Venture Capital Performance

Carta released some Venture Capital (VC) performance data last week. It looks like the vintages deployed during the bubble/pandemic are going to challenged.

While venture is a long game, the Carta report shows that only 9% of 2021 venture funds have distributed more capital than LPs paid in, a measure known as the DPI ratio. By contrast, 16% of 2020 funds and 24% of 2019 funds boasted positive DPI after 3 years—though as the chart below shows, even the 2019 funds are tracking well below their earlier counterparts in returning cash.

On one hand, DPI (Distributed to paid in capital) is clearly lagging previous vintages, on the other hand, the investments that are fund returners take more than a couple years to grow. An exit in year 3 is likely a failure.

The takeaway for your average investor, if you allocate to a VC fund, be prepared to wait almost a decade to see a return of your initial investment.

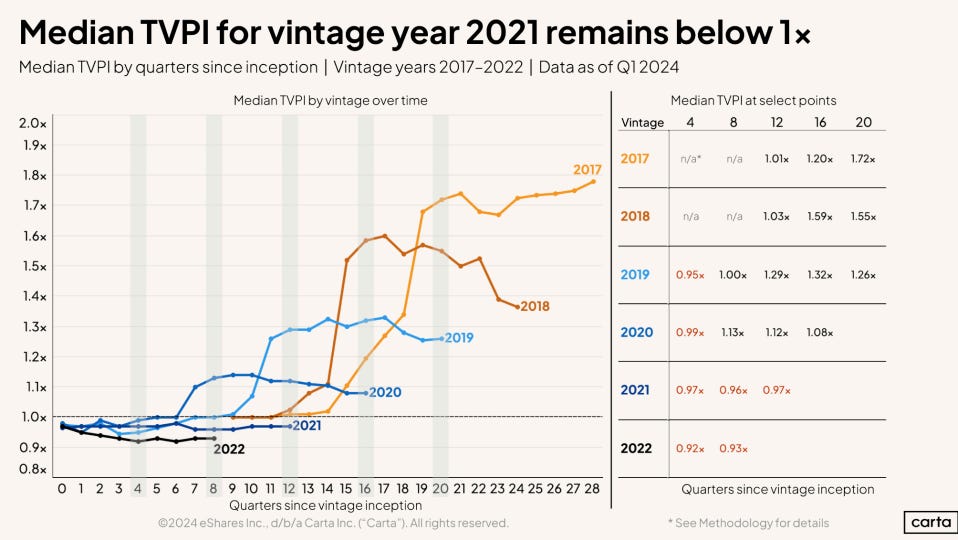

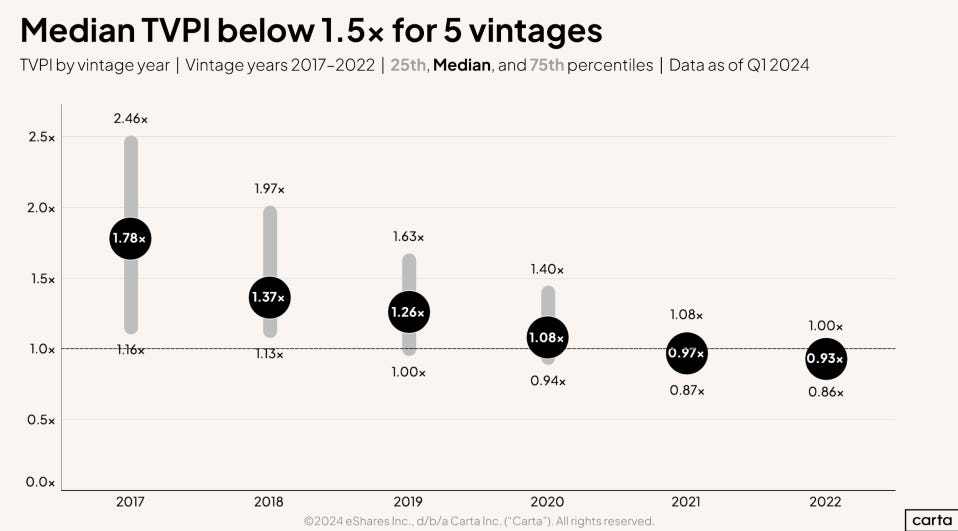

When looking at TVPI (Total value to paid in), the underperformance is clearer. Post 2020 vintages are stuck in the J-curve and underwater.

Another way to slice the TVPI data. The median 2017 vintage fund is sitting at 1.78x (data is net of fees).

Additionally, I am doubtful current marks fully reflect reality and are likely still inflated.

Looking at the performance data from an IRR perspective. Venture trails the Nasdaq (QQQ). The Nasdaq has delivered 20.8% annualized since 2017 and 19.7% since 2020.

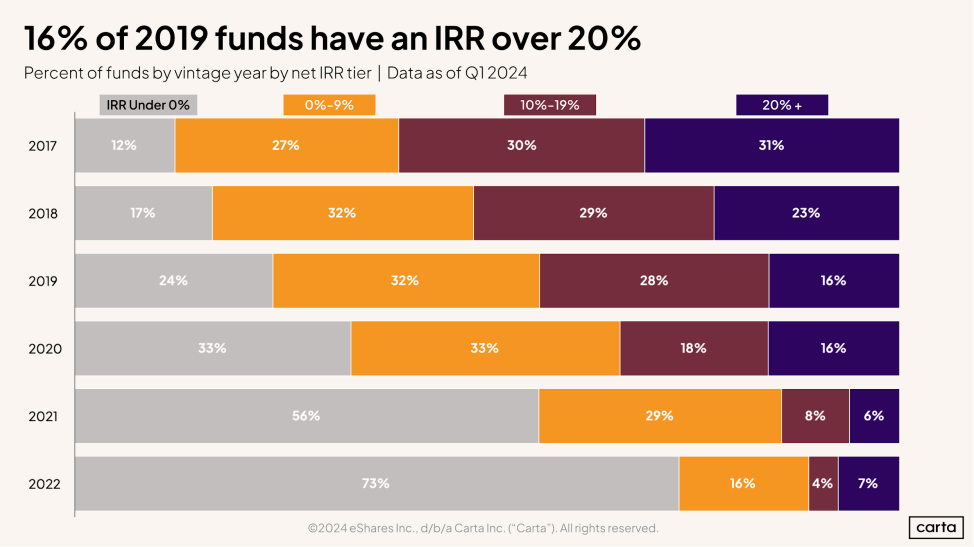

The top 31% of the 2017 vintage are boasting IRRs above 20% and 16% of the 2019 & 2020 vintages are clearing 20%. To justify the long lock-up, you probably need to be north of 20% at this point.

31% of funds in vintage year 2017 have an IRR over 20% (about 7 years into the lifecycle of those funds). A progressively smaller share of funds in each successive vintage are currently clearing the 20% mark, with a slight break in the trend at vintage year 2020.

The stark difference in performance by vintage year is clearer in the chart above. At the 12 quarter mark (three years into a fund’s lifecycle),the median IRR for vintage year 2019 had grown to 19.4%. The median IRR for vintage 2021, by contrast, failed to break into positive territory after the same amount of time.

It remains a challenging fundraising environment, most companies are resorting to bridge rounds, 42% of rounds priced in Q1 were extensions of previous rounds.

Historically, ~25% of companies would graduate from Seed to Series A after 7 quarters, it has fallen to ~13%.

Q1 had the highest share of down rounds in the past 5 years. This number is understated as the companies and VCs will try to structure deals that do not cause companies to take marks (converts, etc.).

And you’re seeing an increased number of start-ups shut down.

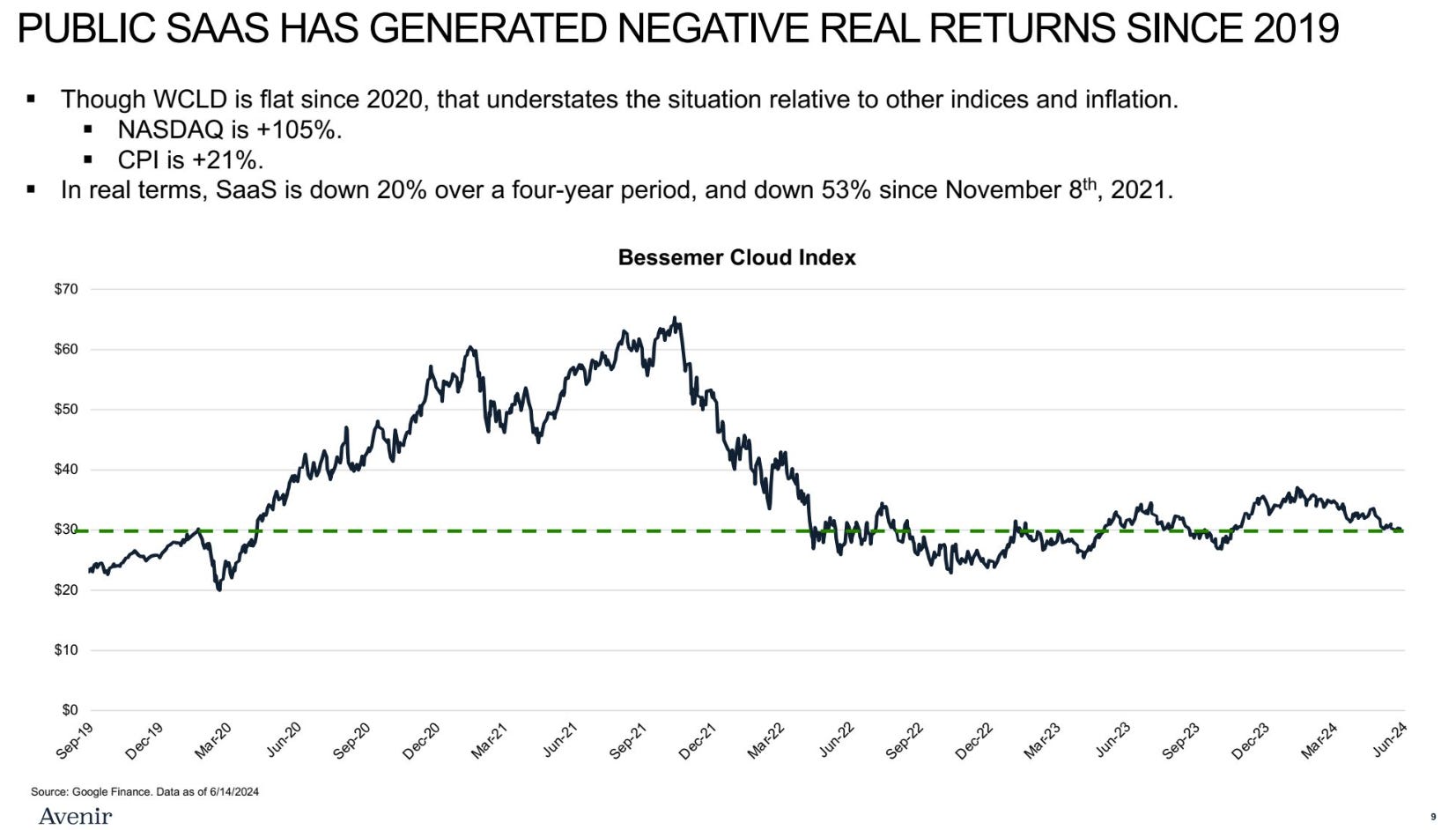

Public markets don’t look much better. The public SaaS index is flat since 2019.

San Fran remains the mecca of start-ups.

And the dollars follow.

All except for 1 of my MBB friends in PE/VC quitted before 2024