Themes for the New Year

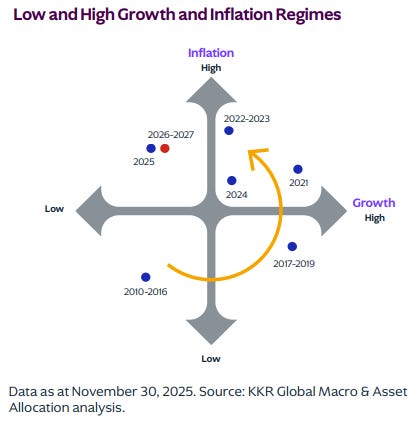

KKR anticipates stagflation, characterized by low growth and persistent inflationary pressures. I see these calls playing out as inflation settling around 3% instead of the targeted 2%, not a spike similar to 2022.

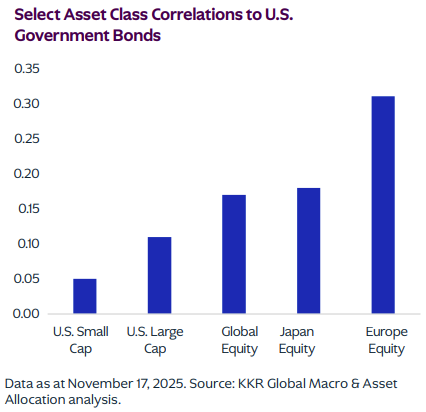

Thus, KKR sees limited diversification benefits from bonds. Current yields pretty much guarantee losses in purchasing power especially, after tax.

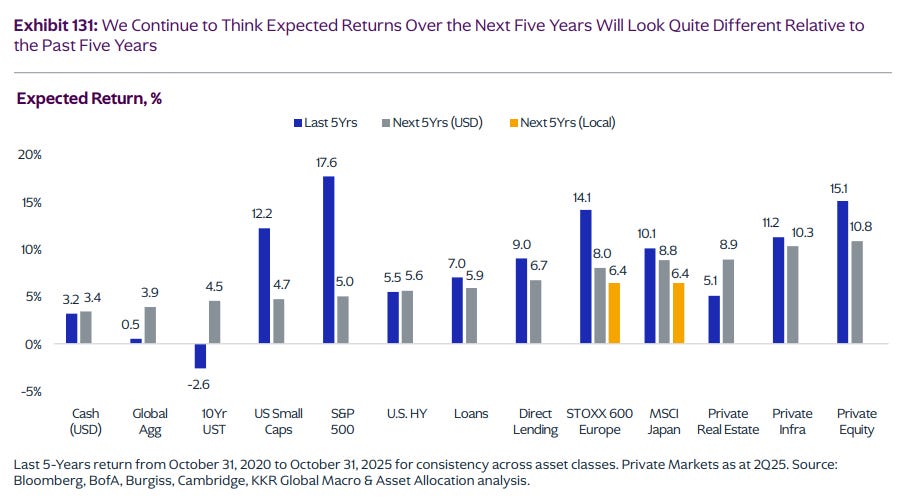

It is perhaps expected that a Private Equity firm would forecast its own sector as the top-performing asset class through 2030. Strategists continue to believe, forward returns will be lower, that prediction was wrong in 2025. They rag on the S&P 500. What do you think outperforms over the next 5 years, a PE fund investment or the Mag 7?

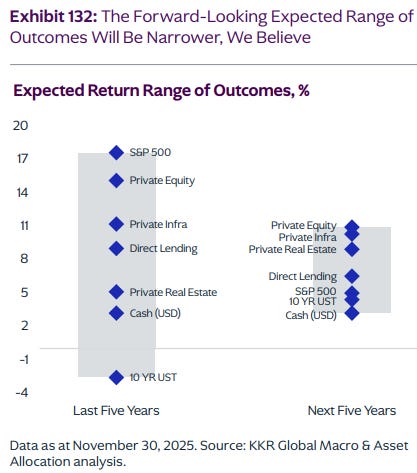

They see many assets classes bid up and less dispersion as alts have matured and public markets are priced richly.

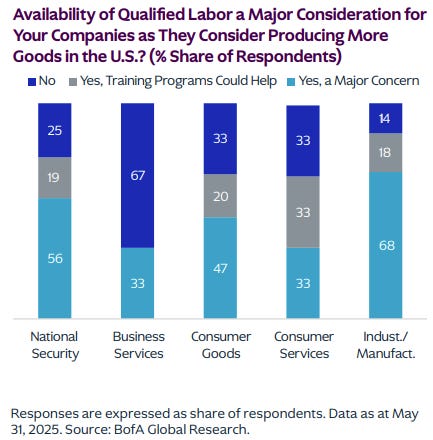

A critical challenge in the reshoring of supply chains is the sourcing of skilled labor. Over the last 35 years, the erosion of the U.S. industrial base has led to a significant loss of institutional knowledge and domain expertise. Rebuilding this capacity requires more than just moving factories; it requires revitalizing a workforce that has been decoupled from the manufacturing process for decades.

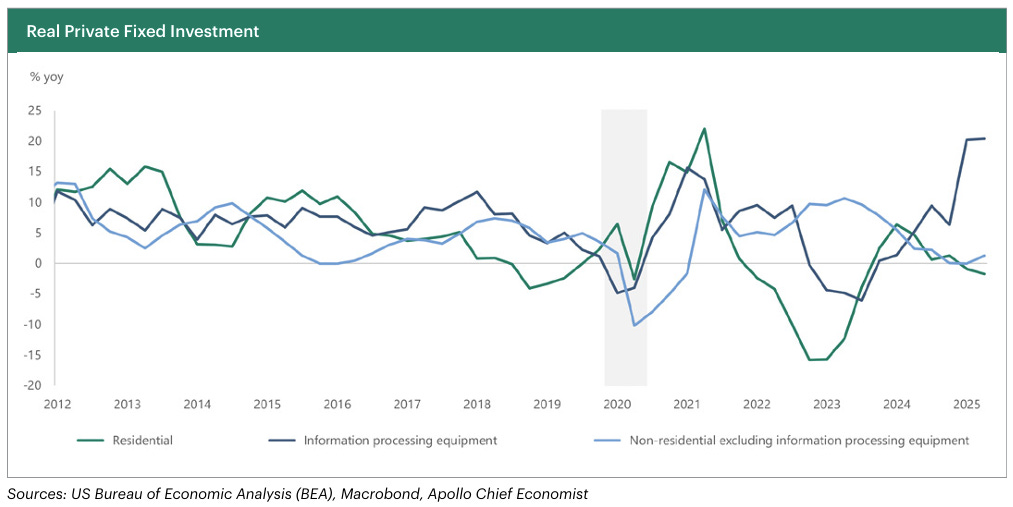

Thus far, reshoring has mostly been talk, the only private fixed investment occuring are data center build outs.

The current administration would love for the US to reclaim its status as the world’s leading exporter. This ambition is more feasible than most believe because modern manufacturing centers on automation rather than manual labor. By shifting the focus from labor-cost differentials to capital efficiency and proximity to consumers, the economic rationale for domestic production has never been stronger. Discriminating against Chinese manufacturers could result in a windfall for their US domestic competition.

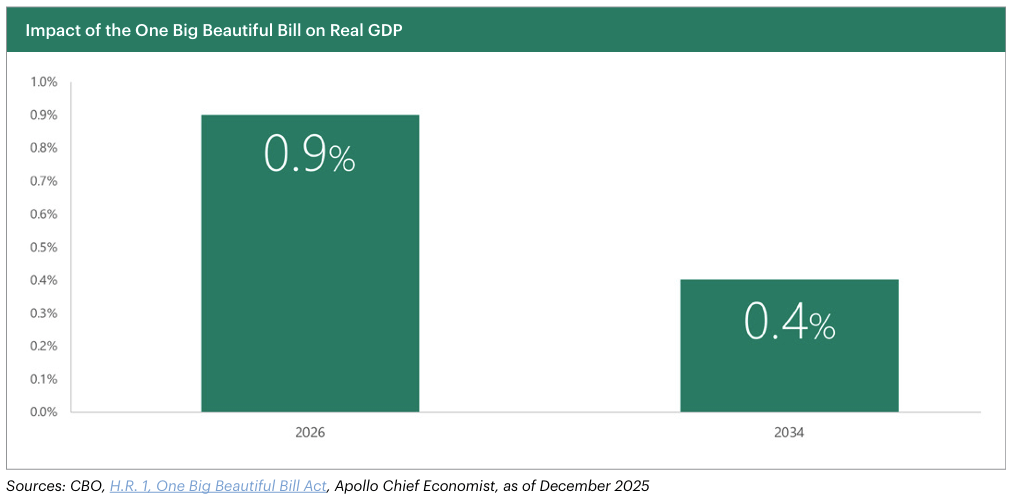

Treasury Secretary Scott Bessent anticipates that the OBBBA will drive GDP growth as it goes into effect this January. A key driver will be the 2026 'refund windfall' totaling an estimated $100–$150 billion. Because 2025 withholdings did not account for the new retroactive tax breaks, Bessent notes that the average working family can expect an additional $1,000 to $2,000 when they file their returns.

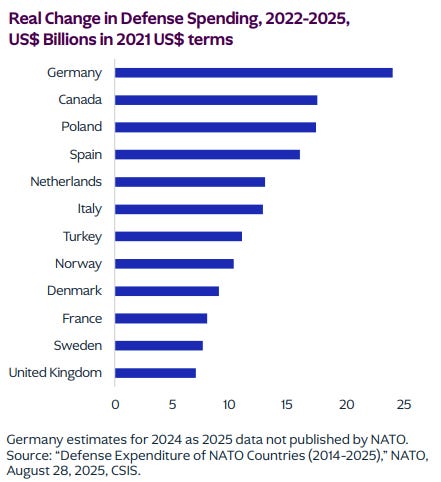

Defense is another beneficiary of continued government fiscal focus.

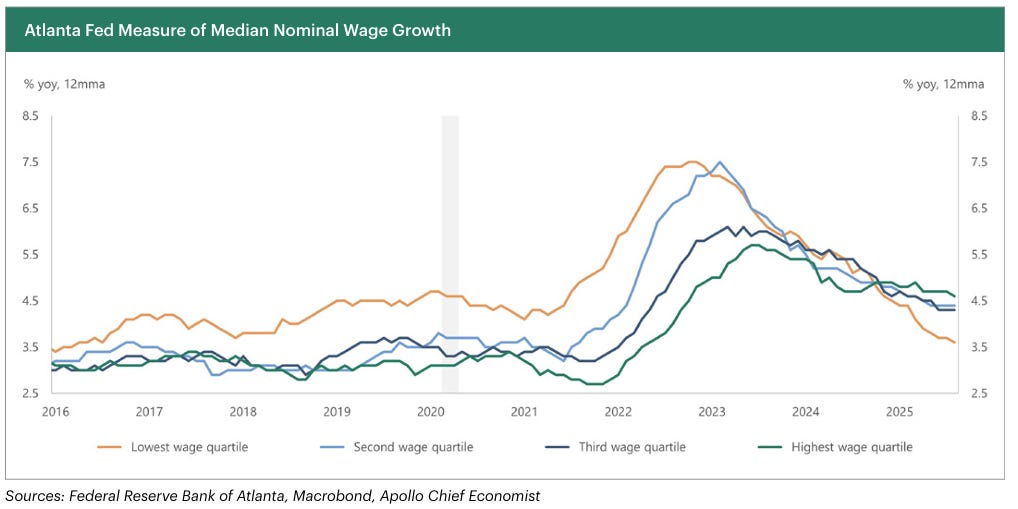

Subdued investment in the manufacturing sector has limited job creation, which in turn has eased the upward pressure on wages. Interestingly, despite the administration’s strict immigration enforcement, the lowest-income roles are currently experiencing the slowest wage growth. This suggests that factors beyond labor supply, such as shifting consumer demand or automation, are now the primary drivers of the wage floor.

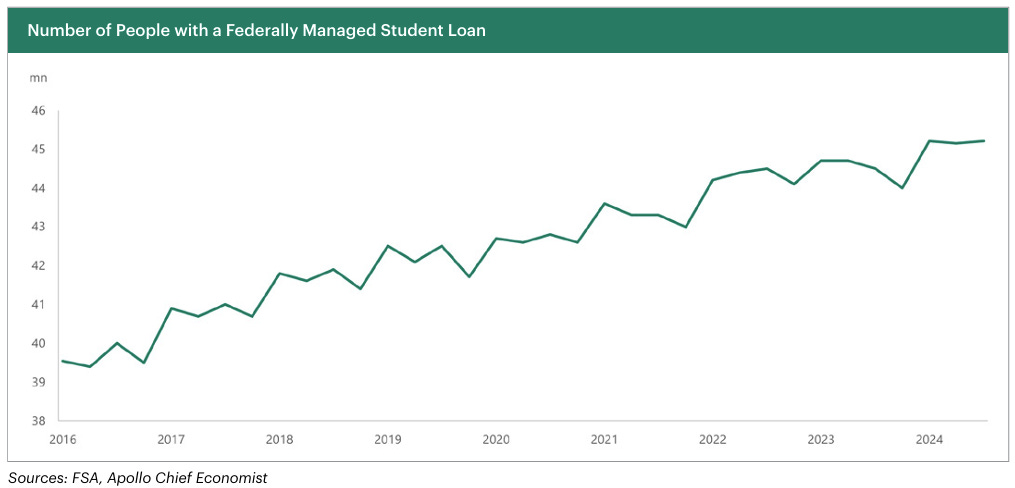

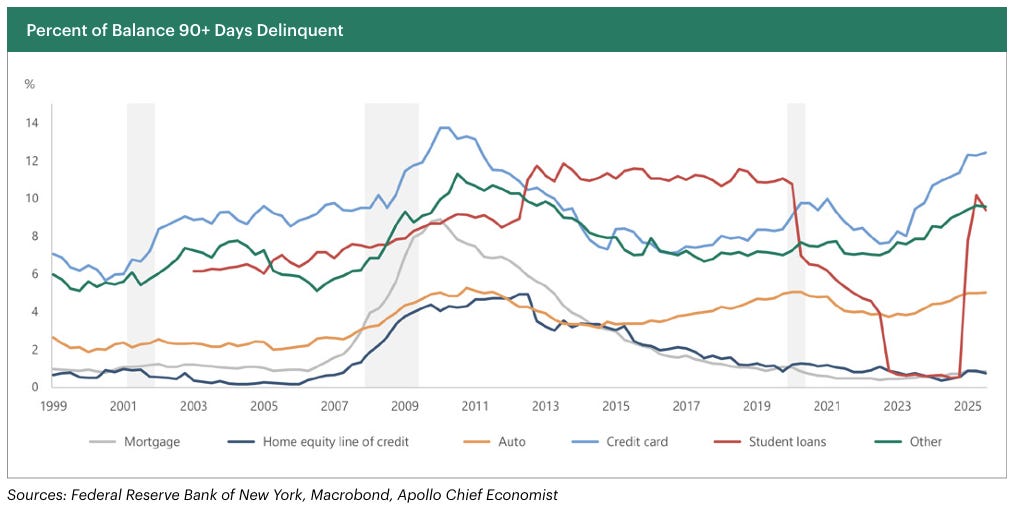

US consumers are divided. The end of the federal student loan repayment moratorium in May 2025 significantly altered the financial landscape for nearly 45 million Americans. This shift, impacting the spending power of roughly 20% of the population, could lead to an overall decrease in consumer spending.

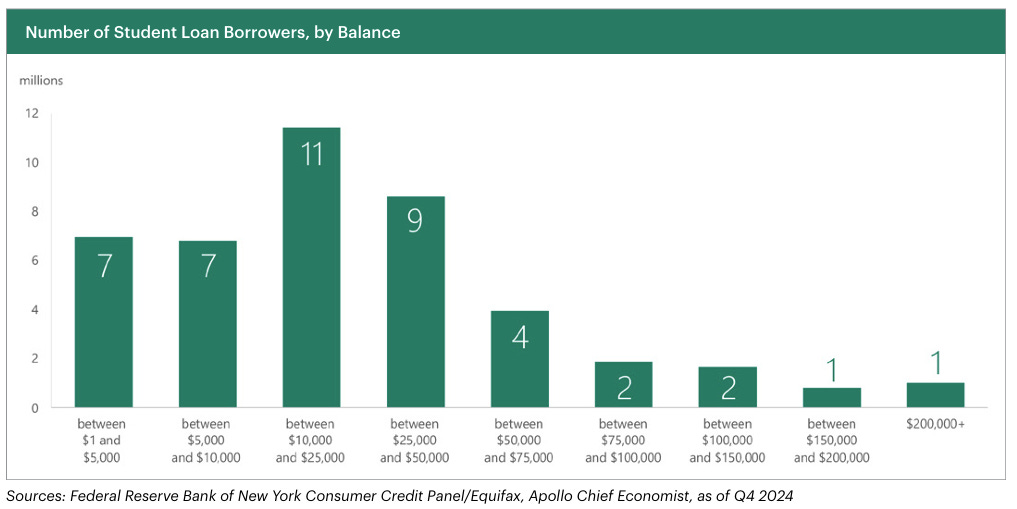

Almost 20 million borrowers have a balance of over $25k in student loans.

We are seeing a clear rise in 'stressed' borrowers across the board. In fact, 90-day delinquency rates for several credit categories are now tracking at their highest levels since the 2008 financial crisis. This trend is particularly visible in the bottom half of the income bracket, where the 'buffer' of pandemic-era savings has completely evaporated.

KKR forecasting PE as the best place to invest for the next 5 years is no different than asking the barber if you need a haircut...