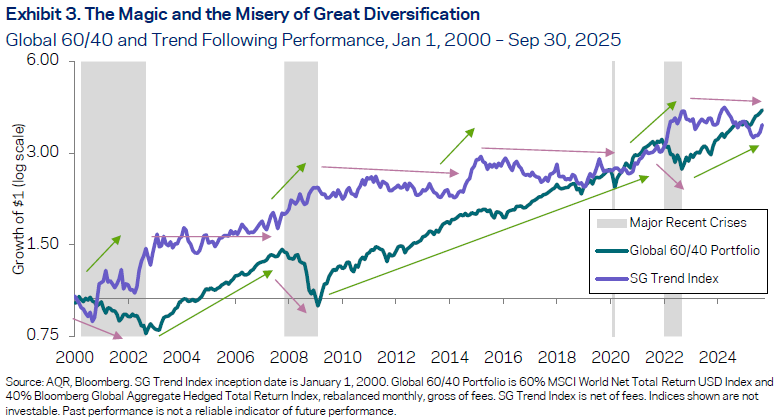

A dedicated camp of investors continues to champion trend following as a portfolio diversifier, yet returns have been lackluster since 2009. This may reflect crowding into the strategy after its past success, or simply that trend performs best in crisis regimes and has struggled in a long, crisis-lite environment. (AQR)

Chinese government bonds now yield less than those in many developed markets, underscoring how much the global rate landscape has changed.(BCA)