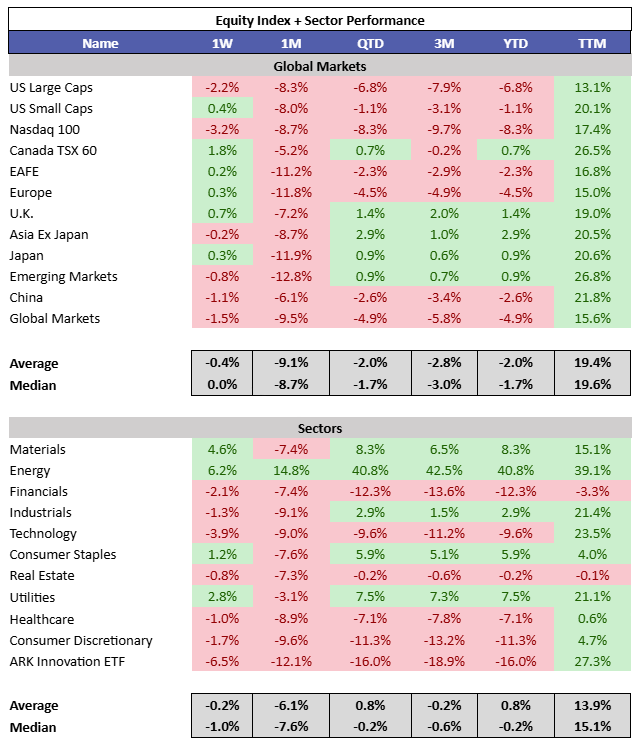

War & Oil

War and oil continue to dominate markets. Oil prices and yields continue to drift higher, while equities remain under pressure. Conflict appears to be escalating, with attacks on critical infrastructure from both sides and rumors of troops on the ground. The longer this drags on without a clear off ramp, the harder it becomes to ignore the impact of higher oil, tighter financial conditions, and potential pressure on consumption.

U.S. markets sold off, catching up to declines in the rest of the world. Energy was once again the best performing sector, Materials bounced after a difficult week prior, and Tech was the worst performing sector.

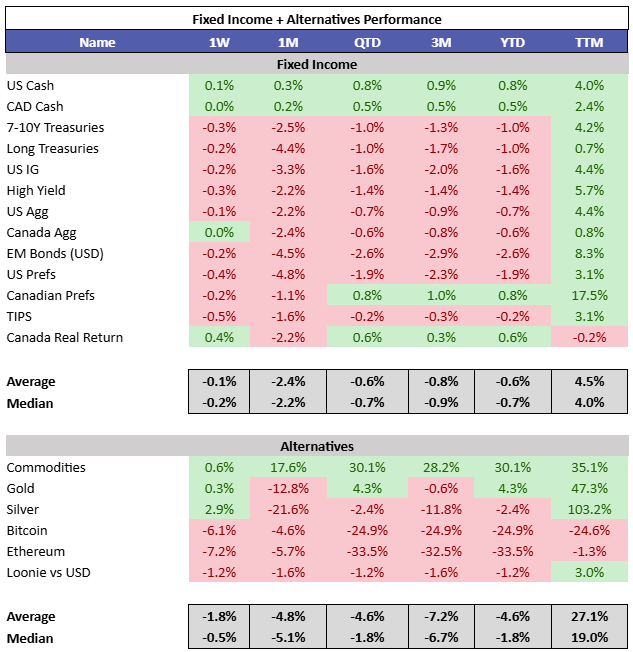

10Y yields rose 5 bps in the U.S. and 2 bps in Canada for the week. Precious metals stopped bleeding lower. Russia, Turkey, and Gulf countries are rumored to be gold sellers. Crypto finally cracked. And CAD has been selling off against USD this month.

It still feels like both sides are far from resolution. JP Morgan mapped out how a potential Hormuz closure could unfold globally. The red lines show oil from the Persian Gulf. The dates below represent when deliveries should stop across regions. (People's Art of War)

Asia: April 1

Europe: April 10

North America: April 15

Australia: April 20

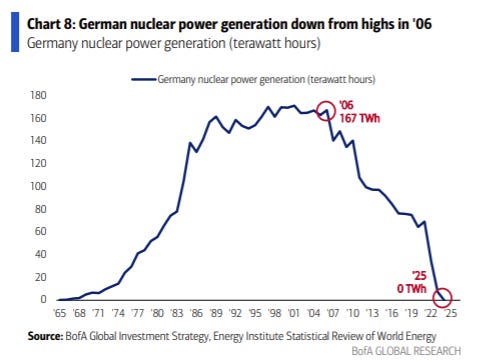

Now would be a helpful time for Germany to still have 167 TWh of nuclear capacity. This could become Europe’s second energy crisis in less than five years. (BofA)

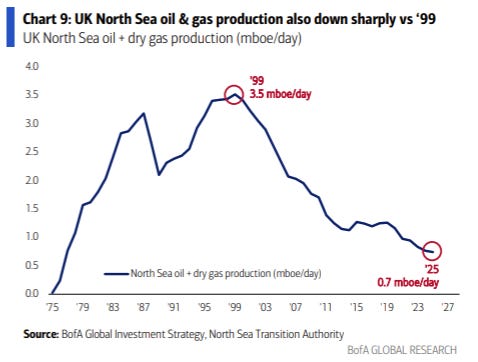

And it would be handy for the UK to have North Sea oil production but that was also curtailed. (BofA)

How this crisis differs from COVID is that you cannot print more oil. These are real assets. Countries are starting to panic and introduce emergency measures to shield populations from spiking oil prices. It will not stop governments from trying to paper over a tight market. This will only worsen government finances and should benefit stores of value. (Respeculator)

Gavekal wrote a research piece on other opportunities in the energy sector. Below are the key takeaways.

The oil futures curve looks increasingly interesting. If energy infrastructure has been damaged in a market that was already underinvesting in new supply, the market could tighten quickly. December 2027 contracts at $75 per barrel suggests markets still view this as temporary. The oil futures market continues to believe this is a short term disruption.

We partner with energy traders with decades of experience to help us and our clients navigate these markets. My colleagues recently interviewed them. Listen below.

Goldman still believes we get a quick resolution, but if the conflict drags on, expect energy prices to remain higher for longer. (@MikeZaccardi)

And do not forget the derivative impacts. Oil is just the tip of the iceberg.

This article dives deep into the second order consequences of this war.