Healthcare: Dead Money or Deep Value? 🚑

Interesting paper from JPM on the Healthcare sector, summarized below. With sentiment at rock bottom, opportunity often rises from the ashes.

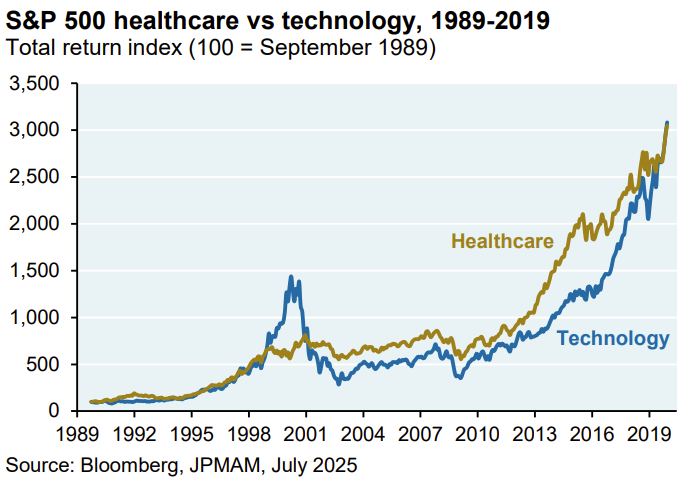

From 1989 to 2019, US healthcare stocks matched tech sector returns with significantly less volatility (15% vs. 24%).

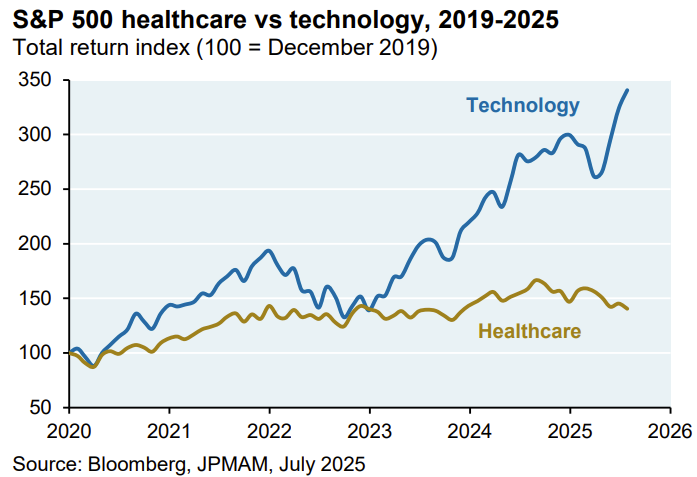

Since 2019, the tech sector's rapid advancement contrasts sharply with healthcare's stagnation. While large-cap pharma's forward P/E of 14x appears stable, this is skewed by Eli Lilly, which constitutes 35% of the S&P 500 Pharma Index and trades at a 24x forward multiple (down from 31x in July 2025 after disappointing oral GLP Phase 3 trial results). Other major pharma companies like Merck, Pfizer, and Bristol Myers trade at significantly lower forward P/E ratios of 8x-9x. Biotech valuations are deeply discounted, with 80% of biotech IPOs since 2018 failing. Managed care returns have declined, and life sciences face potential headwinds from reduced funding for scientific research organizations like the NIH, NSF, and CDC, evidenced by a sharp decrease in NIH grants through July.

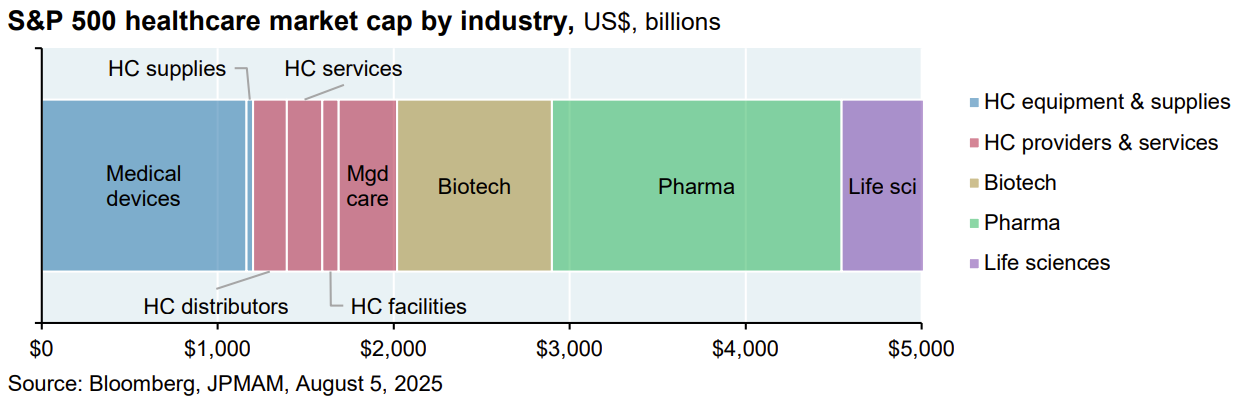

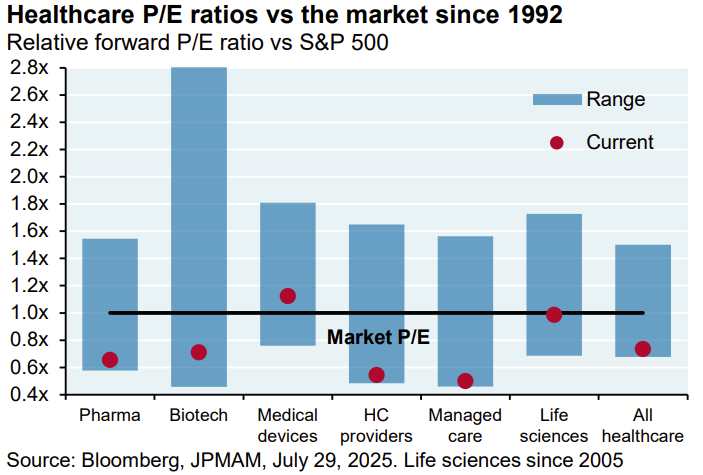

Healthcare names are diverse, and the sector comprises five sub-sectors, Pharma being the largest.

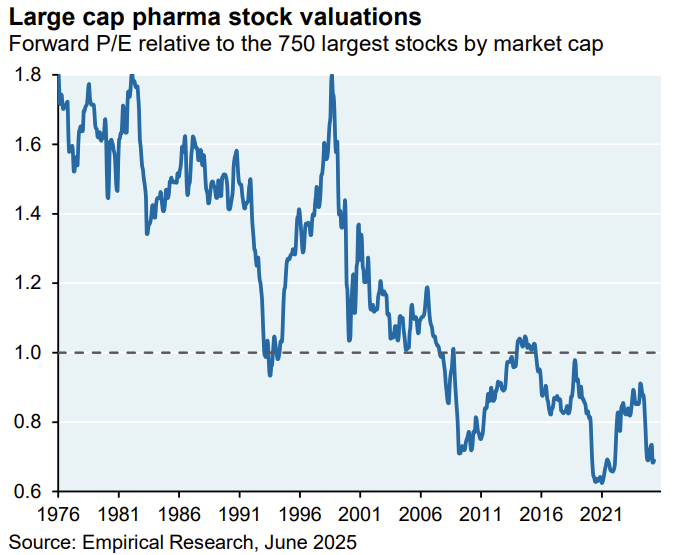

Since 1976, Pharma has gone from significant premium over the rest of the market to trading a discount.

While medical devices trade at a premium compared to the S&P 500, all other subsectors, unsurprisingly, trade at the bottom of their valuation range relative to the S&P 500 due to recent performance. Biotech exhibits the most valuation dispersion.

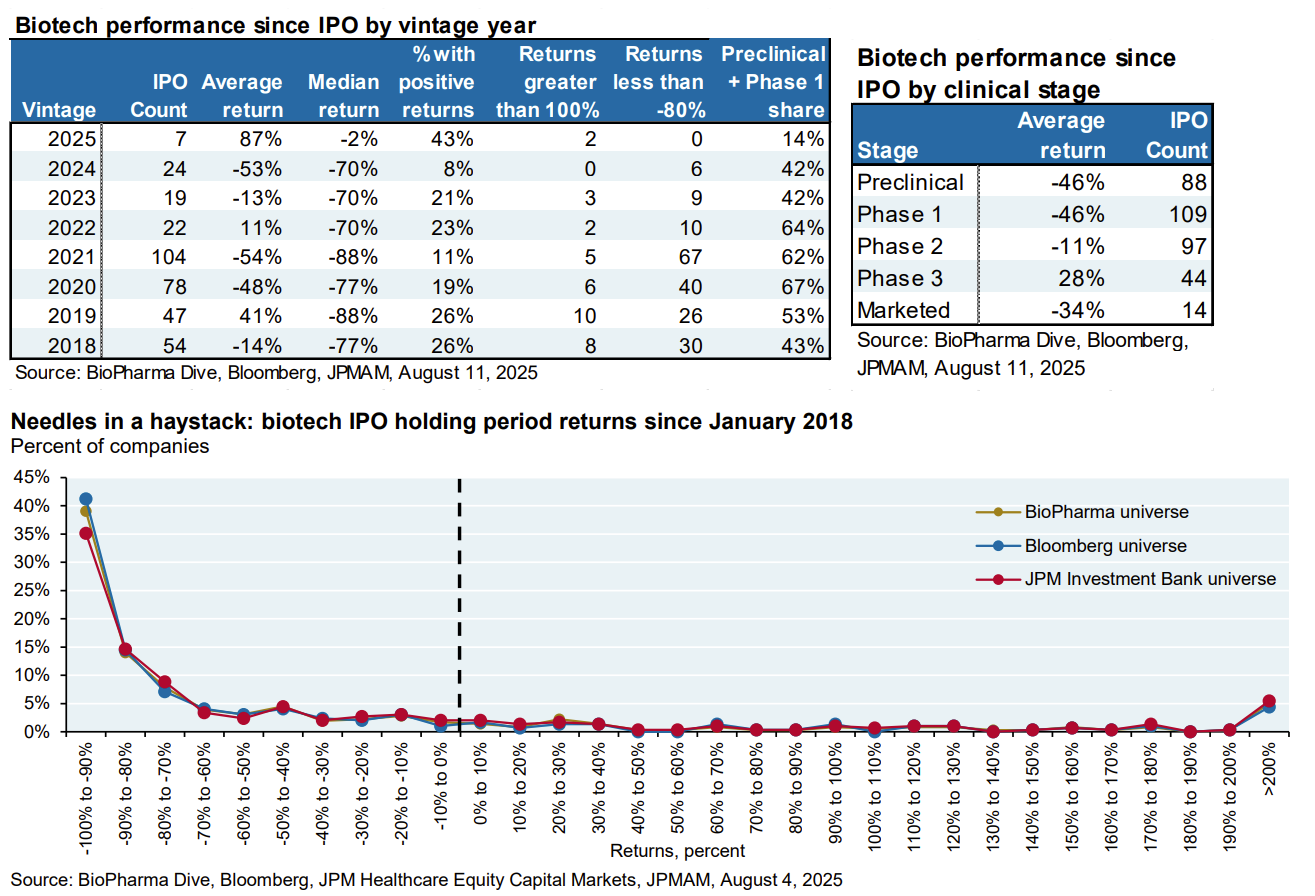

Biotech investors faced headwinds even before recent HHS and FDA changes. The sector, second only to Managed Care, experienced a significant drop in annualized returns post-2020. Prior to 2020, biotech returns boasted a 17% annual compound growth rate over 25 years. Since then, returns have plummeted to 6%. Has something changed? Data shows that identifying successful biotech IPOs has become exceedingly difficult. Since 2018, half of all biotech IPOs have lost over 80% of their value, with only 20% achieving positive returns.

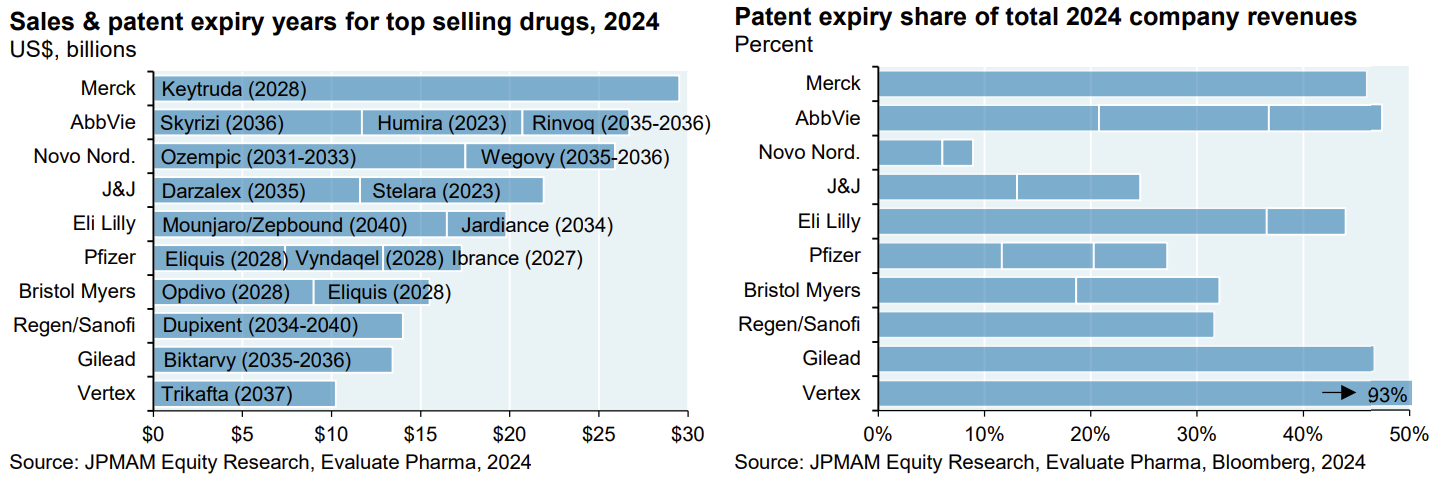

The impending patent cliff poses a significant challenge to the pharma industry. Several major companies face substantial revenue losses as patents for blockbuster drugs expire in the coming years. AbbVie, for instance, will see patents for Skyrizi, Humira, and Rinvoq expire by 2036, impacting approximately 50% of their 2024 revenue. Merck's Keytruda patent expires sooner, in 2028, while Pfizer's Eliquis, Vyndaqel, and Ibrance face patent expirations in 2027-2028.

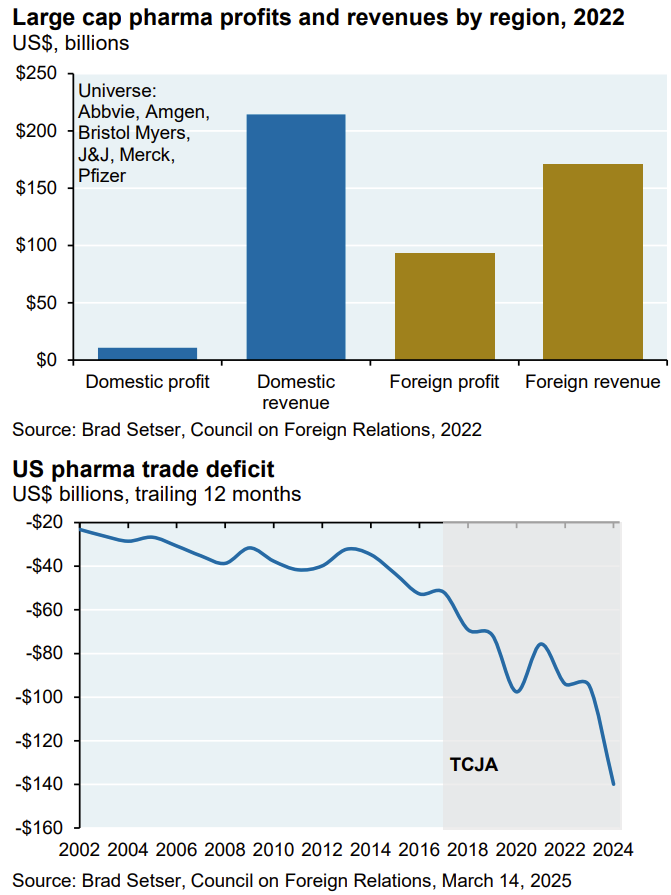

Section 232 tariffs on pharmaceuticals remain under consideration amid scrutiny of the industry's tax practices. Analysis by Brad Setser at the Council on Foreign Relations indicates that major US drug companies strategically report foreign profits in tax havens like Ireland and Singapore, while declaring losses in the US. Consequently, they pay the majority of their corporate taxes offshore, despite the US being their primary market. The US pharmaceutical trade deficit, averaging approximately $30 billion from 2002 to 2015, has significantly increased since the 2017 TCJA tax bill established a 10.5% minimum tax on global intangible income. This tax change appears to have incentivized US pharmaceutical companies to shift production overseas, causing the deficit to surge to $140 billion by December 2024, and further to $190 billion due to anticipated tariffs this year.

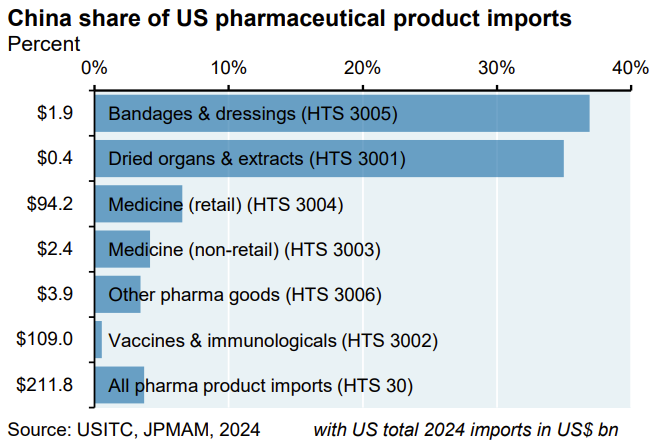

China's prioritization of domestic supplies during COVID-19 exposed US pharmaceutical supply chain vulnerabilities, prompting the establishment of a Strategic Active Pharmaceutical Ingredients Reserve, which was only 1% filled as of November 2024. While China's share of US pharma imports varies, it is generally higher in categories with lower import values. For instance, China accounts for over 30% of US bandage and extract imports, but these represent a small fraction of the overall value compared to medicines and vaccines. Consequently, China's share of total US pharma import value is only 4%. Less of an issue than the media makes it out to be.

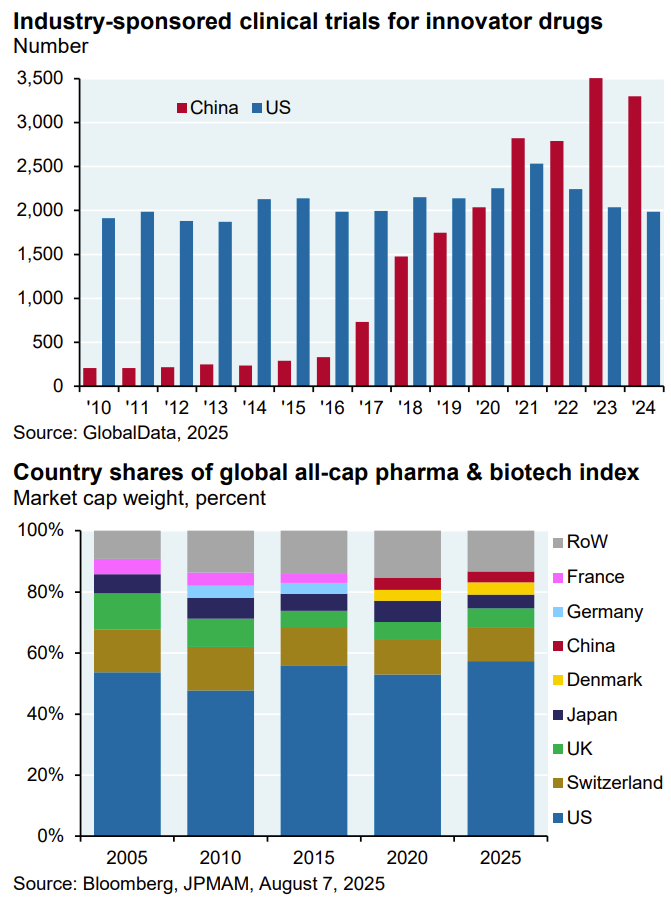

However, China is catching up to the US in industry-sponsored clinical trials and drug development. Acquisitions of Chinese drug companies haven't consistently boosted US large-cap pharma, as seen with Merck. Despite partnering with several Chinese firms in 2023-2024, Merck's P/E ratio remains near historical lows (8x-9x), though Keytruda's upcoming loss of exclusivity is a major factor. China still represents a small portion (~3.5%) of the global pharma and biotech market cap.

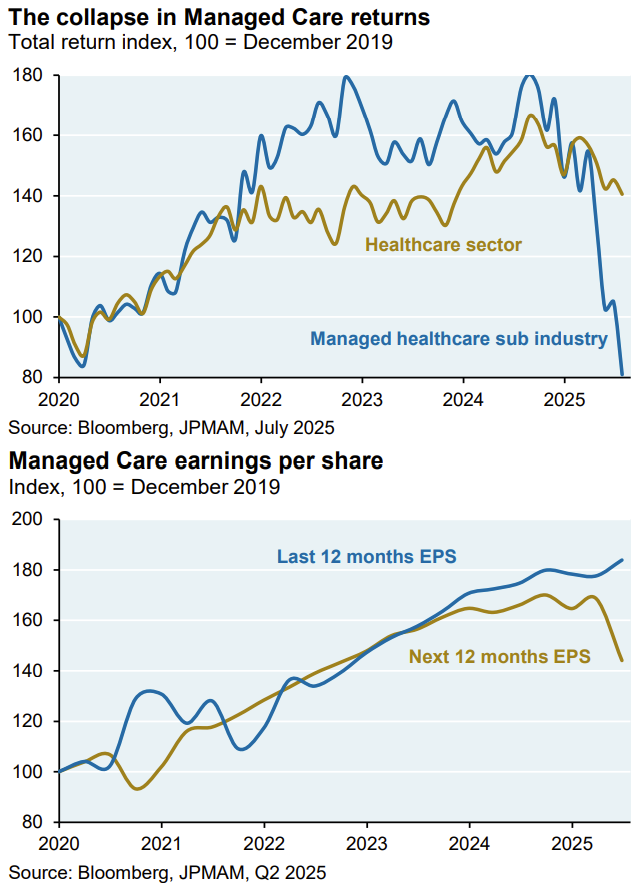

This year, health insurance providers, particularly large-cap managed care companies like Centene, Elevance, Humana, Molina, and United Healthcare, have underperformed. This decline isn't yet driven by earnings, but rather reduced industry guidance due to (a) Medicaid and ACA funding cuts from new legislation, (b) lower CMS Medicare Advantage reimbursement rates, and (c) for United Healthcare, increased scrutiny of Medicare Advantage billing practices and a higher-risk, higher-cost patient influx. For example, Centene withdrew its full-year 2025 earnings guidance in July and significantly cut its adjusted EPS forecast due to lower market growth in most of its operating states, notably impacting its ACA exchange business.

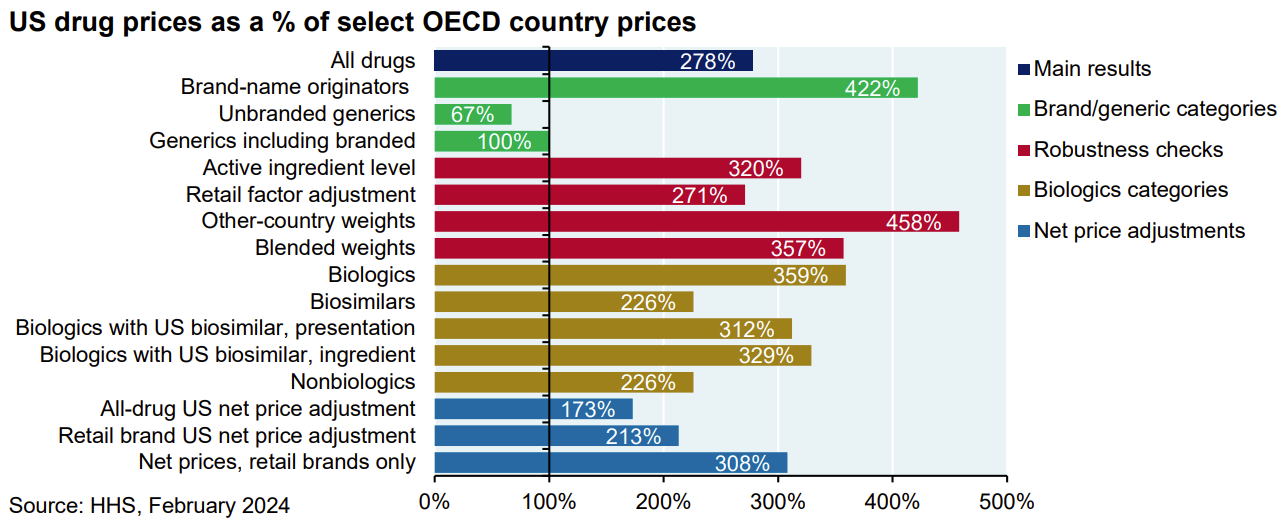

Finally, the current administration aims to address the fact that the US pays 278% more for drugs than other OECD countries across all drugs.

Thoughtfully provoking as always

Simple fact: U.S. has the highest cost healthcare in the world and consumers are running out of money, private and public, with which to pay for it.

IMO what we face is not a cyclical but a secular change in the economics of healthcare.